A new study of the prominent NFT platform Foundation leverages crypto’s built-in candidness to answer a question foremost in the mind of every ambitious artist selling there (or anywhere): What is the recipe for market success?

The five laws clarified by the data may be able to help crypto artists improve their results on the platform. But they also lend support to the notion that the NFT market sometimes behaves much more like the legacy art market than many blockchain revolutionaries would like to believe.

Published in February in the journal Scientific Reports, the research was conducted by Barabási Lab, a team of artists and data scientists studying complex networks. It is the second analysis of a major NFT platform performed by the lab’s founder and namesake, Northeastern University professor Albert-László Barabási; he wrote about his research on SuperRare for the New York Times last May. (Barabási’s co-authors on the Foundation study are Kishore Vasan and Milán Janosov, the latter of whom also worked on the SuperRare piece.)

Studying Foundation, which launched in February 2021, provided an opportunity to focus on primary market data just as NFTs vaulted into the broader culture conversation via the $69.3 million sale of Beeple’s Everydays – the First 5000 Days at Christie’s that March. It is an understatement to say Foundation does not specialize in secondary sales; of the more than 48,000 NFTs originally listed for sale on the platform during the study’s course, a minuscule 138, or 0.2 percent, were actually resold there.

It’s vital to keep in mind that Barabási’s research into Foundation covers only about the first five months of its lifespan (ending June 18, 2021). Still, its five main findings about artistic success on the platform are clear and powerful. Based on what I know about how markets for art and collectibles tend to work, I’d also bet that they are more likely to stay ingrained for the long term than to fade out over time.

Here they are…

1. It Pays to Be First—and It Keeps Paying

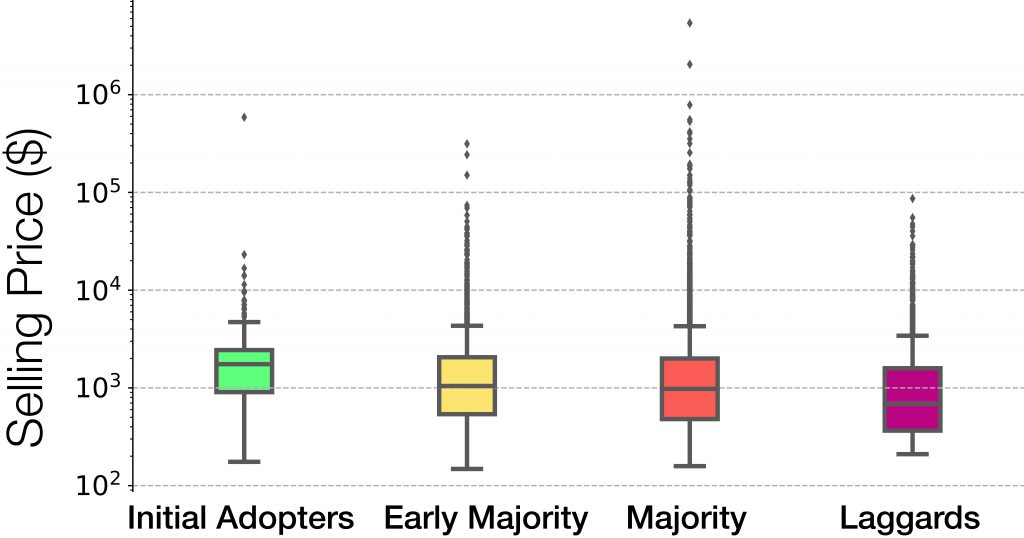

Selling prices of Foundation artists segmented by the period during which they joined the platform, showing a first-mover advantage between groups. Visualization by Barabási Lab. Courtesy of Barabási Lab.

Artists who joined Foundation earlier sold more NFTs on average, and at a higher average price per NFT, compared to their counterparts who arrived later in the platform’s life cycle. This led the early entrants to higher total earnings overall. Barabási and company wrote that these results reflected a clear and lasting “first-mover advantage” in terms of artistic success.

Notably, the researchers found that the first-mover advantage applied to more than just the very fastest artists off the starting block. The effect persisted even when comparing different groups of artists that joined Foundation at different junctures to one another.

Yes, the group labeled the “initial adopters”—the first 2.5 percent of artists to start on Foundation, joining between January 21 and February 22—out-earned the “early majority” artists—the 13.5 percent of artists who joined between February 23 and March 10. But the early majority, in turn, also out-earned the later “majority,” who in turn out-earned the “laggards,” the 16 percent of artists who began selling on Foundation between May 19 and the study’s conclusion.

We can see the effect more clearly by breaking it down into components. Of all NFTs offered on Foundation during the initial-adopter period, more than 74 percent found buyers. Yet the same was true for a smaller and smaller share of the NFTs released during each subsequent phase of the market, ending with only about 13 percent of the NFTs offered in the laggard phase selling.

A similar relationship manifested in terms of NFT sale prices (shown in the chart above). The median selling price (meaning, the price separating the top half of results from the bottom half) was $1,746 during the initial-adopter window. It dropped to about $1,046 during the early-majority period, however, before sinking to about $976 during the majority phase, and $688 during the laggard phase.

What accounts for the first-mover advantage? Barabási and his team chalk it up to two related factors. The first is what I’ve previously called the “tyranny of options“: as more and more people offered more and more works on Foundation, artists naturally had a more and more difficult time standing out. Second, the initial frenzy to get in on the NFT market subsided over time (presumably as Beeplemania ebbed), leading buyers to pull back on their purchasing. In short, both supply and demand favored the early adopters.

2. It’s Better to Be ‘Foundation Famous’ Than ‘Twitter Famous’

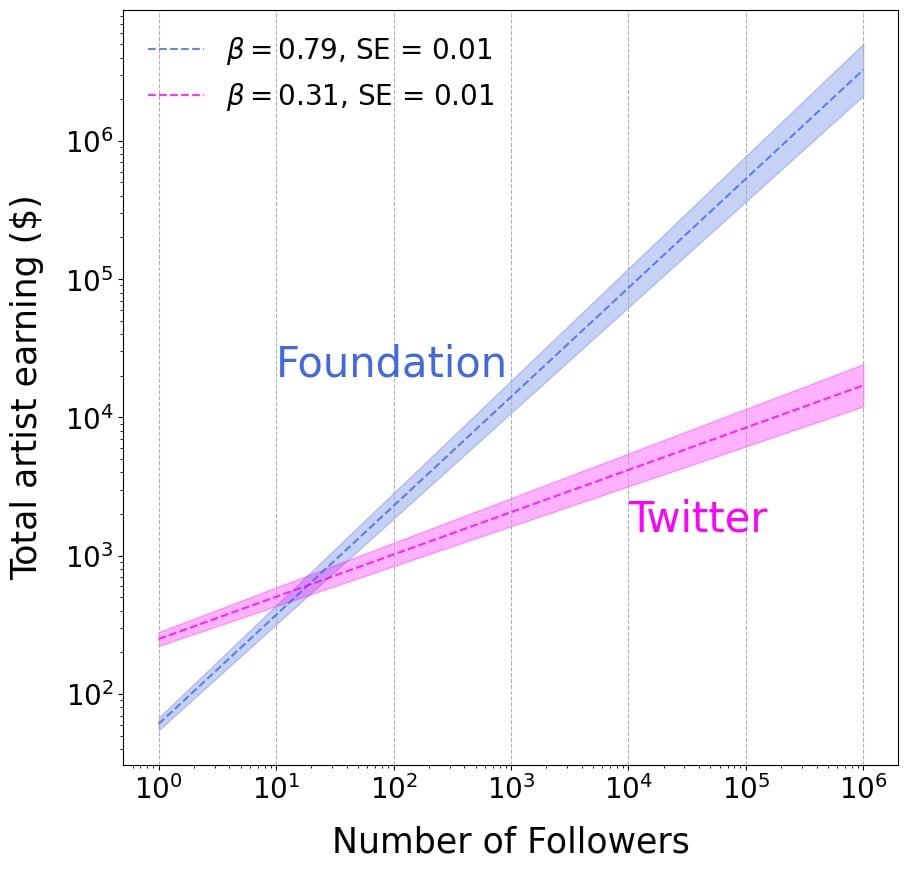

Earnings of Foundation artists in relation to follower count on Foundation versus Twitter, showing the former is exponentially more important to sales than the latter. Visualization by Barabási Lab. Courtesy of Barabási Lab.

Like Twitter or Instagram, Foundation allows users to follow artists on its platform to receive notifications about their activity, including new NFT drops. Yet Foundation is only a niche within a niche of the crypto space compared to Twitter itself, which has become the headquarters of crypto enthusiasts in general and crypto artists in particular.

This is part of the reason why NFTs are often seen as a mechanism for monetizing viral fame. Think of the NFTs for the original Nyan Cat GIF and Disaster Girl photo selling for almost $600,000 and $500,000, respectively. It’s difficult to imagine those prices (and many others) soaring so high in the crypto space without the consensus-building propulsion of Twitter. No wonder many, if not most, artists tweet about their Foundation drops to maximize visibility and (they hope) prices.

But the data shows that this cross-platform marketing strategy provided mixed returns. Gaining Twitter followers modestly boosted artists’ sales; gaining Foundation followers dramatically boosted artists’ sales.

By growing their Foundation audience from 100 followers to 1,000 followers, the study found, artists “likely experience a tenfold increase in earnings.” Artists would have to increase their Twitter follower count from about 100 to 10,000—an order of magnitude more—to capture an equivalent rise in earnings.

The analysis suggests that Foundation is something of a closed circuit for crypto artists. Their online presence elsewhere is nice—but unless they can port their audience over to Foundation, their success there will be limited.

3. It’s Still About Who You Know

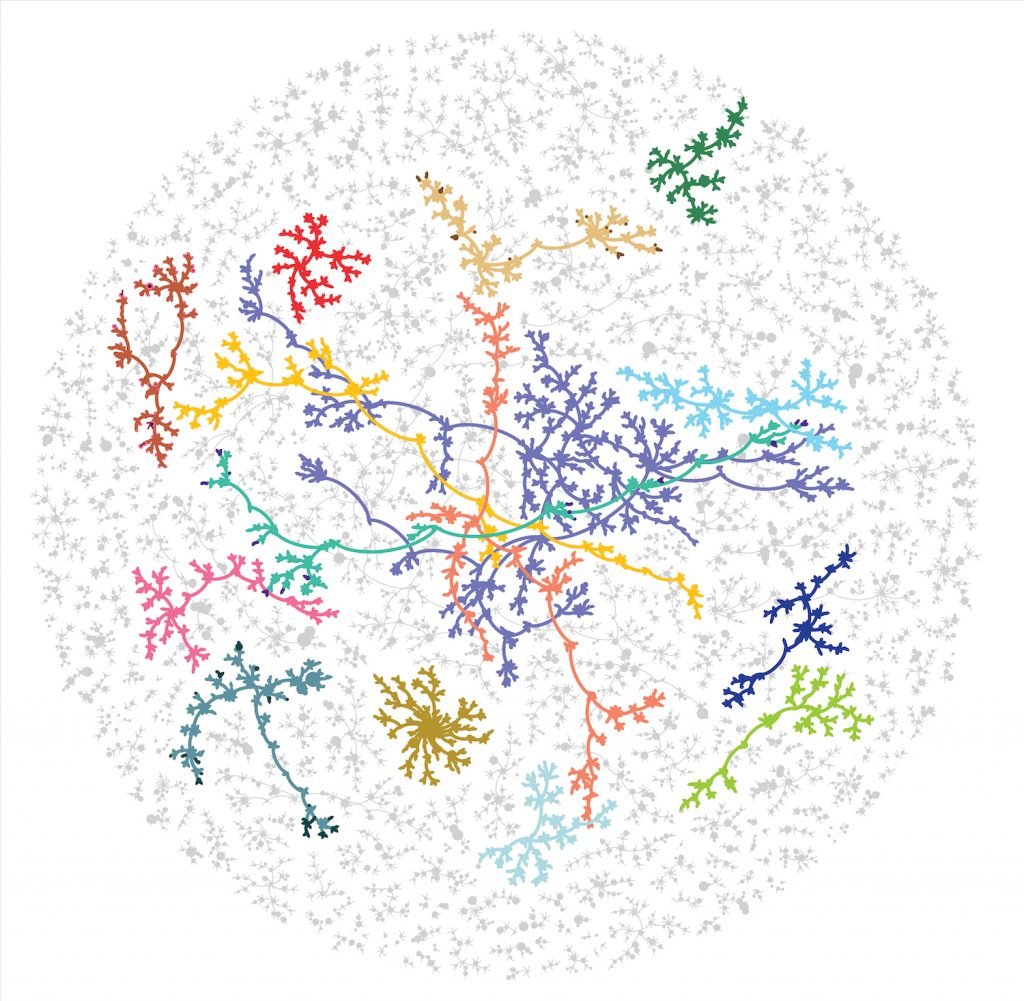

Network map of the 204 artist clusters that emerged during Foundation’s first 100 days, showing which artists invited which others onto the platform. The 20 largest clusters by quantity of artists are each displayed in a different color, with each node corresponding to a single artist, and the size of each node corresponding to that artist’s sales volume. Visualization by Barabási Lab. Courtesy of Barabási Lab.

As a so-called “open” platform, Foundation grows its creative community by allowing artists to invite other artists to show and sell there. This dynamic hews closer to the utopian, collectivist rhetoric of crypto than closed platforms like SuperRare, which grows by “onboarding only a small number of hand-picked artists,” according to its website.

Since every Foundation artist’s profile page includes an “invited by” tag, Barabási and his team were able to map every network of invitations that sprouted on the platform in its first five months. They found that the 14,706 artists who were on board by mid-June arrived via 640 individual networks (which the researchers call “artist clusters”), each made up of an average of 22 artists.

Crucially, the data showed that select artist clusters dramatically outperformed others. The chart above shows every one of the 204 artist clusters that emerged in Foundation’s first 100 days, with the top 20 clusters by number of artists each displayed in a different color. (For an animation representing their growth over this time span, click here.)

Based on these results, Barabási and company were able to separate the sell side into what they called “rich” and “poor” artist clusters. The highest-earning cluster in the sample sold more than $2.7 million worth of NFTs, with a mean price of nearly $6,800 per token. Both measures eclipsed the maximum figures achieved by a randomized sample, where the highest-earning cluster sold only about $902,000 worth of NFTs, with a mean price under $2,700. (The effect persisted even after the researchers omitted the top-selling NFT in each cluster.)

The opposite manifested on the low end of the earnings continuum. The poorest artist clusters sold significantly less work by value overall, and at a significantly lower average price per NFT, than the worst-performing cluster in a randomized reference. So if you were offered a Foundation invite from an artist you knew to be struggling on the platform today (well after the first-mover advantage has disappeared), the data indicates you would be better off holding out for the prospect of a better offer later on.

Members of these extreme clusters were rich or poor in terms of more than just total earnings, too. They also sold significantly more (or less) NFTs by volume, had larger (or smaller) Foundation followings, and larger (or smaller) Twitter followings than randomness would allow.

Among these myriad metrics of success, then, the message was the same: new artists did about as well, or as poorly, on Foundation as whoever brought them on in the first place. So while the open platform democratized access, success was largely predetermined by artists’ pre-existing relationships.

4. It’s Very Hard to Shake Your Initial Reputation

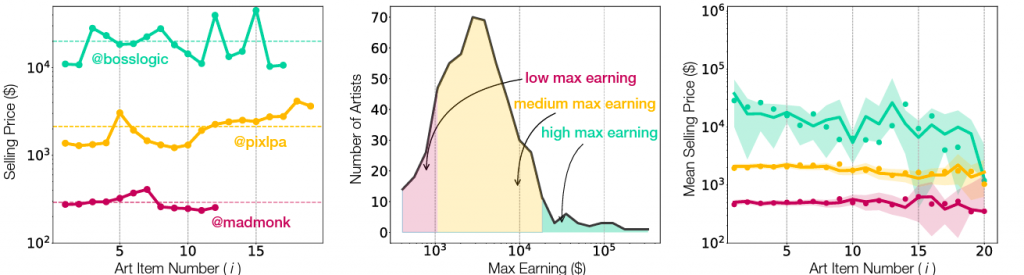

Segmentation of individuals artists’ prices (left), max earnings by group (middle), and mean selling price by group (right) based on their initial reputation. Visualization by Barabási Lab. Courtesy of Barabási Lab.

On Foundation, artists are responsible for setting their own prices. In fact, if a new work fails to attract interest at its initial asking price, the artist can simply re-list it at a lower price to try to spur bids. (Foundation allows works to be offered for private sale or public auction; in the latter case, a 24-hour countdown clock begins when a bidder agrees to meet the listed reserve price.)

This setup means artists’ sale prices on Foundation theoretically could be much more responsive to demand than in the traditional gallery sector. There, dealers try hard to ensure that prices neither rise unsustainably quickly, nor fall too much, ever (even in the absence of demand).

On Foundation, however, each artist’s selling prices behaved like something of a hybrid: they often varied significantly from NFT to NFT—but they also tended to remain within a stable, clearly bounded range. Crucially, this range tends to be set by an artist’s very first sale. Informed by their findings about artist clusters and the sales significance of social networks, Barabási and his co-authors conclude that this price stability depends on an artist’s initial reputation.

The researchers used sales data to split Foundation’s artist population into three distinct classes (visible in the middle chart above, for max earnings): low-reputation (the bottom 20 percent of artists, all with their top sale coming in below $1,254), medium-reputation (the middle 75 percent of artists, all with their priciest sale falling between $1,254 and $18,510), and high-reputation (the top five percent of artists, all with their priciest sale surpassing $18,510).

To ground this discussion in specifics, consider the high-reputation artist known as bosslogic. Nearly all of the 17 NFTs that bosslogic sold on Foundation during the sample period traded for between $10,000 and $30,000 each. But individual prices rose and fell significantly within this price band. For instance, bosslogic’s eighth NFT sold for just shy of $28,000. Their next three NFTs went for between $11,000 and $18,200 each, before bidding pushed their twelfth sale to an outlier price of $39,708.

The same basic phenomenon played out among lower-reputation tiers of creators. For example, the artist known as pixlpa sold 19 total NFTs, each for between about $1,000 and $2,000. Those results cemented pixlpa in Foundation’s middle class of artists—significantly less successful than bosslogic and their high-reputation peers, but significantly more successful than low-reputation artists like madmonk, whose 12 sales generally closed at prices between $250 and $350 each.

The key finding is that the level of reputation impacts multiple measurable factors of success such as work-to-work selling price, mean sale price, number of NFTs sold, and maximum earnings, all of which mutually reinforce. The result is a kind of crypto predestination: in general, an artist’s odds of success on Foundation are set before they even mint their first NFT.

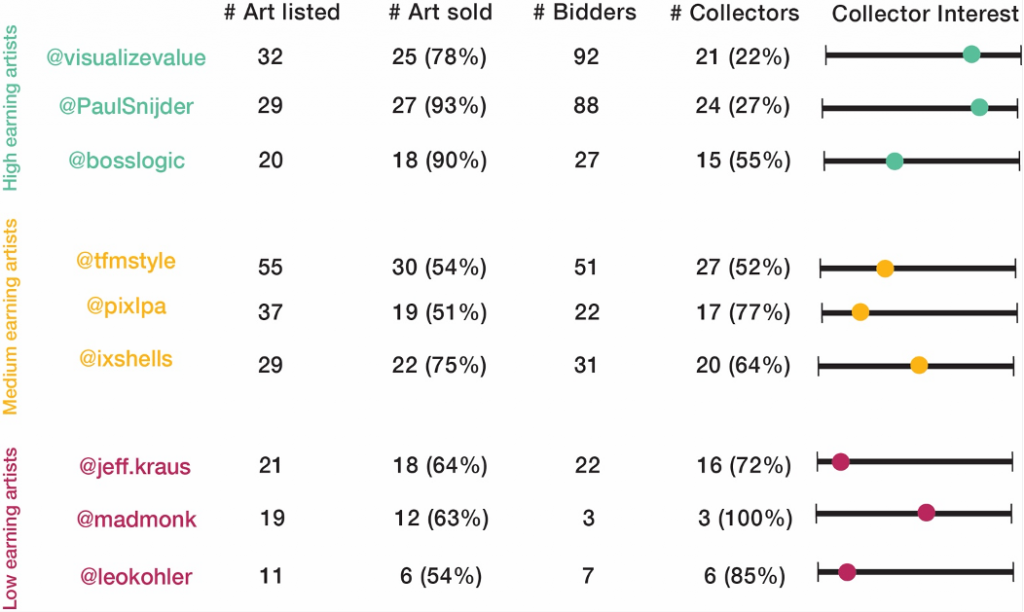

5. Even as NFTs Drew in the Masses, the Rich Still Ruled

Comparison of nine artists’ offerings, sales volume, bidder counts, and collector counts based on earnings level. Visualization by Barabási Lab. Courtesy of Barabási Lab.

Among high-, medium-, and low-reputation artists, the sales data diverged and converged in important ways.

All three groups exhibited a direct relationship between sales growth and growth in the number of bidders; the difference was that high-reputation artists attracted new bidders at twice the rate of medium- and low-reputation artists.

But there’s a twist: what remained “indistinguishable” among the three groups, Barabási and company found, was the rate at which the three groups of artists found new buyers.

In other words, even as high-earning artists sold more NFTs and attracted new bidders faster than everyone else, their collector base grew no faster. More people were competing for their work than for the lower-reputation groups, but about the same amount were actually winning those competitions (relative to comparable points in each group’s sales history).

This means that new works by high-reputation artists tended to be acquired over and over again by a few passionate collectors, often at outsize prices driven up by wider-spread bidding. Medium- and low-reputation artists, in contrast, tended to see their NFTs acquired at consistently lower prices among a more equally matched pool of buyers.

Drilling into the data clarifies the relationship. Among the 2,743 NFTs sold by the 180 top-earning artists with 10 or more transactions, about one-third were purchased by collectors who had previously bought work by the same artist. The roughly $4.5 million spent by these repeat investors made up more than 76 percent of the total sales value for this cohort ($5.9 million). The upshot? The minority of works acquired by top collectors sold for vastly more than the majority of works acquired by everyone else, even if we restrict our view to works made by a single artist.

The sales history of the artist PaulSnijder illustrates the point. During the study, nearly 62 percent of PaulSnijder’s earnings by value came from just six NFTs acquired by just three repeat collectors. Their other 21 sold works, each purchased by a different buyer, provided the remaining 38.5 percent of their earnings.

To Sum Up: A Mixed Bag

Since the beginning of the NFT markets’ surge more than a year ago, one of the central hopes has been that the technology’s disruptive potential and ethos of democratization would lead to more equitable results than the legacy art market. For the most part, Barabási and company’s research into Foundation douses those hopes in cold water.

True, the findings offer some good news. The first-mover advantage (Point #1) may have changed the careers of artists who were early to enter the field. The influence of follower count on sales success (Point #2) also reinforces that it is possible for crypto artists to organically grow a lasting career, fan by fan (if you focus on the right kind of fans).

However, the study’s takeaways about rich and poor artist clusters (#3), initial reputation (#4), and the importance of forming strong ties with a shallow pool of wealthy buyers (#5) will sound all too familiar to most veterans of the art establishment. In fact, they chime eerily well with Barabási’s findings in a 2018 study of the traditional art world, which determined that the trajectory of artists’ careers depended to an overwhelming extent on whether they began showing in “low initial prestige” or “high initial prestige” galleries and institutions. That die, too, was cast by the the strength of their relationships with other successful artists, wealthy buyers, and tastemakers.

In this sense, the early data on Foundation suggests that a high-quality social network is still the chief mechanism for advancement in crypto art. The most revolutionary aspect of NFTs is that they shift the responsibility for constructing such a network wholly onto the artist. Remember, a synonym for “gatekeepers” is “market makers.” To the extent that crypto eliminates the former, it also requires artists to become the latter by tirelessly advocating to boost their own standing. But if self-promotion isn’t foremost in an artist’s skill set, Barabási’s research indicates, then reputation might be even more confining in the crypto space than it is outside it.