A version of this story originally appeared in the fall 2019 artnet Intelligence Report.

The date on the New York Times in your hands is September 21, 1989. You’re on the subway home, trying to read the cover story about Mikhail Gorbachev purging the USSR’s Politburo, but Mayor Ed Koch’s plan to air-condition every train in New York hasn’t reached the one you’re on, and the heat is oppressive. Besides, you’re too anxious that the big deal you’re trying to close for your auction house may just blow up in your face.

There’s a new collector in Tokyo you need to call after tonight’s episode of Cheers ends. The fax he sent you at the end of his workday came through as nothing more than a smear of black ink, so it’s still unclear if his financials actually check out. He says he’s in real estate (naturally), and the way the Japanese market has been climbing for the past few years, there’s no telling how much he could spend in November if he’s serious. A single Van Gogh almost hit $54 million less than two years ago, and the Impressionist market has stayed so volcanic since then that you’re starting to dream the record could be broken again soon.

Problem is, you couldn’t find the collector’s card in your Rolodex today. Your assistant is driving to Florida, so you won’t be able to ask where it might have gone until she calls you from a motel room to check in tomorrow morning. Too bad those new “mobile phones” Motorola just released cost $3,000. Then again, holding a wireless electronic device up to your ear all day probably gives you cancer or psychosis, so the whole product line might be dead in a year or two.

Young buck Larry Gagosian cozying up to Leo Castelli in 1996. (Photo: Ron Galella Collection via Getty Images)

Speaking of psychosis, you wonder if Leo Castelli is losing his mind. At lunch today, you finally stopped by 65 Thompson Street in SoHo, where a few months back he started up a partnership with that 40-something LA shark Larry Gagosian. As if fighting with the other auction houses didn’t make your life difficult enough, Gagosian has been running around for the past few years acting like dealers have some kind of God-given right to compete in the resale market. What does he think, auction houses are going to start putting on exhibitions and offering works by living artists? Doesn’t he understand there’s a particular way of doing things in this business? Is the whole art world as we know it breaking down?

Fast-forward 30 years from this hypothetical day in the life and it’s clear that, in a way, the art world as it existed back then really did break down over the ensuing decades. That clubby handshake business where everybody knew your name has been replaced by a multibillion-dollar international industry.

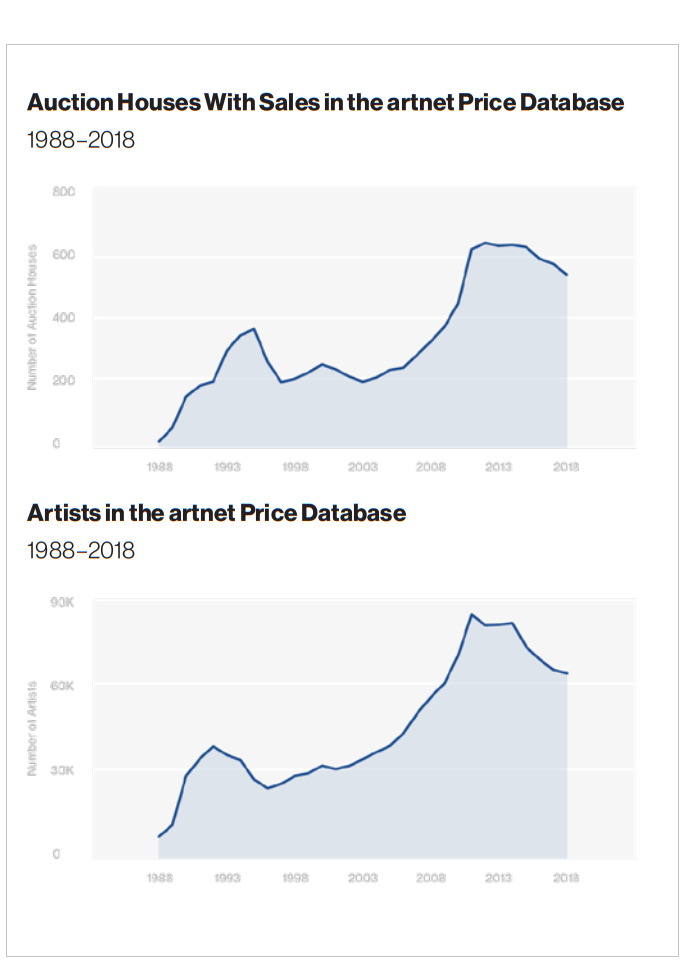

Today, that industry still has plenty of growing up to do, but the refinement process has begun. Consider that, in 1988, the Artnet Price Database tracked only 18 auction houses and about 8,300 artists. Over the next 24 years, those figures skyrocketed: By 2012, there were 632 auction houses and 90,275 artists. But, like any mature industry, it is now entering a period of consolidation after decades of expansion. Last year, Artnet recorded only 534 houses (a drop of around 16 percent from the high-water mark) and 71,621 artists (down 25 percent from the peak).

Still, the scale and contours of today’s art world would have been largely inconceivable to dealers, auction-house professionals, and collectors 30 years ago. Tastes have changed; non-Western economies have emerged as essential forces; and what was once a quaint cottage industry has become surprisingly corporate.

How was this transformation possible? Because three supposed truisms about the art market in the late 1980s have proved to be totally, completely wrong. Here, we explore the art-world myths that the rise of the art industry shattered.

Myth 1: Contemporary Art Will Never Be Popular

It has been said that “we are what we repeatedly do.” And based on the history of Artnet Price Database searches, we have become an industry ravenous for artists who started out in graffiti, vinyl toys, and (possibly staged) documentaries. The artists who saw the greatest increase in interested users over the past 15 years include KAWS (#1), Mr. Brainwash (#6), and Banksy (#7).

The rise of street art would no doubt be jarring to the dealers and collectors who were battling over Van Goghs in the late 1980s—as would the realization that what is driving the market is the ascent of young art in general. Most of the artists occupying this list’s upper reaches—40 of the top 50 names—were born in 1945 or later.

“The attention contemporary art gets today is what we were always hoping for,” says Thaddaeus Ropac, whose five international galleries grew from a single location in Salzburg opened in 1983. “It was once a small group of followers—we were happy with whatever number of visitors we got; we were happy about any small sale. But expectations today are on a totally different level.”

This trend toward the new is unmistakable in the data. For instance, of the 150 artists with the greatest increase in interested users since 2005, only one does not qualify as either postwar (which covers artists artists born between 1911 and 1944) or contemporary (artists born after 1945): the abstract color theorist Josef Albers (1888–1976). And he ranks seventy-third.

© Artnet Intelligence, 2019.

From today’s vantage point, it seems almost unbelievable that an era existed when contemporary work—which by its nature mirrors the issues and spirit of its age—did not enjoy such broad popularity. But Allan Schwartzman, chairman of Sotheby’s Fine Art Division, recalls that there was “no market for contemporary art” as recently as the late 1970s.

That all changed in the big-money 1980s, a decade during which, he says, art began “being filtered through the eyes of dealers” who largely championed “brash, bold, invincible” works by the likes of Julian Schnabel, Anselm Kiefer, and Robert Longo. The stock market crash of 1987 and the AIDS crisis threw a shroud over this Masters of the Universe mentality. The newly foreboding climate chimed with “a more introspective sensibility” shared by several important young artists whose work explored themes of mortality, intimacy, imperfection, and transience. From Robert Gober and Marlene Dumas to Rirkrit Tiravanija and Elizabeth Peyton, these artists “became the critical names in art, and often in collecting, in the decades that followed,” says Schwartzman.

As the number of wealthy individuals around the world grew from the late ‘90s into the 2000s, demand for artworks as symbols of refinement and success drastically increased—and contemporary art had inherent advantages over older art among all but the most moneyed of this ascendant class. That’s because, while the very top of the market became increasingly sophisticated about which pieces across different genres were worth significant price premiums, the rank-and-file rich gravitated to the next best and most available thing. And works by living (or recently dead) artists vastly outnumbered the classics.

From gallery dinners and studio visits to art-fair parties and biennials, the social incentives also heavily favored the contemporary, particularly as the amount of money flooding into the art business made these events more lavish and exclusive. This revenue boost translated into bigger budgets, greater ambition, and more robust marketing for successful galleries and artists.

Jay-Z and Marina Abramovic during the filming of Picasso Baby in 2013. Courtesy of Pace.

Before long, this expansion became a virtuous cycle. The more contemporary art bubbled over into the celebrity and mass-culture spheres, the more global brands were keen to partner with artists, and the more popular the artists became. Audiences can now encounter the work of fine artists in Jay Z videos, on the cover of Vogue, on Louis Vuitton handbags and Nike sneakers, in tequila ad campaigns, and in a thousand other venues far more visible than the traditional art context—and museums reap the benefits of this enlarged viewership.

Consider the fact that the Broad, the privately funded Los Angeles museum opened in 2015 by Eli and Edythe Broad, two of the most prominent collectors in the emerging class of contemporary mega-buyers, became one of the 15 most-attended American museums in its first year and has since grown its audience by 12 to 15 percent annually.

© Artnet Intelligence, 2019.

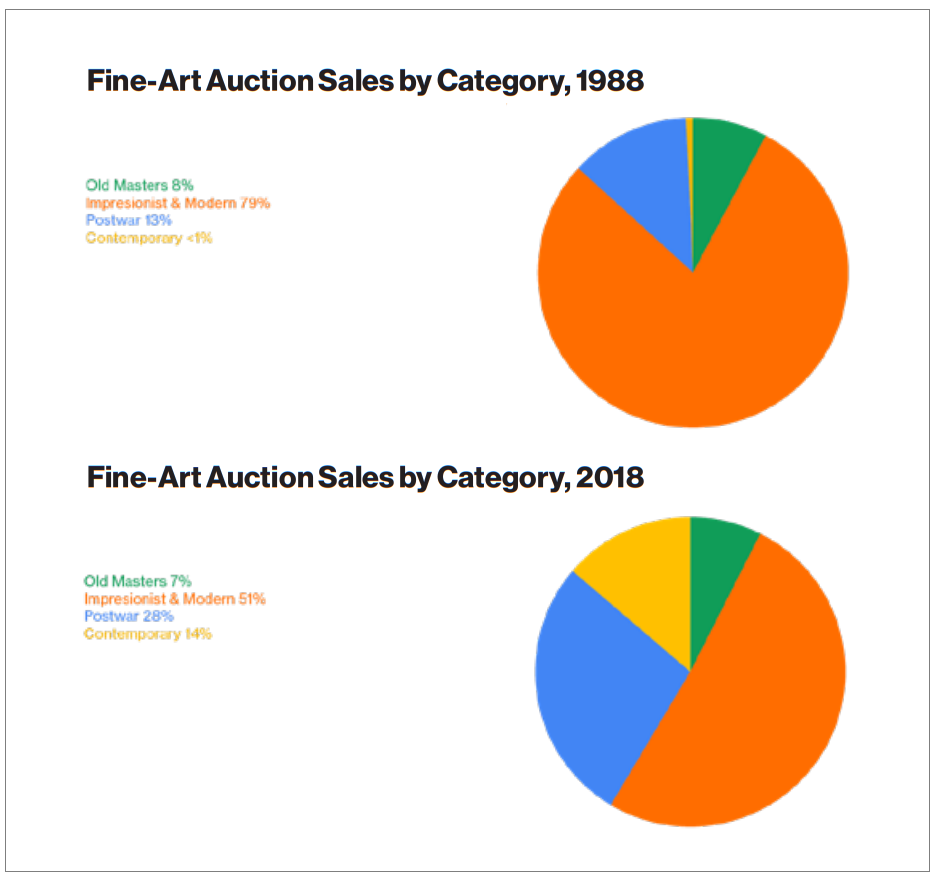

But does a huge gain in interest in contemporary art correlate to a major rise in sales? Inflation-adjusted auction results over the past 30 years certainly say so. Artists born after 1945 have seized more auction market share than any other segment in the past three decades, going from just 0.8 percent of total sales value in 1988 to 13.7 percent in 2018. That’s a gain of 1,700 percent.

Of the remaining categories of fine art, only postwar increased its market share over this time frame, from 12.5 percent in 1988 to 27.7 percent in 2018—a very healthy boost of about 120 percent, but an order of magnitude less than the game-changing growth of contemporary art.

Myth 2: Auction Houses and Art Galleries Are Different Things

Unpacking how and why sales gravitated toward the new lays bare some of the most fundamental changes in the art world since the late ‘80s. One of the biggest is the breakdown of the traditional border between auction houses and galleries. This development, which is arguably still in its early stages, has done much to transform the art business into a mature industry able to exploit the growing opportunities that lie before it.

© Artnet News Intelligence.

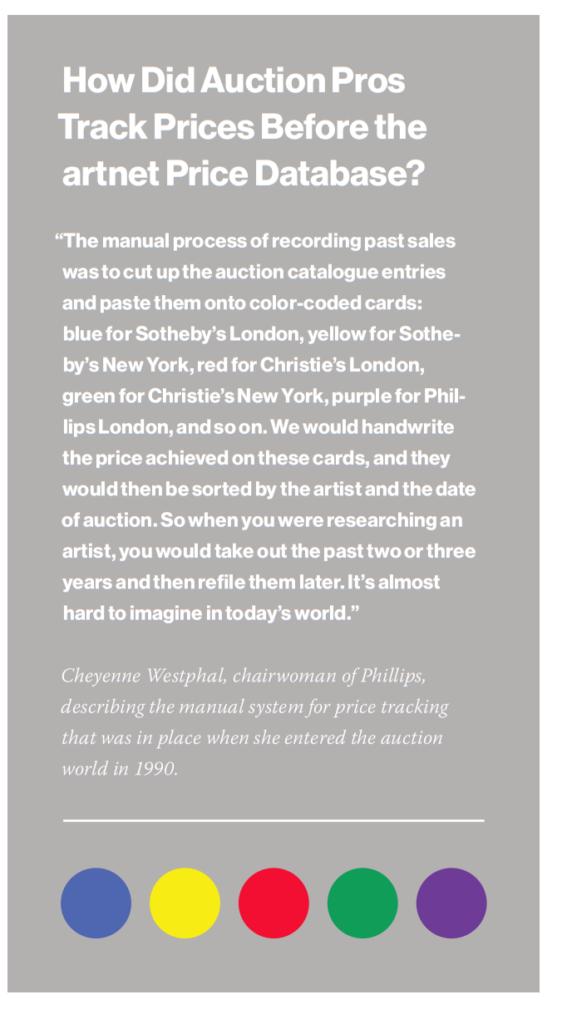

Thirty years ago, auction houses did not sell much contemporary art, which was considered the domain of art dealers. “When I joined the business, there was a rule that you wouldn’t offer an artwork by a living artist that wasn’t at least 10 years old, so nothing truly contemporary was offered in a postwar sale,” recounts Phillips chairwoman Cheyenne Westphal, who began her auction career at Sotheby’s in 1990. “That has changed dramatically.”

Among the biggest signs of this shift were the sales at Sotheby’s of objects and ephemera from Damien Hirst’s Pharmacy restaurant in 2004 and the 2008 “Beautiful Inside My Head Forever” auction of Hirst that, Westphal recalls, “bypassed any gallery system and did something you would call ‘direct to consumer,’ which was definitely not a term used in the art world at the time.”

Haunch of Venison, as seen from the street. Courtesy of Haunch of Venison.

The collapse of the distinction between auction houses and galleries occurred “step by step,” according to Ropac. He recalls Sotheby’s 1996 acquisition of André Emmerich Gallery, then primarily known for representing American color-field painters such as Morris Louis and Kenneth Noland, as an early milestone in a “slow process” through which the auction houses “tried to understand how they could get the best out of contemporary art.” Christie’s followed suit in 2007 by acquiring the international contemporary gallery Haunch of Venison, which then handled the likes of Richard Long, Bill Viola, and Rachel Whiteread.

The major houses eventually realized that running galleries that represented living artists was, in Ropac’s words, “a step too far, and stepped back” to, at most, operating exhibition spaces focused on private sales. But even this development was a meaningful one, and their consignments of contemporary works less than a decade old gradually moved from day-sale experiments to evening-sale fixtures over the past 10 years, at least in the United States.

Auction house employees man the phones during the “Beautiful Inside My Head Forever” sale at Sotheby’s, September 15, 2008. (Photo by Daniel Berehulak/Getty Images)

Dealers have been equally responsible for redrawing the art market’s borders. From Lucy Mitchell-Innes and David Nash, who exited Sotheby’s in the mid-‘90s, to Brett Gorvy, who departed Christie’s in 2016, major auction-house staffers have proved increasingly unafraid to pivot to the gallery sector, where new work from the studio is, in many cases, offered alongside secondary-market material premium enough to lead an evening sale.

This exploding distribution mechanism for contemporary work powered up the sector in a way that no competing category could match. It is no coincidence that the period during which the contemporary category made its greatest gain in the auction market—between 2004 (when contemporary accounted for 5.9 percent of all sales) and 2014 (14.9 percent)—maps almost exactly onto the one in which the number of worldwide art fairs ballooned (from 68 in 2005 to more than 220 by 2015).

So why is this increasing overlap between auction houses and galleries significant? Because each sector lacks what the other offers. Auction houses have corporate structures that allow them to scale up their operations on a global playing field and pursue long-term strategies despite changes in CEOs or ownership, but they lack access to fresh-to-market inventory. Galleries, on the other hand, have direct access to artistic production, but they are often passion-driven businesses operated by a charismatic founder (or founders) whose unique gifts and relationships cannot be easily transferred to successors. Combine the two, and you have something approaching the kind of vertically integrated corporate structure that has enabled companies in other industries to thrive in a global marketplace.

The facade of Gagosian, courtesy of Shutterstock.

We’re not there yet, to be sure, but this increasing hybridization shows no sign of slowing down. This spring, Gagosian announced the appointment of gallery veteran Andrew Fabricant to the newly created position of chief operating officer, the establishment of a 24-member advisory board of top salespeople, and, perhaps most notably, the creation of a new, separate business called Gagosian Art Advisory, LLC, led by Christie’s veteran Laura Paulson.

The move echoed the acquisition by Sotheby’s, three years earlier, of the art advisory firm Art Agency, Partners. For both high-end galleries and auction houses, it seems, the goal is to transform into 360-degree art-service juggernauts capable of handling a client’s every need, from private buying and selling to advising and estate planning to collections management and logistics. The race is on to see who will be best able to capitalize on the opportunities created by the growing—and increasingly global—market, ultimately becoming the LVMH of art.

Myth 3: There Is No Such Thing as Global Taste

It can be easy to forget how far the art market has come in Asia, and how fast. Patti Wong says that when she was appointed chairman of Sotheby’s Hong Kong in 2004, the city was still viewed as a “regional hub” whose business relied on “Chinese collectors buying Chinese things.”

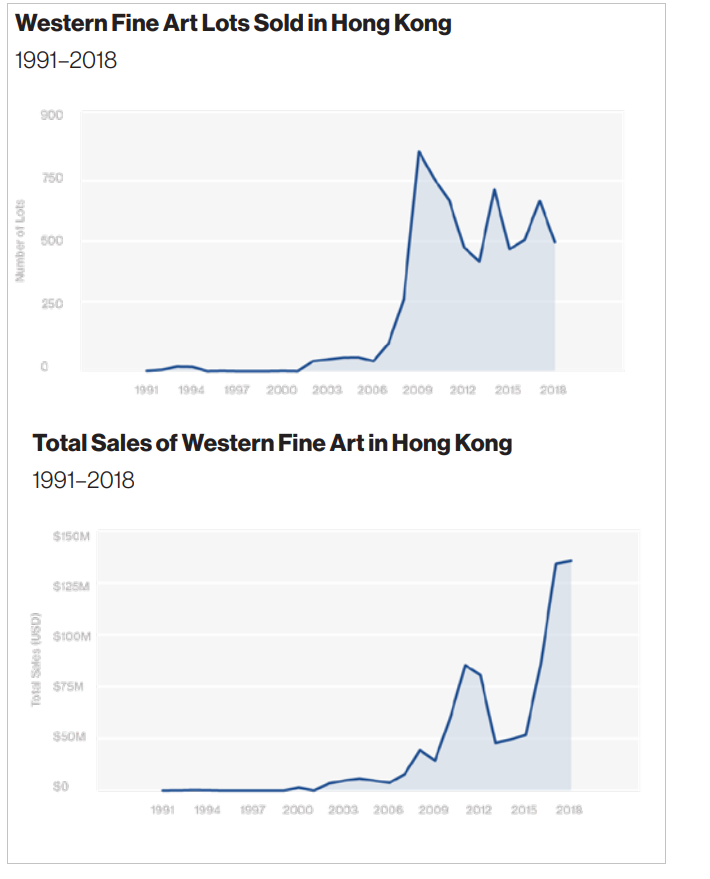

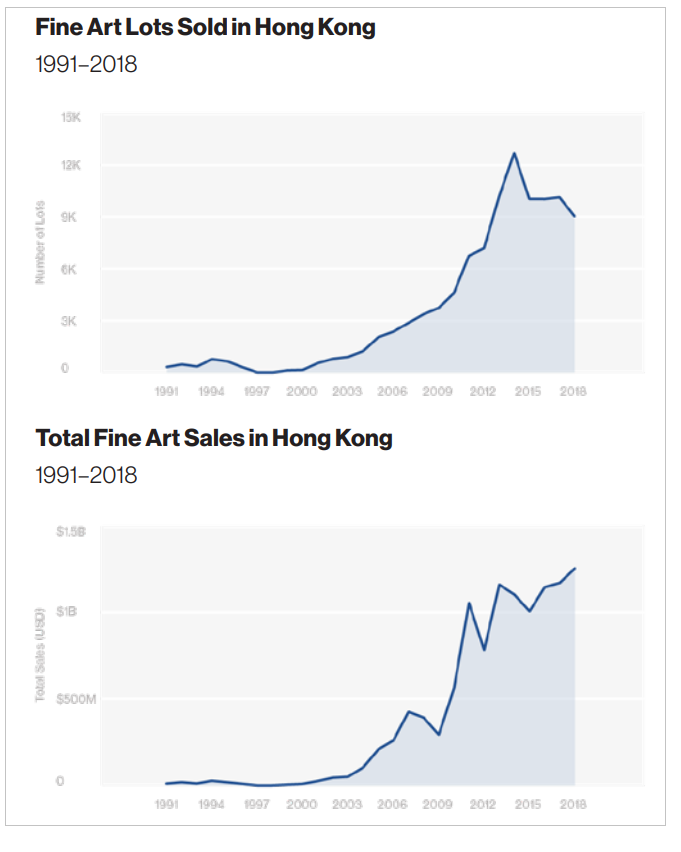

Indeed, from 1991 (when Artnet’s records for Hong Kong begin) to 2004, a grand total of just 124 works by Western artists sold at auction in the city, with a combined value of roughly $12.1 million. Fast-forward to 2018, and 498 Western works collectively brought in $132.7 million—almost 1,100 percent more in one year alone than Western art made in that first 13-year stretch.

Sotheby’s staff take phone bids during an auction at Sotheby’s in Hong Kong on April 3, 2018. Photo: Isaac Lawrence/AFP/Getty Images.

Just as telling, Wong contends that a “key message of the last 10 years has been the Asian buying power outside of Asia,” with sales in New York, London, and other Western markets being increasingly propelled by East Asian clients.

In this respect, fine art is aligned with other 21st-century businesses. The world’s major commercial and cultural economies are now intertwined to an unprecedented degree. It seems completely intuitive, for instance, that Marvel’s Avengers: Endgame grossed $178 million at the mainland Chinese box office over Labor Day weekend, or that it is as easy to find a Chanel store in Seoul as in Paris or New York.

© Artnet Intelligence, 2019.

Yet blue-chip Western art did not become blue-chip global art until the 2010s. It isn’t just that the preceding decades saw vanishingly few works by non-Asian artists come to auction in Hong Kong. The Western artists with strong presences in East Asia during this earlier era tended to be regional sensations with little to no strength under the gavel in other art-market hubs. In fact, even though he was Belgian by birth and ethnicity, one of these early top-sellers, the Modernist painter Adrien Jean Le Mayeur de Merprès, is normally included in Sotheby’s sales of Southeast Asian art today.

Looking strictly at paintings, the top-selling non-Asian talent in Hong Kong during the 1990s was British artist George Chinnery, whose renditions of Chinese subjects and scenes amassed about $124,500 at auction. The two decades since then have been led by Le Mayeur, who spent much of his career in Indonesia (and whose regional fame culminated with a museum in his honor in Bali). His paintings brought close to $20.3 million in the 2000s, and and have earned more than $43.1 million to date in the 2010s.

Le Mayeur aside, the sales rankings will look much more familiar to the average Westerner since 2010, after which point the internet, the identical international circuit traveled by socioeconomic elites, and other factors seem to have carried blue-chip artistic taste past an inflection point. The other top-sellers at Hong Kong auctions to date this decade are KAWS (nearly $37 million), Jean-Michel Basquiat (about $30 million), and Gerhard Richter (about $25 million).

Art Basel Hong Kong. Courtesy Art Basel.

East Asian collectors haven’t just become more international in an astonishingly short period of time. They have also become dramatically more discerning. Only a few years ago, Allan Schwartzman says, the predilection for “buying names rather than works” made the region’s buyers vulnerable to “various people in the market who took advantage [of them] to sell inferior works at healthy prices.” Those days are gone. According to Wong, “Asians rely on data,” typically researching not just previous sales prices but also how those prices landed relative to presale estimates so that they can make shrewd decisions.

The result? Hong Kong is rapidly approaching price parity with London and New York, if it is not already there. As evidence, Wong points to the results for Andy Warhol’s Mao (1973), one of the marquee lots in Sotheby’s Hong Kong’s Modern and contemporary evening sale in April 2017, which included Western artworks for the first time. The fiery red canvas sold for the equivalent of $12.6 million with premium—identical, in terms of US dollars, to the £7.6 million it brought at Sotheby’s London three years earlier and a gain of £2.4 million if the pound sterling’s drop over that period is taken into account.

This accelerated learning curve has equipped the art market as a whole to expand quickly and aggressively throughout East Asia. The inauguration of Art Basel Hong Kong in 2013 ushered in a new era for the territory’s relationship to Western galleries. Although Pace recently announced it would close its Beijing space, the globe-spanning gallery continues operating in (currently protest-ridden) Hong Kong, which also plays host to such heavyweights as Gagosian, David Zwirner, Hauser & Wirth, and Lévy Gorvy. Other high-tier galleries have set up permanent spaces elsewhere in the region: Perrotin and Lehmann Maupin in Seoul; Sean Kelly in Taiwan; Blum & Poe in Tokyo.

KAWS, Holiday (2019). Photo: courtesy of AllRightsReserved.

This development has been largely driven by East Asia’s first-generation inheritors of mega-wealth. A large proportion of this demographic grew up in families that collected in more traditional categories, such as regional antiquities or Chinese ink paintings, and were educated (and culturally embedded) in the West during some of their formative years.

“It’s quite regular that we have a collector in his late 20s or early 30s buying seriously at auction—and not just one or two, but in volume,” says Westphal. “It’s a generation of collectors very used to absorbing information, very keen on finding out what is going on and what is going to be the next big thing, and driving that, as well.”

© Artnet Intelligence, 2019.

Having two generations of collectors with roots in East Asia has made a colossal difference for the Hong Kong auction market. In 1991, Hong Kong houses in the Price Database combined to sell 313 fine artworks (by both Asian and non-Asian artists) for $10.9 million. In 2018, a total of 9,017 works changed hands to generate almost $1.4 billion in sales, a 234-fold increase in 27 years.

Wong says that understanding the data-driven mind-set of East Asian collectors has allowed Sotheby’s to, in her words, move beyond “what people expected: the Warhol Mao, [Yoshitoma] Nara, [Yayoi] Kusama” and begin offering high-quality works by artists with solid market profiles but no sustained prior presence in Asia. Last April, for example, Sotheby’s Hong Kong set new world records for both Ethiopian-born, New York-based painter Julie Mehretu and New York-based sensation KAWS.

This is why Wong says Asian collectors “no longer just follow the data but are part of making the data” that charts the global market’s path—a development many would have considered unthinkable 30 years ago. So the next time you hear a colleague or client gripe that the art market is doomed to keep repeating the same mistakes, feel free to remind them that an awful lot tends to change in three decades.

A version of this story originally appeared in the fall 2019 artnet Intelligence Report. To download the full report, which has juicy details on the most bankable artists, a survey of what top collectors are buying and why, and a deep dive into the market for African contemporary art, click here.