Auctions

Ahead of a Marathon Auction Week, Data Shows Skyrocketing Valuations and Changing Tastes at the Market’s Peak

Three data-driven takeaways from pre-sale figures for the major May auction cycle, dating from 2000 to 2018.

Three data-driven takeaways from pre-sale figures for the major May auction cycle, dating from 2000 to 2018.

Tim Schneider

ShareShare This Article

ShareShare This Article

Get ready to witness eye-watering amounts of money spent in less time than it takes for you to refresh Twitter. It’s spring auction week in New York, when Christie’s, Sotheby’s, and Phillips hold their marathon sales of Impressionist, Modern, postwar, and contemporary art.

We’ll no doubt learn lessons from the eventual results of these sales, but consignments and pre-sale projections also provide a valuable look into how consignors and top professionals in the auction sector read the market at this critical moment in the annual calendar. So as a preview of the week’s major fine art sales, which kick off this evening, I dug back through the pre-sale data from the stalwart auctions of the May sales cycle, from 2000 to the present, to see what meaningful themes would emerge.

Before unveiling the takeaways, let’s clarify the analytical boundaries, shall we?

With that context in mind, here are three major conclusions from the data.

The chart below shows the total value of pre-sale estimates for the main sales in May dating back to 2000.

The data tells us that this season’s pre-sale estimates are down somewhat from the peak in 2014. But they’re still nearly four times as high as they were 19 years ago.

(Note: To compensate for the fact that estimates are always given as a range, we’ve chosen to add up the low and high estimate of each sale to create a “total estimate.” For example, if Christie’s projected an auction would reach $100 million to $200 million, the sale would appear in this chart with a total estimate of $300 million.)

This picture represents a dramatic expansion of the market in less than two decades. But it also begs an obvious follow-up question: What’s been a bigger drive of this growth, the number of artworks coming to auction, or the price per work?

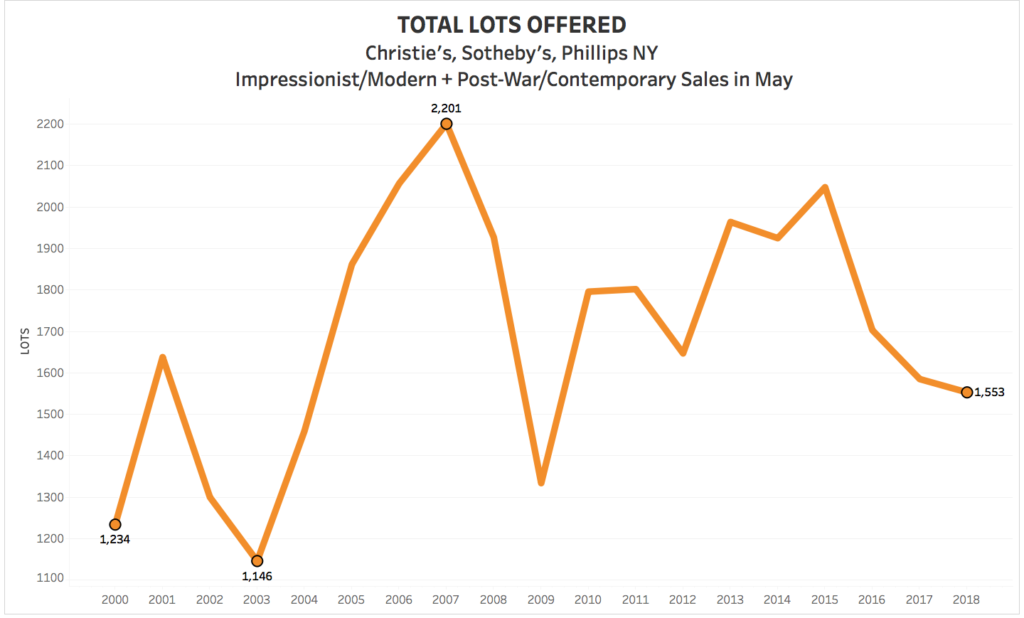

Here’s a look at the auction volume, meaning the number of lots offered, in the same sales over the same period. (Worth noting: Christie’s did not hold any postwar and contemporary auctions in May 2000, so their re-entry in 2001 creates an automatic one-year jump in practically every chart we’ll review here.)

Overall, we reached peak auction volume for this sales cycle in 2007, when the three houses combined to offer about 2,200 lots. That number was about 78 percent higher than in 2000.

In comparison, this May’s total of 1,553 lots qualifies as an increase of only about 300 artworks, or roughly 25 percent, over our starting point 18 seasons ago.

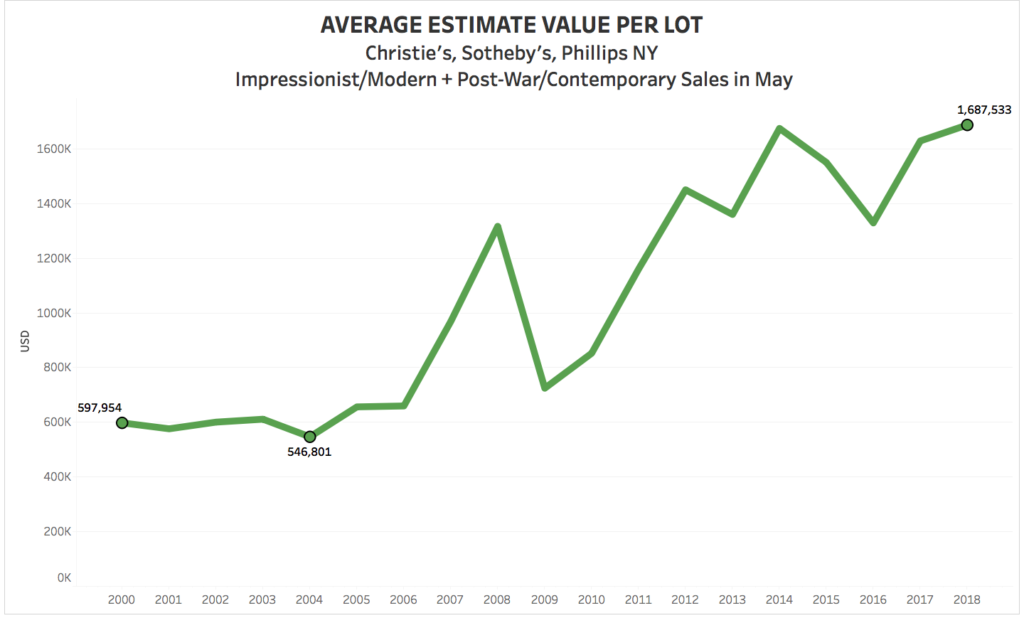

So if we’ve seen a nearly 400-percent rise in pre-sale estimate value from a roughly 25-percent rise in the number of offered works, it doesn’t require a bolt of divine inspiration to conclude that artwork at auction has been getting significantly more expensive.

How much more expensive, you ask? Turns out the average pre-sale estimate for a work in this cycle is now almost three times pricier than it was at the start of our sample period—a swing from about $600,000 in 2000 to almost $1.7 million per piece this May.

Granted, this isn’t because every single object hitting the auction block is multiple times the price it would have been 18 years ago. Since we’re using average values, huge growth at the top of the market moves all of the findings aggressively toward the higher end.

At the same time, the distortion is exactly the point. It may not be a revelation that prices have risen much further and faster than the number of artworks being offered in this sales cycle, evidencing the auction market’s often-discussed move toward the apex of the socioeconomic pyramid. But it is illuminating to be able to quantify the size of the shift.

The data also points to some more surprising conclusions, as well.

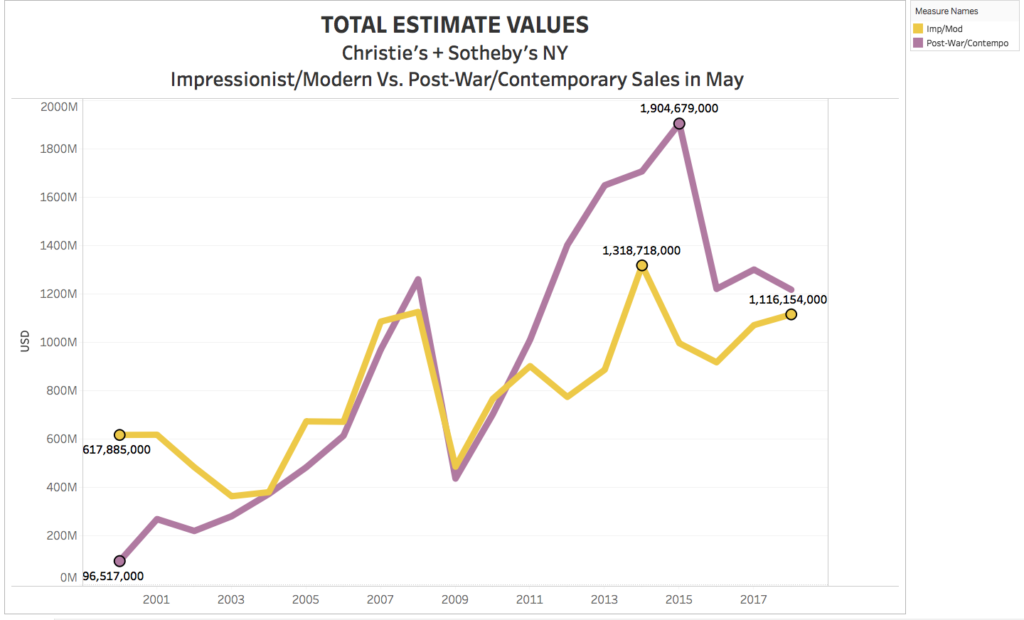

For years, it has been an article of faith that the art market’s growth this millennium has owed largely to the explosion of interest in postwar and contemporary work. Although that has largely been true based on May sales past, recent evidence suggests that the paradigm is shifting.

Below is a chart comparing the total pre-sale estimate values for May’s Impressionist and Modern auctions versus postwar and contemporary auctions since 2000. Because Phillips’s “20th Century and Contemporary” sale category muddies the waters in this showdown, we’ve strictly used data from Christie’s and Sotheby’s more clearly defined auctions.

Although postwar and contemporary work has come in higher on the pre-sale estimate scale than Impressionist and Modern over the past 18 seasons, the category’s total has also dropped farther and faster since 2015. Next week, the two categories will be separated by only (“only”) about $100 million—the closest they’ve been to one another by this metric since 2010.

As always, past performance is not indicative of future results. The tables could easily turn again next May. Still, three years makes a trend, and this one bears watching.

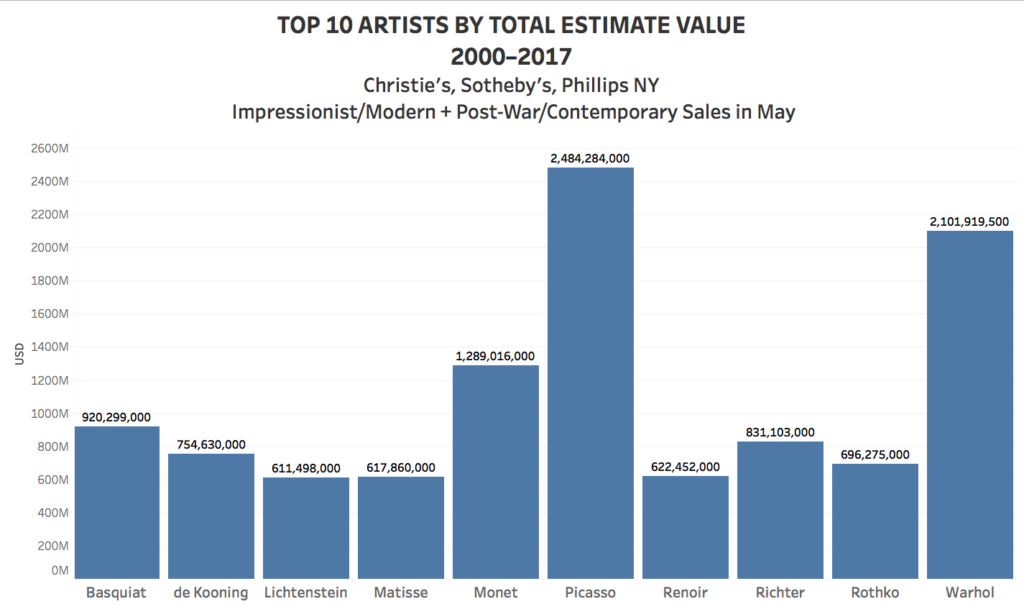

The chart below breaks out the top 10 artists by total pre-sale estimate value, meaning the combined low and high estimates for all works offered in the main May auctions by the Big Three houses from 2000 to 2017.

The heavyweight artists who made the chart range from Roy Lichtenstein, at a relatively humble $611 million, to Pablo Picasso, destroyer of worlds, at a total of nearly $2.5 billion. Between them stand three Impressionist/Modern artists—Henri Matisse, Claude Monet, and Pierre-Auguste Renoir—and five postwar/contemporary artists—Jean-Michel Basquiat, Willem de Kooning, Gerhard Richter, Mark Rothko, and Andy Warhol.

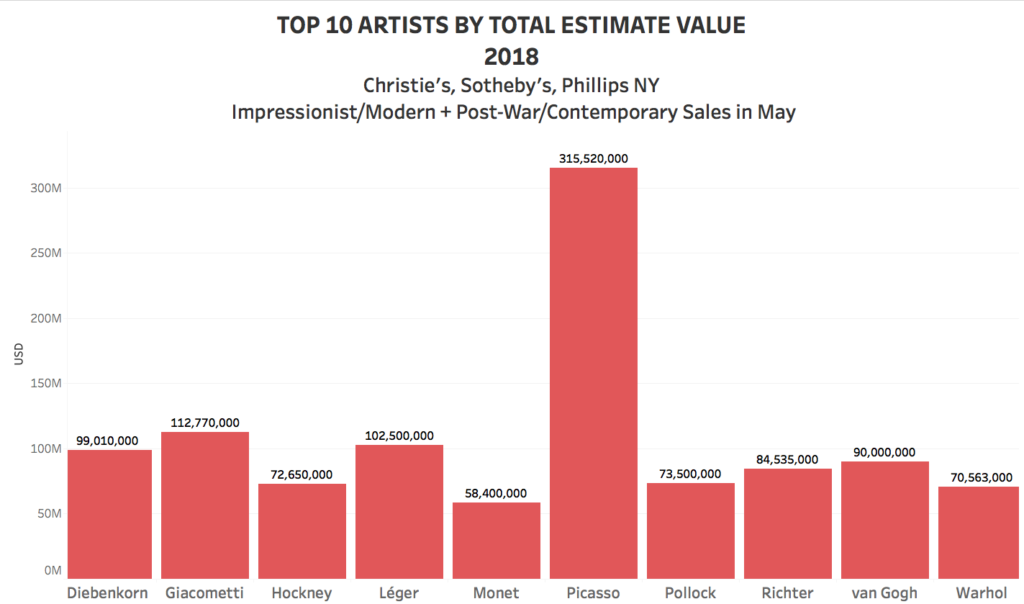

Now, let’s look at the list for this May alone.

We see two Modernists reappear from the 2000–2017 chart: Monet at the low end ($58.4 million), and Picasso once again reigning supreme from on high ($315.5 million). But only two other stars from the previous chart return: the postwar duo of Richter and Warhol.

The other six artists on this year’s list are all new to the top 10 conversation. Alberto Giacometti, Fernand Léger, and Vincent van Gogh represent the older guard, while Richard Diebenkorn, David Hockney, and Jackson Pollock emerge from the postwar crowd.

Could this be a one-year anomaly? We can’t totally rule it out. Statistically speaking, estimates in a single sales cycle will always be more prone to random events than estimates aggregated from numerous cycles. (In this case, for example, Diebenkorn’s presence is likely due to Barbara and Donald Zucker’s collection of 22 works by the artist being sold at Christie’s—an event unlikely to be repeated anytime soon.)

Still, it’s at least worth noting that we’re seeing more flux than stability in this year’s top 10, regardless of the era in which the artists lived and worked. Nor do these artists represent sudden plot twists that we would never expect to see in this context. All of them are among the bluest of the blue chippers.

In concert with the market’s demonstrated shift toward Impressionist and Modern works shown in takeaway two above, then, the data suggests that this season’s wealthiest collectors are mostly looking to different icons—or, more precisely, looking to unload different icons—than in past years, no matter their period of interest. Time—and sales results—will tell if shifting demand matches the shifting supply.