Every Monday morning, artnet News brings you The Gray Market. The column decodes important stories from the previous week—and offers unparalleled insight into the inner workings of the art industry in the process.

This week, debating just how much we lose if the world’s oldest auction house indeed leaves the public arena…

DO YOU SEE WHAT I SEE?

In case you’ve been living inside of a bottle for the past week, on Monday, Franco-Israeli telecom billionaire Patrick Drahi agreed to terms on a deal to acquire Sotheby’s and take the 275-year-old auction house private. Pending final shareholder approval, the transaction’s price tag would reach $3.7 billion through a combination of cash, financing, and assumption of Sotheby’s existing debt. Investors would be bought out at $57 per share, a roughly 61 percent premium over the house’s trading price the preceding Friday and only a few pennies south of its all-time high.

Drahi’s bid shocked the art industry, in no small part because he himself seems to be a largely unknown quantity in this realm. (My colleague Eileen Kinsella and I compiled a dossier on what we know about the man so far.) With relatively little to go on regarding his plans for Sotheby’s, a considerable amount of analysis has focused on what the house’s move to private ownership would mean for auction-market transparency.

Broadly speaking, two opposing schools of thought exist. The more popular one holds that this development blinds our view of telling details about one of the market’s biggest players. Since Sotheby’s will no longer need to regularly compile and release an armada of SEC filings, we will no longer be able to learn unquestionable information about the house’s profits and losses, art-financing ledgers, executive compensation, and other hard data not provided by privately held nemesis Christie’s (which releases only highly selective sales info subject to far less official oversight). The end result is a crippling blow to transparency in the art market.

A view outside Sotheby’s in New York City. (Photo by Noam Galai/Getty Images)

The opposing camp, however, argues that Sotheby’s public filings provide far less clarity about either the company itself or the market overall than it might seem. For instance, in-house financial guarantees, one of the most controversial and consequential aspects of the auction market today, are not itemized in any of the house’s publicly available documents, and neither are winning bidders or the payment status of their acquisitions. Besides, even if the public had access to comprehensive information about Sotheby’s business, it would still leave both the rest of the auction market and the entire gallery sector as a giant mass of dark matter.

I think each side has a point. It’s certainly true that Sotheby’s SEC filings provide less information than keen market observers would like, but I think it’s also impossible to contend in good faith that these losses of visibility, however incremental, are a good thing for a market trying to shake a well-earned reputation for concealment. If you’ll allow me an analogy, my quality of life wouldn’t be that much worse if I no longer had eyebrows, but it doesn’t mean I should be happy if some maniac dragged me into an alley and shaved them off.

One loss of transparency that hasn’t received much attention, however, is the one that extends beyond art and collectibles sales. If the house does indeed exit the New York Stock Exchange (where it has traded for the past 31 years), it won’t just black out a peephole into the auction market. It will black out what has long been a peephole into the financial markets as a whole, as well as the moment-to-moment psychology of the world’s wealthiest class.

Sotheby’s at the New York Stock Exchange. Photo courtesy of Sotheby’s.

SIGNS AND SYMBOLS

Shortly after news broke about Sotheby’s proposed sale to Drahi last Monday, financial analyst Michael Santoli tweeted about how the house’s price on the NYSE has been “one of the better market ‘tells’ of recent decades,” by virtue of its tendency to climb and dive based on the discretionary purchases of the major-investor class.

Here’s how I explained the concept in a piece analyzing Sotheby’s CEO Tad Smith’s first-year compensation package back in 2016:

Sotheby’s performance historically just piggybacks the wealth effect. When the world economy booms and portfolio values rise, elites tend to spend more, especially on luxury goods—and a high-end public auction house like [Sotheby’s] becomes a king-slayer. When the world economy sputters and portfolio values decline, elites tend to spend less—and [Sotheby’s] starts losing limbs like an untreated leper.

Later, Santoli elaborated on the “tell” concept on CNBC’s Closing Bell, telestrating a chart (below) that pitted Sotheby’s share price against the performance of the S&P 500, Standard & Poor’s index of the 500 largest companies weighted by their market capitalization (meaning, the quantity of shares outstanding multiplied by their current trading price).

Sotheby’s trading price versus the S&P 500 index, from the late 1980s to 2019. Courtesy of Michael Santoli.

Santoli noted that Sotheby’s price (in blue) peaked either almost exactly in sync with the S&P (in yellow) or within a few months at the following critical points in market history:

- October 1989, before the start of the 1990 recession

- Late April 1999, before the dot-com bubble burst

- October 2007, before the start of the Great Recession, and…

- Late March 2011, before a dip caused by the Eurozone debt crisis

However, Santoli also raised a point I hadn’t heard previously. Starting in 2013 (marked by the third circle from the right on his chart), Sotheby’s suddenly crapped out as an indicator of the broader public asset markets.

That year, the S&P broke out above the resistance it kept meeting during the roughly 13-year period beginning with the pre-dot-com peak. Sotheby’s price since 2013, by contrast, has taken harder dives than the S&P but failed to meaningfully rise above its previous highs during upswings.

All of which begs a question that mirrored the one I asked myself when Drahi’s deal for the house suddenly emerged: What the hell happened?

THE BIG BREAKOUT

Admittedly, this question deserves in-depth treatment from someone smarter than a guy who once accidentally flipped a whole freshly baked pizza face-down onto the back of a hot oven door. But I’m going to take a shot at it anyway.

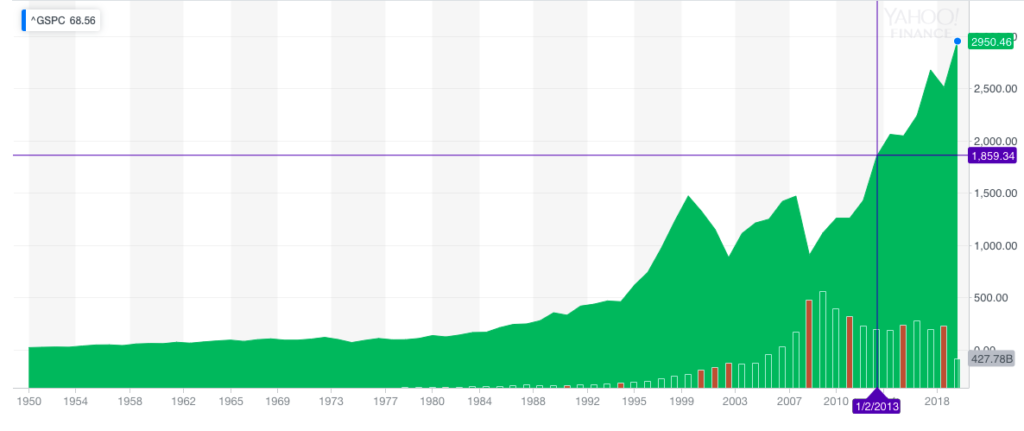

If Sotheby’s stopped tracking with the S&P in 2013, the obvious first question to ask is whether something extraordinary started happening with either Sotheby’s or the S&P around that time. Chart the S&P alone since 1950, and what you see is this….

The S&P 500 index, from 1950 to 2019. Courtesy of Yahoo Finance.

By the middle of 2012, the index edged above its previous all-time high of 1,469.25 back in 1999. By January 2013 (the crossed purple lines above), that previous all-time high started to look quaint. And by January 2019, the S&P 500 had more than doubled its 1999 peak, closing at 2,950.46.

Now, I’m not a macroeconomist. But one important contributing factor in this development is the explosive growth of the so-called FAANG stocks—Facebook, Amazon, Apple, Netflix, and the artist formerly known as Google. (Technically, what trades now is Google’s parent company, Alphabet.) Between 2013 and 2018, the FAANGs reached titanic individual valuations, with Apple and Amazon becoming the first two trillion-dollar companies last year. Together, the quintet managed to double its influence on the S&P in those five years, collectively comprising over 11 percent of the index’s total value by March 2018.

A smart investor and collector suggested to me on Friday that it would be very interesting to compare Sotheby’s post-2013 price against the S&P minus the FAANGs. That analysis demanded more quant skills and time than I had for this column this week, but I suspect the house’s share price would track much better with the de-FAANGed S&P 500 than the complete one, which has now basically been mainlining Human Growth Hormone from Silicon Valley for about seven years.

I’m going to go further, though. Data doesn’t just show that Sotheby’s share price has been unable to grow in tune with the broader financial markets. I think it shows that the auction market as a whole has been unable to grow in tune with the wealth of the investing class.

John Baldessari, Money (with Space Between), (1991) courtesy Gemini G.E.L.© John Baldessari.

GROWING PAINS

Back in 2009, the National Bureau of Economic Research published a working paper suggesting that art prices increase as income inequality worsens. It’s also widely accepted by now that income and wealth inequality have been getting substantially more severe for about 40 years. For example, the World Inequality Lab found that, between 1980–2017, the share of wealth controlled by the richest one percent in the US, China, and Europe increased from 28 percent to 33 percent, while the share of wealth controlled by the poorest 75 percent went unchanged.

So what has happened to artwork prices since 2013, the year that the S&P 500 first started going benevolently berserk?

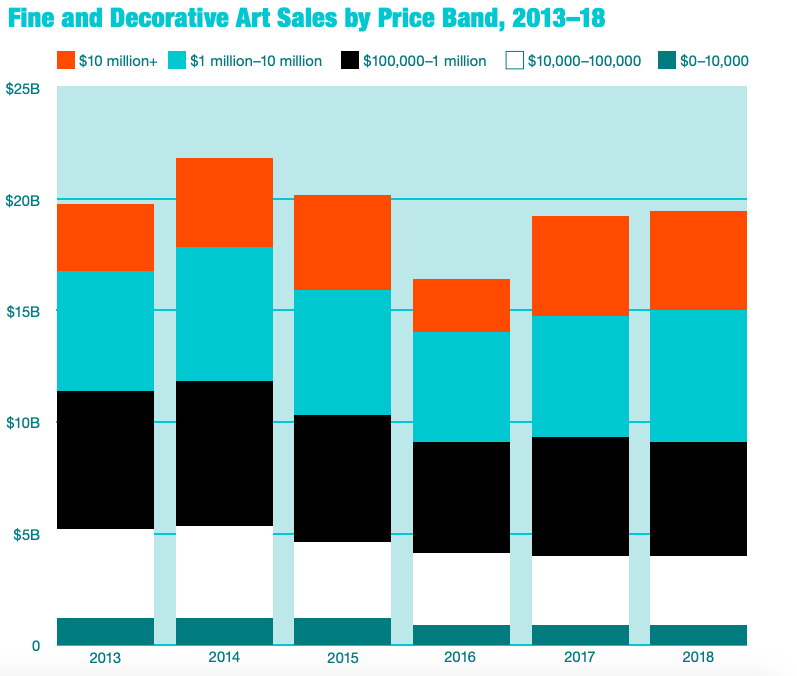

In the latest artnet Intelligence Report, we found that the two highest-priced tiers of fine art and decorative art at auction were the only two whose share of total sales grew from 2013 through 2018. The proportion of works priced from $1 million to $10 million increased by about 9 percent during that period, and the proportion of works priced above $10 million increased by about 32 percent.

As for the price tiers below those two, each one decreased over the same span… by between roughly 24 percent and 30 percent.

Fine Art and Decorative Art Sales by Price Band, 2013–2018. © 2019 artnet Intelligence Report.

Those aren’t the only downturns in the auction market, though. The total number of fine and decorative artworks sold annually dropped from about 620,000 in 2014 to about 456,000 in 2018. And the total value of those sales plunged from about $21.8 billion in 2014 to about $19.3 billion in 2018. (As Felix Salmon noted on Sunday night, the all-time highs for annual sales value and lots sold came in 2011, so these figures have actually been in in decline for a bit longer than the chart above shows. But back then, Sotheby’s share price was still outperforming the S&P.)

How has Sotheby’s itself performed since 2013? Based on its annual reports, the house’s consolidated sales—a blend of aggregate auction sales, private sales, and sales from inventory—peaked in 2014 at just below $6.8 billion. Sotheby’s hasn’t gotten close to that figure since. Last year, its best in the range, the house still came up about $420 million short.

So what do we make of all this?

TELL ME A STORY

Here’s a narrative that makes sense to me based on the data points above, and that also gels with my anecdotal experience in the art world: On average, prices for individual artworks have continued to grow in tune with wealth concentration since 2013, but the auction market as a whole has not figured out how to grow with them. And Sotheby’s share price has stalled out as a result.

Let’s tease that out a little more, shall we?

Boosted in part by absurdly muscular results from the FAANGs, the S&P has powered up to new heights, which signaled (and to some extent, helped create) a new level of wealth for global elites. This new level of wealth and its increasing consolidation have indeed contributed to fatter prices for individual artworks, at least at the top of the market. But the supply of high-priced artworks and the number of auctions per year are finite, which means that only a limited number of those high-priced artworks can make it to the auction block every year.

In tandem, the rising wealth concentration over this period reduced the number of middle-class and upper-middle-class buyers, while the rising artwork prices left fewer works in the price range of those who remained. And on top of that, the auction houses have been collectively unable to divine substantial new revenue streams to replace the income they’ve lost due to this hollowing out of the buyer base.

As a result, the auction market has shrunk in terms of overall value and number of clients. And why would investors want to pump money into a publicly traded auction house whose headline figures, as a consequence of all of the above, continue to sputter relative to the jet propulsion of its core constituency’s fortunes?

An expert pouring over the Voynich Manuscript in 2016. Photo by Cesar Manso/AFP/Getty Images.

If this story isn’t just a story, then it’s all the more reason that Sotheby’s should concentrate on expanding its buyer base and diversifying its revenue streams. It’s the only way to significantly push sales through the coffin lid they’ve been flailing against for the past five years.

Maybe Patrick Drahi thinks he and Sotheby’s current leadership can do those things. If so, it would provide a plausible business motivation (beyond just flexing) for trying to buy the company at all, let alone at such a high premium.

But even if he’s right, the rest of us won’t be able to see it—at least, unless the growth eventually becomes so rampant that Drahi can cash out for a big gain by taking the house public again. And at that point, maybe Sotheby’s stock will once again tell us something useful about the confidence levels of the wealthy and the fate of the public asset markets overall.

[artnet News]

That’s all for this week. ‘Til next time, remember: In the land of the blind, the one-eyed man is grossly outnumbered.

")