The latest of Dr. Clare McAndrew’s annual reports sponsored by Art Basel and UBS portrays an industry whose ingenuity and main engines for growth seem to have stalled out.

However, the study also delves into under-examined segments of the market that offer food for thought about what, if anything, might finally propel sales of art and collectibles beyond the limits of the 2010s.

If you’ve read any of the three previous editions of The Art Market, the headline findings in its latest iteration will feel familiar. The report estimates sales across all sectors of the art market to have reached $64.1 billion in 2019, a decline of five percent versus the prior year. That figure is roughly on par with McAndrew’s approximation for 2017 ($63.7 billion), as well as within striking distance of her estimate for the trade’s all-time high of $68.2 billion in 2014 (when her report was still being produced in conjunction with TEFAF).

In other words, the market has retrenched, but the larger takeaway is that it’s been unable to crack the $70 billion ceiling for as long as anyone has been checking.

Several other metrics showed incremental upward or downward movement, but reinforced that the macro picture of 2019 looks broadly similar to most other recent years. The US, UK, and China (in descending order) remain the world’s three largest art markets by value, still accounting for more than 80 percent of the trade’s worldwide sales (82 percent, to be exact); dealer sales increased to an estimated $36.8 billion overall—a new peak, but only a two-percent rise versus 2018; and online sales comprised an estimated $5.9 billion, or nine percent of the market’s full value.

(As a reference point, this means e-commerce would have to nearly double in the next 12 months to surpass the €10 billion target for 2020 projected in McAndrew’s 2014 TEFAF Art Market Report.)

The methodology used for the report’s main sections remains largely unchanged from years past, which will once again spur split opinions from observers. On one hand, it makes The Art Market 2020 a clean comparison to past editions, reinforcing that the long-term trends on display reflect shifts in the business rather than shifts in McAndrew’s process. But its data still carries most of the same caveats as in previous years, such as its melding of fine art, decorative art, and antiques into a single stream (unless otherwise noted), as well as the fact that its dealer-sector figures largely come from an anonymized survey that aims to collect a representative cross-section of the world’s private sellers via 6,500 potential respondents—only about 1,100 of whom ultimately participated. (Although this 17 percent response rate exceeds the average for such surveys, and the report has gradually fleshed out its appendix over the years, the individual dealer responses remain unavailable for review.)

Still, while attention will almost undoubtedly gravitate toward the report’s central sales data, arguably its most intriguing aspects arise from supplementary analyses of Art Basel and UBS’s respective areas of expertise: art fairs and high-net-worth individuals.

Art Basel Miami Beach 2019. Photo: Courtesy of Art Basel.

Fair Play

Using the aforementioned dealer survey (methodology skeptics, take note), the report concludes that sales at art fairs totaled an estimated $16.6 billion in 2019, essentially steady from the prior year. This figure would mean fairs accounted for about one-quarter of the overall art market by value—a proportion that would have been unfathomable 20 years ago, when there were only about 55 such events scheduled around the world.

But it isn’t just the amount of fair sales that have changed. It’s also their timing. Although 64 percent of transactions by value ($10.6 billion worth) are still finalized during the events themselves, about 15 percent of works by value ($2.5 billion worth) are sold before the fairs even open, and the remaining 21 percent of deals ($3.5 billion worth) don’t close until after the fairs do. While this distribution may not surprise anyone who’s participated in an art fair recently, it would underscore that this sector of the art economy has become more fluid—and harder to capture with traditional art-fair sales reports—than ever.

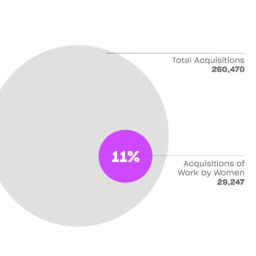

Based on data from sources beyond the dealer survey, the expanded timeline for deal-making doesn’t seem to encourage risk-taking. McAndrew relays that about two percent of “star” artists were responsible for about one-third of the works on view in art-fair stands last year. Those star artists also still demonstrated a huge gender disparity; only about 21 percent were female—a depressing parallel to what we’ve seen in museum collections.

However, the relative conservatism of the works on view isn’t hurting attendance at many fairs. Quite the opposite, in fact.

The report estimates that 1.2 million people visited art fairs in 2019, up four percent from 2018. Art Basel Hong Kong showed the strongest year-over-year surge among major fairs, boosting attendance by 10 percent (and highlighting why the cancelation of this year’s edition due to coronavirus comes as such a blow). The Armory Show shrunk the most among this cohort, shedding 12 percent of its visitor figures from the prior year (perhaps owing in part to the structural problems discovered at its venue days before its 2019 edition was set to debut).

Several fairs have also shown incredible growth over a multiyear period. Among the major players, Frieze London, Frieze Masters, and Masterpiece have each amped up attendance by between 62 percent and 75 percent since 2013. Many smaller fairs have done even better over that span, with Art Beijing, the 1-54 Contemporary African Art Fair in London, ZONAMACO, and others all at least doubling their attendance.

And yet, consolidation (finally) seems to have set in. The report found that the sector showed a net loss of 14 art fairs between 2018 and 2019, suggesting the possibility that the winners may be cannibalizing the losers.

Fairgoers take pictures of Maurizio Cattelan’s Comedian, for sale from Perrotin at Art Basel Miami Beach 2019. Photo by Sarah Cascone.

Changes in Demand

As in past editions, The Art Market 2020 includes data about who’s buying art, antiques and luxury objects, not just who’s selling them. Through UBS, McAndrew queried 1,300 high-net-worth individuals (HNWI)—defined as people with investable assets greater than $1 million—about their collecting activity over a two-year period. Each respondent hailed from one of seven markets: the US, UK, France, Germany, Hong Kong, Taiwan, and Singapore. And the results were intriguing.

First, the respondents’ ages often seemed to make a much bigger difference in their habits than their nation of origin. Millennials (here defined as people aged 23 to 38) outspent every other generation, acquiring an average of $3 million worth of art and collectible objects in the preceding two years. In contrast, Baby Boomers in the sample (aged 55 to 73) averaged less than $500,000 of spending each.

Although the most popular purchases among survey respondents were jewelry, gems, and watches, fine art ranked second among all age groups—but largely because of the millennials’ impact on the overall results. About 79 percent of millennial respondents acquired fine art regardless of their home country, including 82 percent of those in the US. Millennials were also the only generation where the majority of respondents acquired at least one artwork, one design object, and one antique during the two-year period in question, suggesting they are more omnivorous in their taste for the finer things.

Motivations for buying varied substantially by age group, too. Roughly three-quarters of millennials said that financial considerations impacted what, and how much, they bought; only about one-third of Baby Boomers said the same. Millennials were also the most enthusiastic about churning their collections, with 71 percent saying they’d sold at least one piece, compared to only about one-third of Boomers. And yet, across all ages and countries of origin, 52 percent of respondents admitted that more than half of the value of their collection was in an off-site storage location, leaving readers to wonder whether older HNWI simply own more artwork than their juniors, or whether they’re more investment-minded than they’re letting on.

Gender differences among these wealthy buyers were pronounced, as well. Despite the fact that men outnumbered women roughly two-to-one among respondents, women tended to be higher-spenders on average at the upper tiers of the market. About 34 percent of female HNWI spent more than $1 million on art and objects, versus only about 25 percent of men. The average female HNWI also had a larger collection than the average male, with about one-third of women holding more than 100 works.

In total, the survey strongly suggests that, if the art market is ever going to break out of its box, it would do well to look to the young and to women of all ages. And if sellers make that pivot, there’s no telling how much else could change besides the industry’s total sales revenue.