The Art Detective is a weekly column by Katya Kazakina for Artnet News Pro that lifts the curtain on what’s really going on in the art market.

For a brief moment during the historic Macklowe Collection sale on November 15, a painting by Mark Rothko broke the auction record for the Abstract Expressionist painter, having hammered for $77.5 million at Sotheby’s.

“And selling, for a new world record for Mark Rothko, to Patti Wong, at $77.5 million,” auctioneer Oliver Barker announced from the podium, capping a lengthy bidding war between Sotheby’s chairman of Asia and two staffers in Hong Kong.

The room erupted in applause. The Rothko record had been unchanged since 2012, when a radiant canvas from the collection of David Pincus fetched $86 million. After Sotheby’s fees were added, the winning bid for the Macklowe Rothko hit $89.3 million, eclipsing that threshold.

But a few minutes later, the price on Sotheby’s website mysteriously dropped, to $82.5 million, and the Pincus Rothko bounced back into record-holding position.

Now you see it. Now you don’t.

Mark Rothko, No. 7 (1951). Photo courtesy of Sotheby’s.

When asked to clarify what happened at a post-sale press briefing, Barker mumbled something about “a conversion.” This didn’t make much sense. So, I followed up the next day, and was told that the incident was related to “a financial arrangement with respect to the work.”

It wasn’t the only high-profile lot in New York’s November auctions to have this kind of bait-and-switch. The same dynamic played out in the sale of the U.S. Constitution, and works by Francis Bacon at Phillips and Jean-Michel Basquiat at Christie’s, according to Artnet News’s calculations. In all cases, the works were sold to people who had placed irrevocable bids on them in advance—and received a discount in exchange.

When an investor makes an irrevocable bid, it means he or she has promised in advance to bid a certain sum, ensuring that the work sells, in exchange for either a set fee, a percentage of the upside if another bidder makes a better offer, or both. The details of such arrangements are tightly guarded and never confirmed.

Such deals amount to an insurance policy for auction houses, who often promise sellers a guaranteed price in order to win consignments. Sotheby’s was on the hook after giving a hefty guarantee for the Macklowe Collection and worked hard to outsource that risk in advance. (Think about it this way: If the auction guarantee is the insurance for the consignor, the irrevocable bid is the insurance for the auction house.) The stakes are high. Should a guaranteed piece fail to sell, it gets “burned” and goes into the auction house’s inventory.

Referred in shorthand as “IBs,” these deals can be lucrative for the investor, too. Should they win the lot, the fees will be subtracted from the final price they pay, even if it exceeds the bid agreed upon in advance. This amounts, essentially, to a special discount.

Francis Bacon, Pope with Owls, 1958. Courtesy Phillips.

Houses have become increasingly savvy about recruiting third-party backers over the past decade. Almost all the top lots in recent years had irrevocable bids. In the recent spate of New York sales, guaranteed lots accounted for 83 percent of the total value, a record high, according to a recent ArtTactic report, and many of those had IBs attached.

“You either get a check in the mail for the overage or you get the object,” said Evan Beard, head of private business services at Bank of America, which had many clients IB’ing the works this month. “Smart money thinks, ‘We are in a strong economic environment. Why not?’”

Many of these bets have been successful. Take the Rothko, whose backer is said to be Taiwanese billionaire Pierre Chen, president of Yageo Foundation and one of the major collectors of Western art in Asia. (A representative for Chen’s foundation said this information isn’t “fully correct,” but that it doesn’t comment on acquisitions.)

The eight-foot-tall canvas depicting three luminous rectangles, No. 7 (1951), was estimated at $70 million to $90 million and guaranteed by Sotheby’s as part of the Macklowe trove.

On the evening of the sale, three bidders went after the work, including Wong, who is known to work with Chen, said people familiar with the matter. As the hammer went down, those watching the event online could see “New auction record for Mark Rothko” appear on the screen.

Auction houses legally have to report net prices whenever the buyer receives a financing fee, subtracted from the total. In this case, Sotheby’s stood to make $11.8 million in fees on the undiscounted record price, but ended up paying $6.8 to the backer. Should the underbidder have made the same winning offer, they would have paid $5 million more than the guarantor did.

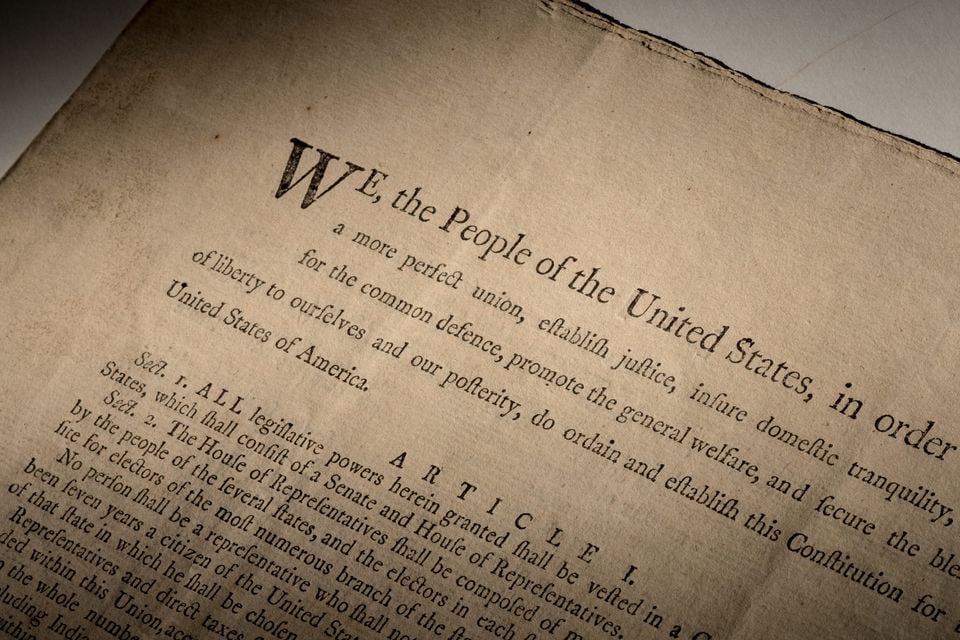

A first edition copy of the Constitution offered at Sotheby’s sold for $43.2 million, setting the record for the most expensive book, manuscript, historical document, or printed text at auction. Photo by Ardon Bar-Hama, courtesy of Sotheby’s.

While not illegal, such discounts highlight the inefficiencies—and ultimately, the inequality—of the auction process. It’s nerdy, geeky, dry stuff. It’s hard to follow and even harder to explain. Over the years, I’ve often heard, “It’s just rich people screwing each other over.”

Who really cares if anonymous buyers of Bacon’s Pope with Owls or Basquiat’s The Guilt of Gold Teeth got millions in discounts for placing irrevocable bids ahead of the sales? In each case, no one else was bidding against them.

It was a bit harder to ignore when the same thing happened again on November 18 during the sale of the U.S. Constitution, also at Sotheby’s. The official first printing of the 1787 document was estimated at $15 million to $20 million, with proceeds benefiting the Dorothy Tapper Goldman Foundation.

Sotheby’s had offered the seller a guaranteed price in advance. In the days before the auction, the manuscript sparked a revolutionary crowdfunding effort by a group called ConstitutionDAO, which raised about $47 million in cryptocurrency from more than 17,000 people in a quest to acquire the document. The group was extremely vocal about its war chest in the days leading up to the sale—and it started to scare other potential bidders off.

In the 11th hour, Sotheby’s found an IB’er—hedge-fund manager Kenneth Griffin—for the lot to ensure there would be competition. “Any client can make an offer to provide an IB on a work,” a spokeswoman said. “The IB is then only accepted if we obtain the seller’s approval and our vetting procedures are satisfied.”

Ken Griffin, CEO of Citadel, testifying in front of a Senate committee. (Photo By Tom Williams/CQ Roll Call)

Bidding for the document started at $10 million. Representing Griffin, Brooke Lampley, Sotheby’s head of fine art sales, swiftly jumped in with a $30 million bid.

For the next five minutes, it was a bidding war between Lampley and Sotheby’s head of private sales David Schrader, who was understood to be bidding on behalf of the disruptors. He went up to $40 million, double the high estimate.

At that level, the final price with fees would have been $46.2 million. Griffin raised his offer by another $1 million. All in, that was more than DAO had.

And so, he won. With added fees, the final price spiked to $47.4 million—a record, by far, for any manuscript at auction. Twitter lit up.

But some 20 minutes later, the price was revised down, to $43.2 million. “This is not the first time for such ‘revisions’ during the fall evening sales,” tweeted journalist Lee Rosenbaum. “What’s up?”

The only explanation is that Griffin received a $4.2 million discount in return for his irrevocable bid. The upshot: Had the DAO had access to the same deal, they would likely have been able to afford to buy the Constitution after all.

The scenario highlights the disadvantage of the underbidder’s position—especially when the world knows how much they have to spend. All their rival must do is bid a little higher than that threshold. And even though that person ends up bidding more, they ultimately pay less than the underbidder would because of the discount they coordinated in advance.

In other words, as one industry insider told me, “The underbidder gets fucked.” Sorry, DAO.

Update, November 20: An earlier version of this article incorrectly identified a Jackson Pollock from the Macklowe Collection and two Warhols as having a final price less than the one the auction house originally recorded.