The Art Detective

What Is the World’s Top Mega-Gallery? We Crunched the Numbers—and No, It’s Not the One You Think

We examined the size of galleries' rosters, their combined square footage, and more to determine who emerged from the pandemic on top.

We examined the size of galleries' rosters, their combined square footage, and more to determine who emerged from the pandemic on top.

Katya Kazakina

ShareShare This Article

ShareShare This Article

The Art Detective is a weekly column by Katya Kazakina for Artnet News Pro that lifts the curtain on what’s really going on in the art market.

A Patti Smith performance. A boutique hotel in a Scottish village. A Miami warehouse featuring jaw-dropping immersive installations with an admission price steeper than most U.S. museums. Book and magazine publishing. Restaurants and bars. C-suites and financial departments.

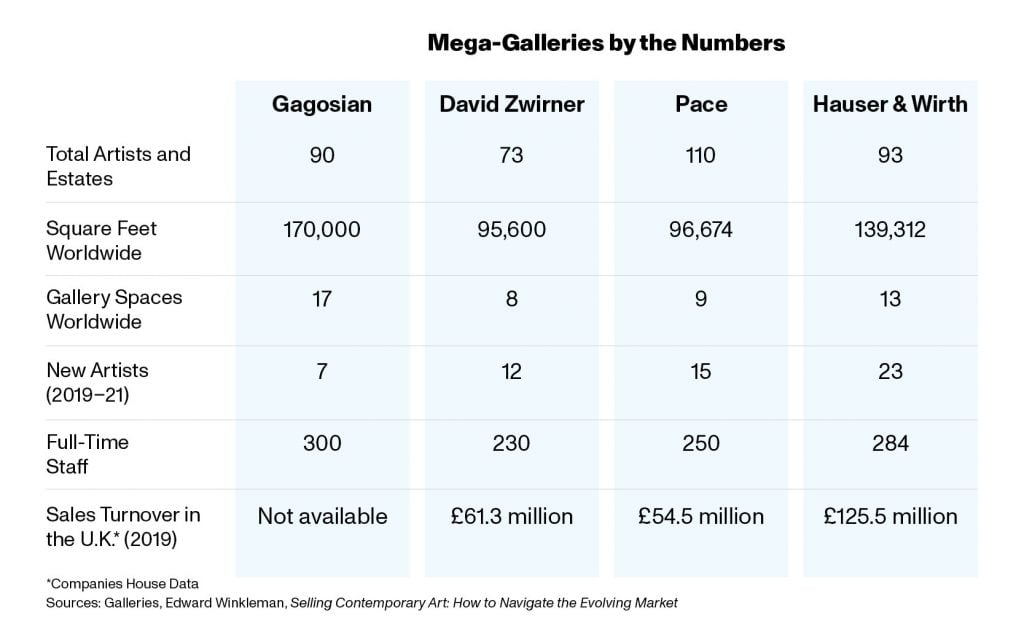

These are just some things Gagosian, Zwirner, Pace, and Hauser & Wirth galleries do as they compete for art-world domination. Combined, the Big Four represent almost 400 artists and occupy more than 330,000 square feet (that’s almost six football fields), according to an analysis by the Art Detective.

No longer mom-and-pop operations, art galleries are evolving into global brands, with new initiatives and branches announced weekly, it seems. As the world emerges from the pandemic, these conglomerates are forging full steam ahead to make up for a year of lost revenue—and grab market share.

Global gallery sales fell 20 percent to $29.3 billion in 2020, with the largest ones (turnover of $10 million or more) reporting the steepest decline, of 31 percent, according to the latest UBS Art Basel art market report.

But who occupies the top spot after a year of reckoning?

Larry Gagosian and Leo Castelli in 1996 in New York City. (Photo by Ron Galella, Ltd./Ron Galella Collection via Getty Images)

Conversations with experts and a close examination of the galleries’ growth reveal that while Gagosian, considered by many to be the industry leader, may be slowing down, there is no clear successor to take its place—yet.

“At this moment, the concept of the top gallery is almost obsolete,” said Barbara Bertozzi Castelli, art historian and widow of Leo Castelli, the top dealer of the previous era.

Instead of a pyramid, the top of the market may become a field dominated by several powerful players, said art adviser Megan Fox Kelly. “And the metrics for measuring the top become not only about sales volume and gallery space but more about influence—who is making the greatest impact? Who is innovating effectively? Where do prominent artists most want to be? And who is building the most effective team to support their artists and collectors?”

***

Larry Gagosian, 76, has been the undisputed leader of the past two decades, with sales topping $1 billion, according to the Wall Street Journal, and a gallery empire upon which the sun never sets. His mega-gallery model has become the template—to emulate and disrupt—for the younger generation of rivals: David Zwirner, Marc Glimcher, and Iwan and Manuela Wirth, who are all in their 50s and hungry.

“Gagosian has been the top gallery for so long, and now it’s a little unclear,” said Natasha Degen, chair of art market studies at the Fashion Institute of Technology in New York. “It seems optically, that these other galleries looking to grow are vying for the top spot more aggressively.”

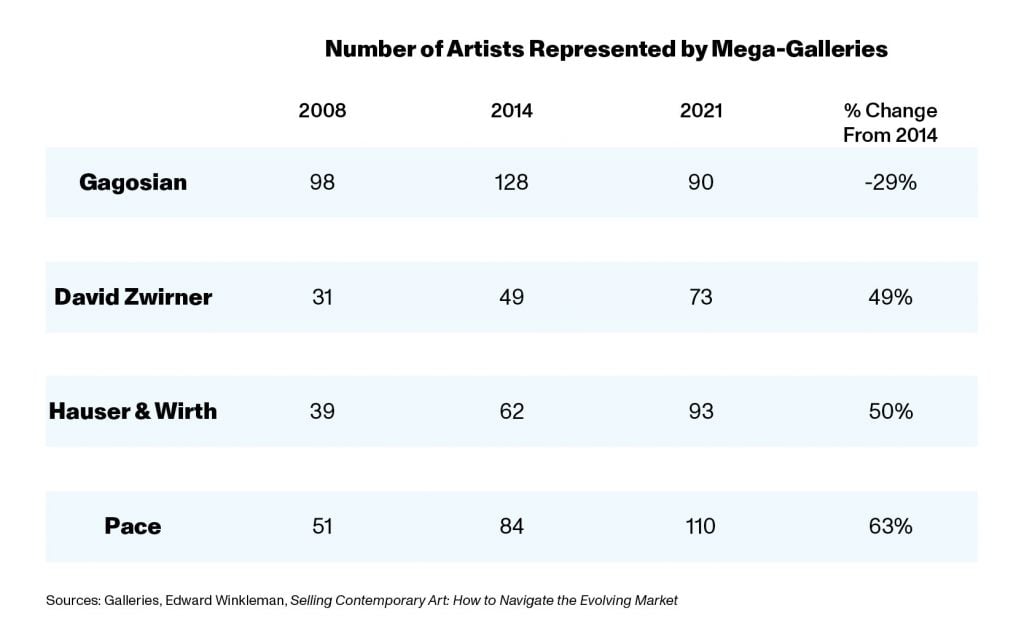

Table by Artnet News.

In 2014, the gap between Gagosian and the rest was vast. The gallery had 15 outposts and represented 128 artists, according to Selling Contemporary Art: How to Navigate the Evolving Market, a book by art dealer Edward Winkleman. Its closest competitor, Pace Gallery, had 8 galleries and 84 artists.

But the gap has been closing. While Gagosian still has the most exhibition space, branches, and staff, its growth has slowed down, and even reversed. The gallery currently lists 90 artists on its website, down 29 percent from seven years ago.

Meanwhile, Gagosian’s three rivals have been in full-on expansion mode, adding artists and opening new galleries. (All four galleries declined to comment on sales and revenues.)

Today, Pace and Hauser & Wirth both represent more artists than Gagosian, a key metric of a gallery’s success and influence. Pace leads the pack with 110 artists and estates. It recently signed Jeff Koons, the world’s most expensive living artist at auction, who had been working with Gagosian and Zwirner.

Those who sought out representation over the past two years and didn’t end up with Gagosian include Barbara Kruger and the estate of Robert Ryman, which went to Zwirner. George Condo and Cindy Sherman chose Hauser & Wirth.

The latter has gobbled up the most artists in the past two years—23, to be precise—including hot young painters like Avery Singer and Christina Quarles. The art world is aflutter with speculation about its heady signing bonuses ($1 million for Singer! $50 million for Condo! $100 million for Sherman!). The gallery didn’t respond to requests for comment.

Table by Artnet News.

To be sure, Gagosian remains a force to be reckoned with. “He’s still probably No. 1 until there’s evidence that he isn’t,” said Don Thompson, an economist and author of two popular books about the art market.

The gallery has taken steps to address succession concerns by naming art dealer Andrew Fabricant as its chief operating officer in 2019, a role that makes him second-in-command at the gallery. But for Thompson, the question still remains: “What happens when [Gagosian] ceases his role?”

***

A similar generational shift was at play in the late 1980s when the influence of Castelli, the top dealer of the previous 25 years, was waning. Many of his artists departed and ascendant galleries such as Pace, Gagosian, and Mary Boone were vying for primacy.

Since opening his gallery in 1957, Castelli focused on discovering and nurturing American artists—Andy Warhol, Roy Lichtenstein, Robert Rauschenberg—and bringing them to an international audience.

“The gallery was there at the specific time when the center of the art scene moved from Paris to New York City,” said Bertozzi Castelli. “And all the artists were shown at Leo’s gallery.”

People often forget that Castelli was an artist-centered, primary market gallery, she noted. The dealer hated resales and was willing to forgo profit while partnering with other galleries to promote his artists. “He used to say that in the secondary market, any type of unethical thing could happen, and he was happy he didn’t need to do it,” Bertozzi Castelli said.

Larry Gagosian in 1988. (Photo by Lynn Goldsmith/Corbis/VCG via Getty Images)

Gagosian, who learned from Castelli, realized that there was another way. His innovation was to open his own galleries around the world and divide his focus between primary and secondary market deals. This way, he didn’t have to share the profit and benefited completely from the upside.

The model took hold in an increasingly globalized art world, but its sustainability has been the subject of fierce debate. As the pandemic struck, even Gagosian started to question the approach. He closed his San Francisco space last year (but also added programming at the former Marciano Foundation in Los Angeles).

“When things go down like this you say, ‘Jesus, Larry, do you really need all these galleries?”’ Gagosian said last year.

***

It remains unclear what the next model will be.

One place to look for answers is the luxury sector, where a handful of companies, including Francois Pinault’s Kering and Bernard Arnault’s LVMH, have outsize influence, power, and brand recognition.

“The top three-four conglomerates take up a larger share of the market every year,” Thompson said. A similar trend is happening in the art world, where the top four galleries (as well as Sotheby’s and Christie’s) are increasing their total sales annually, he added.

Hauser & Wirth presidents Iwan and Manuela Wirth and Marc Payot. Photo courtesy of Hauser & Wirth.

Companies like Prada, Gucci, and Louis Vuitton have transformed from their original niches (in leather goods and luggage) to global brands that are larger than any of the product lines they offer.

“In the art world, there’s recognition that more can be done on the brand building side,” Degen said.

***

Indeed, each gallery seems to be working to carve out its own brand identity to attract new audiences and expand the global collector base. Gagosian—who, it has been said, was the first to perfect the art of selling art to billionaires—established itself as elite, maximalist, and unabashedly luxe. For the latest installment of its livestreamed “Premieres” series, it got Patti Smith to perform in front of Gerhard Richter’s paintings.

“People know Gagosian like they know Art Basel,” Degen said. “They may not have been to the gallery, but they know the brand.”

President Bill Clinton, Ben Stiller and David Zwirner attend the Artists for Haiti dinner. (Photo by Andrew H. Walker/Getty Images)

Zwirner, which has poured abundant resources into its publishing arm and robust online infrastructure, distinguished itself as perhaps the most high-minded of the bunch, while Hauser & Wirth has deep pockets, no single aesthetic, and a European sensibility. With destination locations like its art-filled hotel, The Fife Arms, in Scotland (technically operated by a separate company) and its forthcoming Mallorca art center, it is the closest the gallery scene has to a lifestyle brand. Finally, the populist-leaning Pace is the most open to experimentation, having been early to court the tech community and invest in crowd-pleasing immersive art projects.

The stakes are higher for these dealers than for predecessors like Castelli because the business is global and the internet has expanded the audience for art dramatically. Exhibitions by teamLab draw millions of visitors, while artists like KAWS and Jean-Michel Basquiat are global brands themselves, more recognized than the galleries who represent them.

teamLab’s Infinite Crystal Universe, 2015-2018. Image courtesy of Pace Gallery.

“That’s going to be the next big question in terms of the next model,” Degen said. “How do you monetize the growing interest among the wider public? And who will be the one to figure out how to do that in a way that doesn’t degrade the brand or alienate artists?”