The Art Detective is a weekly column by Katya Kazakina for Artnet News Pro that lifts the curtain on what’s really going on in the art market.

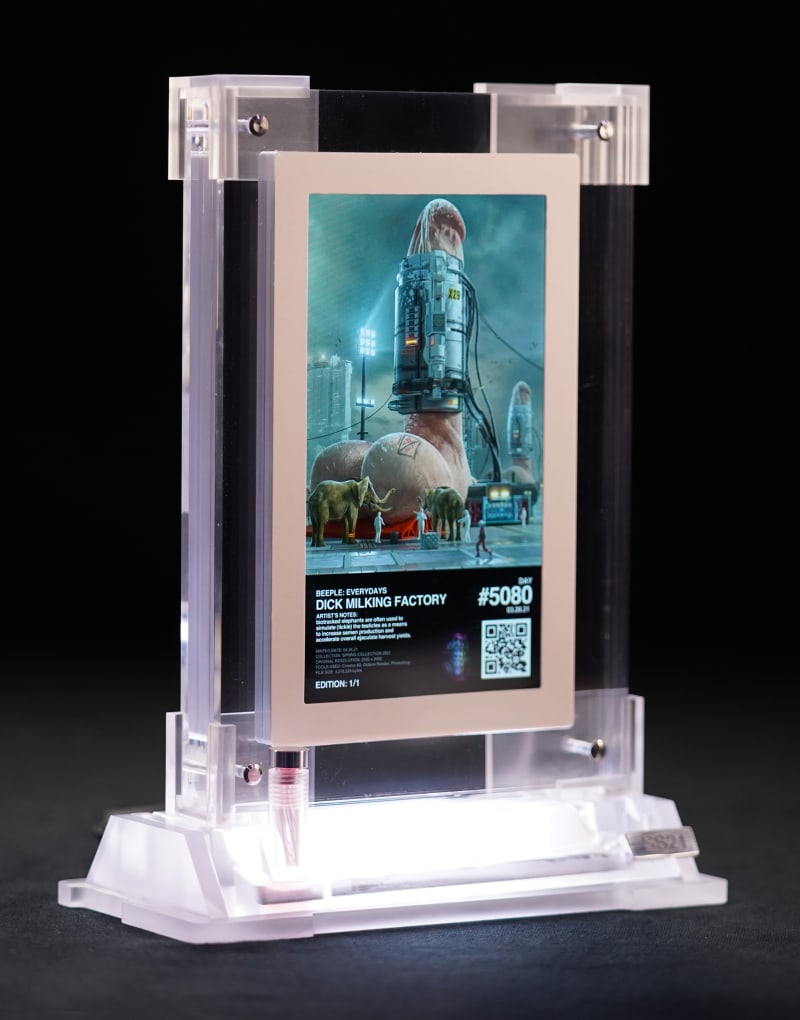

Beeple’s NFT artwork Dick Milking Factory isn’t for everyone. At the center is an erect, rocket-size penis supported by a pair of giant testicles and catered to by testicle-tickling elephants. Yes, you heard me.

But crypto investor Ryan Zurrer simply had to have it. When it came up for auction on Nifty Gateway in May, he outbid 10 competitors and took it home to the tune of $505,050.

“Some people would consider it quite revolting,” Zurrer told me when we spoke by phone last month. “But I found it really interesting because it was a joke internally for our family office.”

Zurrer made a fortune investing in crypto assets. His invite-only, multi-family office, called Dialectic, focuses on the challenges and opportunities presented by crypto wealth. He thought Dick Milking Factory was a good investment.

“We were going to put Dick Milking Factory to work, milking yield,” Zurrer said.

Here’s how it works: He borrows against the NFT in U.S. dollars (most recently, he got a $750,000 loan), then uses the capital as a lender in a riskier, higher-interest decentralized finance transaction. “This provides me a margin between what I am receiving as a lender and what I am paying as a borrower on a high-quality asset like a Beeple,” Zurrer explained. “The joke is how much money we are making on this.”

It sounded like a tongue twister: Dick. Milk. Yield. But it also made sense that NFTs would now be treated like a mortgage on a house—or, gasp, a Picasso.

Beeple’s Dick Milking Factory from “Everydays.” Courtesy of the artist and Nifty Gateway.

Still, I had a hard time imagining, say, Bank of America issuing a loan on Dick Milking Factory. (They won’t. More on that later.) Such transactions remain firmly outside of the traditional banking system. There, in the world of “defi” (which stands for “decentralized finance”), CryptoPunks, Bored Apes, and Beeple Everydays are viewed as blue-chip assets, tradable and monetized. And a growing number of investors are using them to play the yield game.

“It’s a space that’s attracting a lot of venture capital interest,” said Evan Beard, head of specialty segments, including art lending, at Bank of America private bank. “We’re watching the space. We’re excited by it. We’re interested in it.”

For now, Bank of America isn’t lending against NFTs, Beard said, adding that financial institutions are “years away” from entering the nascent segment. (By comparison, traditional art financing, a market that is expected to hit $30 billion this year, seems almost old school. That field has grown tremendously over the past decade as financiers found a way to extract value from the art trophies hanging on their walls and stored in freeports.)

NFTs are a small but highly visible slice of a bigger cake. “It’s a gateway into a much broader potential intangible property lending world,” Beard said.

Think domain names, avatars, and gaming items. The idea that all those gems and gold my son used to collect and mine as a Minecraft-obsessed 10-year-old can be potentially tokenized, monetized, and used as collateral for loans seems wild. But it’s happening.

“Our end goal is to enable people who accumulated largely digital wealth be able to translate it into real world money,” said Josef Je, co-founder of PWN AG, a Swiss start-up that facilitates lending against digital assets. “Ultimately our target market isn’t art NFTs, but it’s the one that gets the most attention.”

Evan Beard, head of art services at Bank of America. Photo courtesy of Sony Pictures.

PWN is part of a growing niche of new platforms that create smart contracts to store collateral in escrow on the blockchain. They provide the infrastructure but don’t take on any financial risk or custody of the items. Founded six months ago, PWN raised $1 million in seed money from Zurrer’s Dialectic and other angel investors, Je said. Another startup with a similar aim, Arcade, announced $15 million in seed financing in December.

The nascent market is small, but the growth is exponential. NFTfi, a South Africa-based company, created smart contracts for $14.4 million in NFT loans so far this month, up from just $12,000 a year and a half ago, according to Stephen Young, the company’s chief executive officer. The total volume of loans on the platform reached $55.5 million over 18 months, he said.

Yuga Labs LLC, 101 Bored Ape Yacht Club (est. 2021). Courtesy of Sotheby’s.

Its top asset, a collection of NFTs known as Bored Ape Yacht Club, generated 188 loans totaling $12.6 million.

The interest is sky-high, in part because of the price volatility of the collateral. For example, the average percentage rate (APR) for Bored Apes loans was 46 percent, according to NFTfi. But it can be even higher. Much higher. Loans for Hashmasks, an NFT collection of mishmash characters, had an APR of 131 percent, according to NFTfi. Banks, on the other hand, have charged their top clients as little as 1 percent on art loans.

During this peer-to-peer phase, lenders are typically individuals and venture capitalists. And the loan period is short—often between a week and 90 days—which makes the rates feel more reasonable. NFTfi’s top lender accounted for $11.7 million in 700 loans, reaping about $700,000 in earned interest, or 88.4 percent APR, the company said.

“The interest rates are also high because of the limited access to liquidating the collateral,” Je said. “Our loans don’t protect the lender as much. The default of the loan is that you get your hands on the collateral.”

One of the Hashmaks. Courtesy of Hashmasks.

Not surprisingly, default is high—and often attractive. Many lenders “loan to own,” hoping for a default because they can get Apes or Autoglyphs at a distressed price.

“A lot of this is a game,” Beard said. “It’s completely divorced from the type of lending that we’ve grown up in Western civilization, where people don’t want to default on things for both moral and reputational reasons.”

The unabashed financial calculation that’s part of the NFT collector’s mindset is the biggest difference between this brave new world and the traditional art market.

It’s taken decades for the collecting community to warm up to borrowing against Picassos and Warhols. While the financiers like Michael Steinhardt and Dan Sundheim have been savvy about extracting value from their collections, most people don’t advertise doing it.

“It’s not something they would talk about at dinner,” Beard said. “They don’t want to be viewed as sort of a crude financial beast using their art in this way.”

The NFT space is different. Trading is endemic. And so there’s no stigma in using a CryptoPunk as a financial instrument. NFT collectors “treat their NFTs as almost a form of currency,” Beard said. “And the aesthetics are secondary to the financial element.”

(Photo by JUSTIN TALLIS/AFP via Getty Images)")