Artnet News Pro

Fractional Ownership Is Turning Art Into Stocks—But Not Everyone Stands to Make a Profit

Retail investors are buying bite-size pieces of Banksys and Picassos in the hope of a payday. Are they getting played?

.")

Retail investors are buying bite-size pieces of Banksys and Picassos in the hope of a payday. Are they getting played?

Katya Kazakina

ShareShare This Article

ShareShare This Article

This article first appeared in the spring 2022 Artnet Intelligence Report. Download the full magazine here.

Last year, Sygnum bank in Switzerland issued 4,000 shares of an unusual asset: a 1964 painting by Pablo Picasso.

Each share of Fillette au béret—a painting of a young girl in a bright blue cap—was valued at CHF1,000 ($1,070). The pitch to potential clients was this: The sale of each segment would be recorded in a smart contract on the blockchain. The painting, meanwhile, would be stored in a freeport until it was sold for a profit.

More than 60 investors jumped at the opportunity last year.

“What before only very few people could own in full is now available to many in a fractionalized manner,” Mathias Imbach, chief executive officer of Sygnum, which specializes in digital assets, said at the time.

Pablo Picasso, Fillette au béret (1964). Photo Seraina Wirz / © Succession Picasso / 2021, ProLitteris, Zürich.

The transformation of this charming Picasso from mantelpiece trophy to tradable asset marked the beginning of a much bigger trend—one that has the potential to change the way the art market operates and fundamentally expand who can participate.

“It’s the natural outgrowth of the financialization of the art market,” said art advisor Wendy Cromwell. “There’s been so much reporting on wealth generation through art that the financial community took notice and jumped on the bandwagon. It’s not about art. It’s about money.”

Since the onset of the pandemic, the notion of art ownership has been radically expanding beyond the physical. And so owning and trading fractions of artworks and collectibles—a 10th of Magic Johnson’s sneakers, a hundredth of a Warhol, a thousandth of a Picasso—moved from the fringes of the art investment conversation to the epicenter.

Artist Pak sold 266,445 shares of the NFT project Merge for $91.8 million on the platform Nifty Gateway in December. A month earlier, more than 17,000 people joined forces as a decentralized autonomous organization (DAO) to raise $47 million in a bid to buy an original printing of the U.S. Constitution at Sotheby’s. And Masterworks, a start-up that allows investors to purchase shares in Basquiats and Kusamas for as little as as $20, is now regarded as a Silicon Valley “unicorn,” valued at $1 billion.

PleasrDAO bought an NFT of a meme to launch the infamous Dogecoin cryptocurrency. (Photo by Yuriko Nakao/Getty Images)

In some ways, the art world is merely reflecting broader trends. The pandemic left scores of middle-class professionals at home with spare time and stimulus checks burning holes in their pockets. Dollar investors who plowed their savings into GameStop, AMC, and other meme stocks emerged as a market-moving force. Now, the same dynamic is playing out in the art industry, which has been discovered by crypto millionaires and decentralized collectives.

Think of it as El Dorado. Everyone wants to get rich—fast. And the entry point is relatively inexpensive. “It’s like buying a ticket to a movie,” said Alberto Mugrabi, a scion of a major art-collecting and -trading family. “It’s an investment to go dream.”

But do these small-scale investors actually stand to make real money? And is the traditional art market prepared for a future in which masterpieces are divided into shares and traded like stocks and bonds?

***

Whether or not the art world is ready, it’s happening. Newbies are going head-to-head with art-market stalwarts. Pak’s $91.8 million NFT price surpassed top auction results for blue-chip heavyweights like Jeff Koons and David Hockney. The bidding war between ConstitutionDAO and billionaire hedge-fund manager Ken Griffin resulted in an auction record for a printed text of $43.2 million. Around these new players, a whole cottage industry is growing. Art funds that tokenize blue-chip works are on the horizon. Art appraisers have never been busier.

The First Printing of the Final Text of the United States Constitution on display during a press preview at Sotheby’s on September 17, 2021 in New York City. (Photo by Alexi Rosenfeld/Getty Images)

Masterworks, meanwhile, has emerged as one of the biggest buyers in the market. Last year, the company bought about 65 works of art to the tune of more than $300 million, according to its SEC filings. It shopped at Christie’s, Sotheby’s, and Phillips (both at auction and privately); top galleries such as White Cube and Skarstedt; and directly from major players like the Mugrabi family and billionaire Steven Tananbaum, the filings state. Many of its appraisals are done by Winston Art Group.

Last year’s loot included five Basquiats bought for a combined $61 million and nine paintings by Kusama ranging for between $1.9 million and $4.8 million each. Masterworks also picked up Joan Mitchell’s 12 Hawks at 3 O’Clock (1960) for $14.2 million from High Fashion Concepts, a limited liability company operated by the Mugrabis.

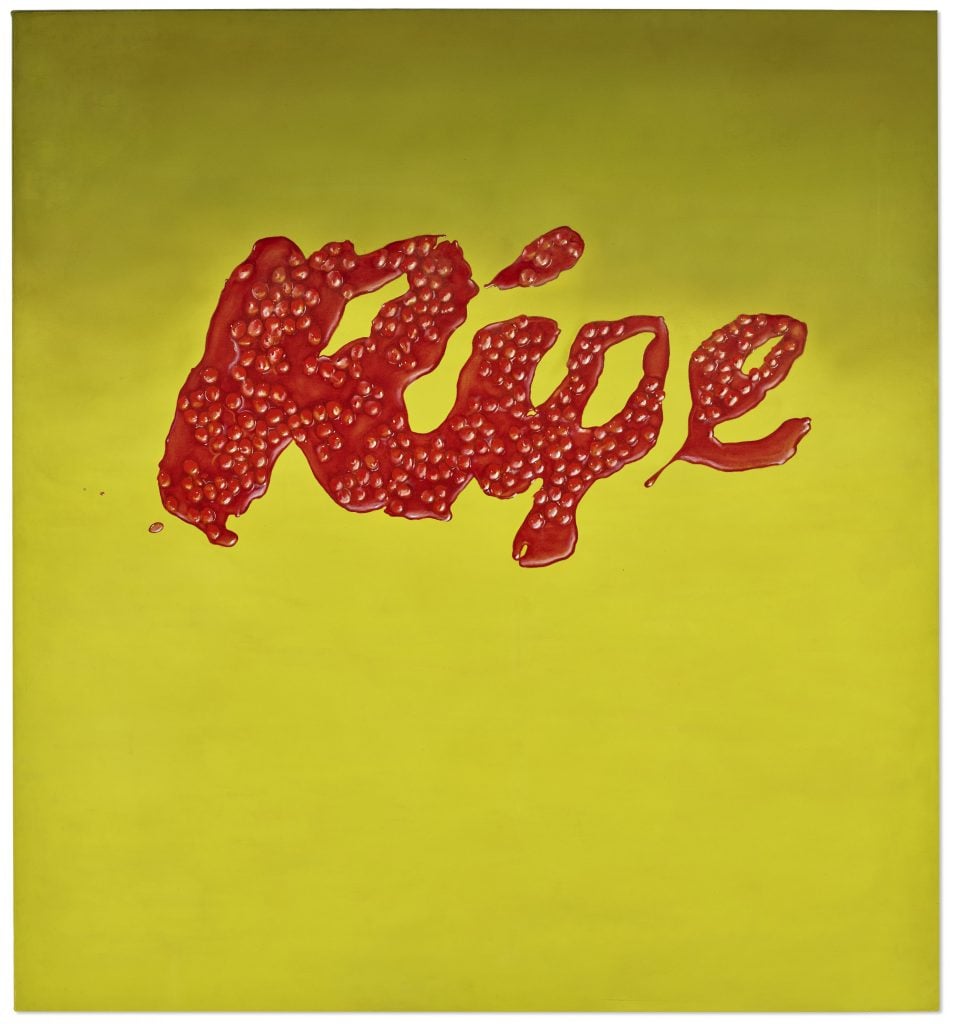

During the November auctions in New York alone, Masterworks dropped more than $60 million at Christie’s, snapping up works including Banksy’s Sunflowers from Petrol Station (2005), Ed Ruscha’s Ripe (1967), and Christopher Wool’s monumental untitled canvas spelling HA AH (1990).

Masterworks adds a roughly 11 percent fee to the purchase price and then offers these works like IPOs, effectively flipping them to investors. The company charges a 1.5 percent annual management fee and earns 20 percent of any profit realized when the works are sold. Masterworks declined to respond to a detailed list of questions about its business.

So far, Masterworks has sold only three artworks from its portfolio. One of them is George Condo’s painting Staring into Space (2014–15), which fetched $2.9 million at Christie’s Hong Kong in December (it had been purchased for $1.6 million in 2020). Investors in this offering could expect a 32 percent return after fees, the company said.

In many ways, the shift from the single owner to the fractional owner boils down to two factors: psychology and technology.

Art used to be the ultimate trophy, something for the ultra-rich to behold and display. But the rise of retail investors is changing the power dynamics. Masterworks now has 360,000 investors, most of whom own shares of artworks without ever seeing them in the flesh.

George Condo, Staring Into Space (2014–15). Courtesy of Christie’s Images, Ltd.

“Fractional-share interest in art is best suited for people who are focused on art as an asset class and may not have the time or interest to engage with art, artists, or the art community more broadly,” said Dan Desmond, executive director of the Blue Rider Group at Morgan Stanley.

Masterworks founder Scott Lynn did not want to be interviewed for this story, but his representative’s explanation for that decision spoke volumes. The company, the rep noted, wants to limit its exposure to the art world (and art publications). “Our investors aren’t art people,” he said. “They are just investors.”

Art resonates with this audience because it is an asset that doesn’t correlate to stocks, bonds, or other financial instruments. It’s also seen as a hedge against inflation. And while investors aren’t interested in going to exclusive gallery dinners, fractional art ownership is a fun novelty investment—buzzy NFTs or historic works by Picasso are more exciting to discuss over cocktails than index funds.

“It’s not a purely financial play,” said Drew Watson, head of art services for Bank of America’s private bank. There is an “intellectual and social” appeal to “being able to talk with your friends about owning a piece of the work of art that’s been securitized and is part of your overall investment allocation.”

Watson’s team has seen an uptick in curiosity among clients over the past year. Inquiries are coming from an emerging wealth segment—often, the newly crypto-rich—as opposed to old money or those who made their fortunes in hedge funds and real estate. (Those kingpins can afford to collect the actual artworks.)

The irony is, of course, that in this new fractional art world, the people least interested in art could end up owning some of the most coveted paintings and sculptures.

***

Fractional ownership of blue-chip art was a tiny niche as recently as two years ago. To be sure, collectors and dealers have often formed syndicates to buy artworks, and cash-strapped museums sometimes pool funds for joint acquisitions. But this represents a whole new level, with a considerably lower price point and an incomparably larger pool of people able to buy in, thanks to new technology.

Consider the case of Javier Lumbreras, the founder of investment company Artemundi, who paid $3 million for Fillette au béret at a Swedish auction house in 2016. The Picasso painting had impressive provenance: It passed through the hands of legendary Swiss art dealer Ernst Beyeler, Los Angeles County Museum of Art cofounder Sydney R. Barlow, and Swedish collector Bertil Neuman. Lumbreras planned to hold the work and resell it for a profit.

Then last year he saw an opportunity he couldn’t have imagined half a decade earlier. As NFTs exploded and cryptocurrencies surged in popularity, Lumbreras partnered with Sygnum to tokenize the painting. It was listed at CHF4 million ($4.3 million), 38 percent more than Lumbreras bought it for. Investors were offered 4,000 shares, each priced at CHF1,000.

An interior hallway of the ARCIS freeport in Harlem. Image courtesy of ARCIS ©2018.

Effectively, investors bought Lumbreras out for a profit (though his company retains 10 percent of the shares). He stands to make more over time: The company charges a onetime fee of 8.9 percent of the original purchase price, or $89 per token, for taking care of the work, loaning it out, and storing it at a Swiss freeport (shareholders can visit whenever they like). If the company sells the painting within five to eight years, it will make an additional 2.5 percent commission.

According to Lumbreras, these complex transactions wouldn’t be possible without blockchain technology. Investors can use any currency, fiat or crypto, to buy a securitized ERC-20 token, based on the Ethereum blockchain, representing their stake. “In a fund you have to sign 6,000 pages of paper,” he said. “Here, you are done with a click.”

It’s democratization—but only, Lumbreras admitted, to a degree. To buy a token, investors must pass know your client and anti-money laundering requirements and have at least CHF500,000 ($540,540) in liquid assets. The minimum investment is five tokens.

“We are not trying to appeal to the traditional art-collecting world,” Lumbreras said. “It’s for people who want to invest in a very safe asset.”

For Blanca De Castro Infante, a wealth manager at a Swiss bank, investing in a fraction of the Picasso was an experiment. Part of her goal was to gain firsthand knowledge about this hot new investing trend. “There’s a lot of hype there,” she said. “The motivation was to try my own medicine.”

While she enjoys going to galleries, De Castro Infante said she is a “laywoman” when it comes to art. “I like art, but I don’t collect myself. I don’t have the means to. So I thought: Well, just go for it.”

***

Lumbreras’s talking points—fractionalization leads to transparency; art is a safe investment; prices for blue-chip art are bound to go up—are echoed by many of the key players behind these initiatives. But not everyone agrees.

“Investors should expect lower returns on art compared with other types of investments,” Bank of America’s Watson said. “The art market is volatile, illiquid, and heavily influenced by collecting trends.”

Ed Ruscha, Ripe (1967). Courtesy of Christie’s Images, Ltd.

Michael Moses, an economist who examined 50,000 repeat art sales over the past 50 years, warned that only 0.5 percent of the works had the compound annual return of 100 percent or more. What about a more modest 10 percent? “My guess, it’s less than 10 percent of all works,” Moses said.

Melanie Gerlis, the author of the 2014 book Art as an Investment? A Survey of Comparative Assets, concurred. “When I think of the costs and the time of making art, owning art, and all the things we know about the weird hierarchy and the black magic that goes on behind the scenes to make an artist successful,” she said, “there’s no way it’s as good an investment as a tech stock.”

You won’t hear much about these risks from fractional-art specialists like Masterworks (unless you read the fine print).

Instead, on its website, Masterworks highlights the impressive historical appreciation of carefully chosen repeat sales by artists in its portfolio. The price of a cheerful flower painting by Warhol increased by a factor of 90 over 28 years; a record $110 million Basquiat was originally purchased for $19,000, representing a windfall of more than 5,200 percent over 33 years.

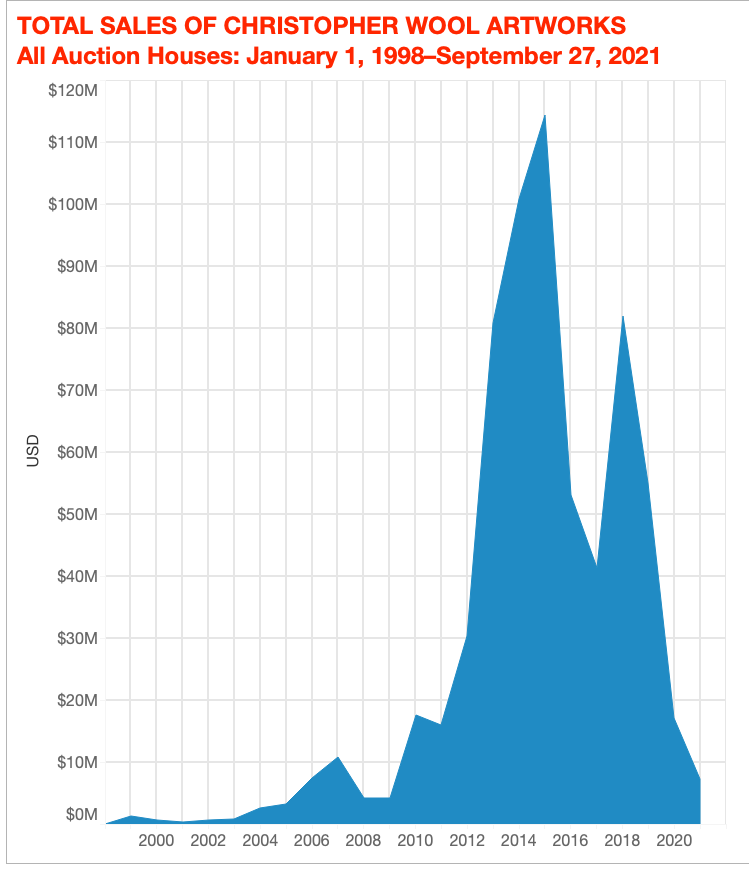

The reality is more complex. Take Wool’s HA AH, recently offered to investors on the Masterworks platform. The company bought the work for $7 million at Christie’s in November; it was the sole bidder. The price represented a 40 percent dip since 2014, when the same painting fetched $10.7 million at auction.

© 2021 Artnet Price Database and Artnet Analytics.

The chart of comparable “word” paintings by Wool on the Masterworks website omits any disappointing results, including unsold works. While Wool’s auction sales declined 63 percent in 2021 from their peak in 2015, according to the Artnet Price Database, Masterworks presents an ascending trajectory, charting 31 percent growth since 1990.

There’s a certain information and access asymmetry between Masterworks and its investors. For example, the company is a frequent financial backer of guarantees to auction houses, receiving fees for taking on the risk and occasionally buying the works when no one else bids. Those fees have amounted to about a 12 percent discount that wouldn’t be available to other buyers. It is unclear if and how those savings are passed onto investors.

In addition, Masterworks often receives preferential payment terms. While most buyers are required to pay within 30 days of the purchase (and top clients get 90 days), Masterworks has secured as long as six months—enough time to sell the shares off to investors.

***

So far, the fractional ownership marketing strategy seems to be working. The next step is scaling up. Lumbreras said Sygnum is pitching tokenized artworks to “very conservative money managers and banks.” Masterworks is said to have approached money managers at major investment banks to add fractional art to their diversified offerings to clients, according to a person familiar with the plan.

How soon this becomes a reality is anyone’s guess.

“It’s still very early days,” Watson said. “They would need more of a track record to be palatable for the large financial institution.”

Tokenized artworks are likely to appeal to individual investors and family offices before banks. “Short-term, I can’t see banks including these tokens as an asset class,” said De Castro Infante. “It’s not their métier. We have analysts who look at solvency and liquidity metrics to see whether the bond is good or bad. We have traders who look at demand and supply of commodities. But we don’t have this knowledge about art.”

Still, those who have been in the art investment game for years see the arrival of new investors as validation.

“Everyone has been talking about art as an asset class for so long, but now it’s really happening,” said Elizabeth von Habsburg, managing director of Winston Art Group. “People are seeing that it’s a financial instrument for better or for worse. They realize there’s more they can do with art than buy it, hold it, or loan against it. They are making the pie bigger.”

This article first appeared in the spring 2022 Artnet Intelligence Report. For more on how DAOs can work for the art market, a detailed breakdown of the leading companies in the fractional ownership space, and our data-led analysis of last year’s auction results, download the full magazine here.