How does a museum end up deciding to sell off substantially all of its most valuable artworks? That’s a question rarely answered. Now, however, thanks to a lawsuit from the indefatigable Berkshire Eagle, the Berkshire Museum has been forced to reveal just that. The results—in the form of some 60 pages of formerly sealed internal documents—are eye-opening.

The story told by the newly released papers, which were made public on Monday, starts in April 2016. That’s when the board of the Berkshire Museum was presented with a detailed report from TDC, a group of museum consultants in Boston. In their “summary of capitalization needs,” TDC concluded that the museum needed about $2 million to pay down debt and about $6 million to improve the facilities. They also penciled in about $23 million in permanent endowments, a sum much greater than the museum’s existing $7.3 million endowment. Altogether, they concluded, the museum needed “an additional $25.61 million in new funds” to “stabilize its operations on multiple dimensions.”

At roughly the same time, the museum board invited both Sotheby’s and Christie’s to value its collection of some 35,000 objects, most of which have essentially zero interest to auction houses. Sotheby’s, which ended up getting the final mandate, only even looked at 207 artworks, and concluded that the 40 most valuable pieces were worth somewhere between $47 million and $85 million, accounting for about 90 percent of the total value of the collection.

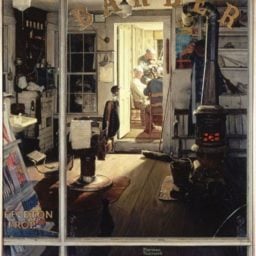

Norman Rockwell, Shuffleton’s Barbershop (1950). Courtesy of the Berkshire Museum.

Most prominently, said Sotheby’s, the museum’s Norman Rockwell masterpiece, Shuffleton’s Barbershop (1950), was worth between $20 million and $30 million on its own, or about 35 percent of the value of the entire collection. The other Rockwell, Shaftsbury Blacksmith Shop (1966), was worth between $7 million and $10 million.

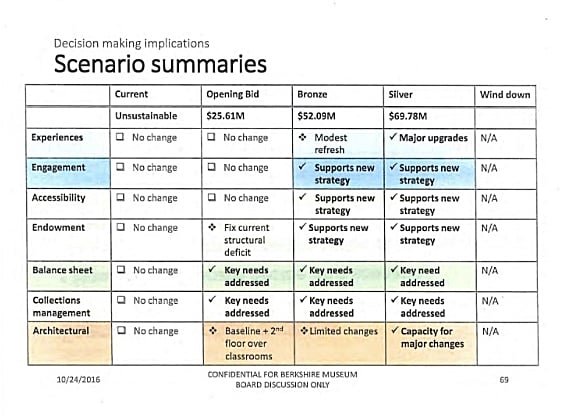

After receiving all this information, the board discussed five different scenarios at a meeting in October 2016. To look at the handout distributed to board members during this meeting is to watch management making it very clear which direction it wanted to go in; it’s clear why the museum wanted to keep it secret.

A chart distributed to the Berkshire Museum’s board last year. The document was made public by the museum in response to a lawsuit brought by the Berkshire Eagle.

Each scenario has a price tag attached, and each price tag corresponds, conveniently enough, to a different degree of deaccessioning. The “Current” scenario, corresponding to no deaccessioning at all, is dismissed outright as being “unsustainable.” That messaging forces the board to choose one of the other four scenarios; all of them involve either selling off art or else closing the museum entirely.

Since no board wants to opt for a “wind down” strategy, the handout essentially forces the board to deaccession artworks. The question is no longer whether to deaccession; just how much deaccessioning to do.

The Berkshire Museum, when it released these records, went to great pains to point out that these are historical documents, and date from a time “now more than 18-months out of date when the planning process was not even halfway through.” But it’s pretty clear that as of October 2016, the decision to deaccession had already been made. (Realistically, of course, there was no point in even asking TDC for an expensive enumeration of “capitalization needs” in the first place, unless management had already decided that the art was going to get sold.)

The three deaccessioning scenarios are given names. One is “Bronze,” one is “Silver,” and therefore you’d expect the third to be “Gold.” But in fact the cheapest scenario—the one which could be funded by selling just a single Rockwell—is referred to only as “Opening Bid.” That column consists mostly of plain Roman type saying that the modest amount of money would generate “no change.”

Once you start getting into the “Bronze” and “Silver” scenarios, on the other hand, things get more exciting: the type turns bold, there are lots more tick marks, and you get positives like “supports new strategy” and “major upgrades.” The more you spend, the more upbeat you can be in announcing your New Vision, and the more you can kid yourself that, far from decimating the Berkshires’ cultural patrimony, you’re instead creating something amazing for the next generation.

Meanwhile, astonishingly, there is nothing on this sheet about deaccessioning, or the costs associated with each of the plans. The museum’s director, working in concert with Sotheby’s, has found a magical money tree, and the only question facing the board is the degree to which they want to shake it.

The board’s choices are clear: do you want more and better, or do you want less and worse? It’s hardly surprising that they chose to auction off as many works as they could—even unto a pair of Calder sculptures which are utterly central to the history and mission of the museum. It comes as no surprise, then, that the board ended up opting for the Silver plan, the most expensive one, without bothering themselves much with the inevitable consequences in terms of the fate of the museum’s collection.

It’s easy to imagine a much more honest version of this sheet. The costs of deaccessioning would be made clear, including certain opprobrium from museum professionals nationwide; a massive PR disaster; withdrawal from a coveted partnership with the Smithsonian; an inability ever to borrow works for exhibitions from any other accredited museum; and, quite possibly, a lawsuit from the state attorney general.

In this alternative universe, once the board decided to get a real grip on its finances, it could start quietly talking to the Norman Rockwell Museum, down the road. Some kind of deal could surely be done whereby a donor would effectively fund the move of two great Rockwell paintings into the place where his legacy is most studied and celebrated. Technically, that would still have meant the deaccession of one or two Rockwells, but in practice no one would have minded very much, because the paintings would have stayed in a Berkshires museum.

As ever, how you ask any given question largely determines the answer you’re going to get. The tragedy of the Berkshire Museum is that its board hired a director who was very good at asking exactly the wrong questions, in exactly the wrong manner. And now, mired in lawsuits, they’re facing the consequences.