Analysis

Sure, NFT Sales Are Slipping—But a Closer Look at the Data Shows the Market Hasn’t Imploded (Yet)

A recent report only tells half the story of what's going on.

on June 1, 2021.")

A recent report only tells half the story of what's going on.

Amy Castor

ShareShare This Article

ShareShare This Article

A report in crypto news site Protos got a lot of traction last week after claiming that the NFT market “imploded” in May. Is it true? Are NFTs a thing of the past?

No. The fact is, NFT sales may be slipping, but the market hasn’t imploded—at least not yet—despite what the media is reporting.

Most of the data gleaned for the Protos report comes from Nonfungible.com, a website that tracks NFT-related transactions on the Ethereum blockchain. But when I reached out for comment, Nonfungible.com itself called the Protos piece “completely misleading,” and pointed to a lengthy blog post the company had written in retort. (In an email, they said that they had only learned of the report through my own tweet of the article, a tweet, which, for some bizarre reason, went viral.)

“This article definitely tried to take down the NFT space, through the revelation of a hypothetical bubble burst,” Gauthier Zuppinger, the cofounder of Nonfungible.com, wrote to me. “This is precisely the reason why we take our role as data providers and market analysts extremely seriously.”

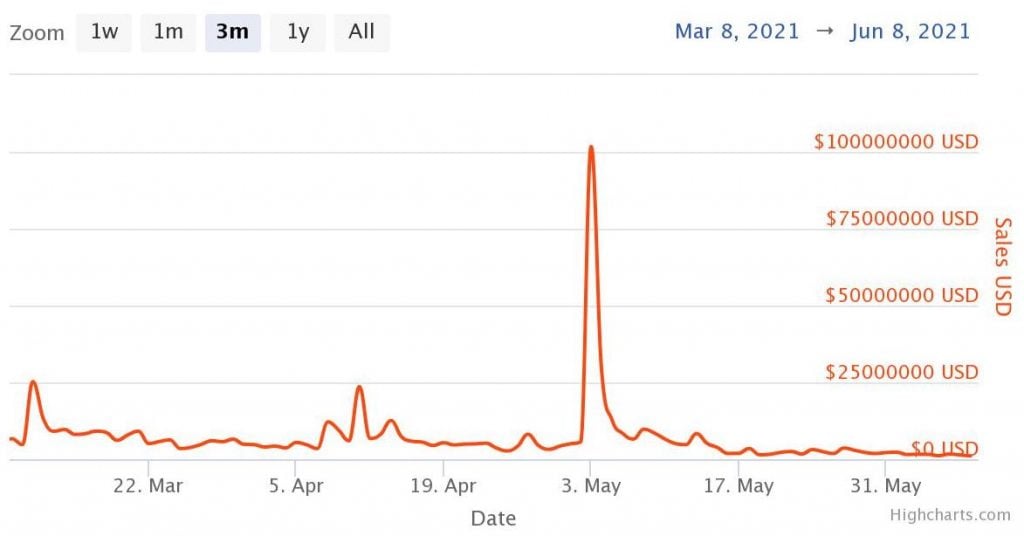

According to Nonfungible.com’s data, NFT sales peaked on May 3 when $102 million worth of NFTs changed hands in a single day. Nearly all of that is attributable to crypto collectibles (collections of digital images with a common theme that are swapped online like trading cards), which made up fully $100 million of those sales, according to the study.

The seven-day period surrounding the peak brought $170 million in transactions, the analysis stated. By the final week of May, sales collapsed to around $19.4 million, representing a 90 percent drop from the record high, Protos pointed out in its withering conclusion.

Before thinking of this as a bubble bursting, though, consider that May 3 was not just any day. It was the day that an NFT project called Meebits launched—and 9,000 hotly anticipated crypto collectibles went up for public sale.

Graph from Nonfungible.com showing sales of NFTs over the last three months as of June 8, 2021.

All of the 3D voxel-based avatars sold out in a matter of hours, netting Larva Labs $80 million worth of ether, the native cryptocurrency of Ethereum. Larva Labs is the same company behind the pixelated avatars known as CryptoPunks, one of the the most well known and closely followed crypto collectibles.

Since Nonfungible.com started tracking NFT sales back in mid-2017, May 3 saw the highest daily sales ever. To give you a sense of what an outlier this was, the second highest sales day was March 11 ($26 million), followed by April 11 ($24 million).

Of the seven markets tracked by Nonfungible.com, “collectibles” took the lead by a wide margin. In recent days, both CrypoPunks and Meebits have continued to be top sellers—one Meebit sold for $154,000 worth of ether, while another sold for $142,000 and two CryptoPunks sold for around $100,000.

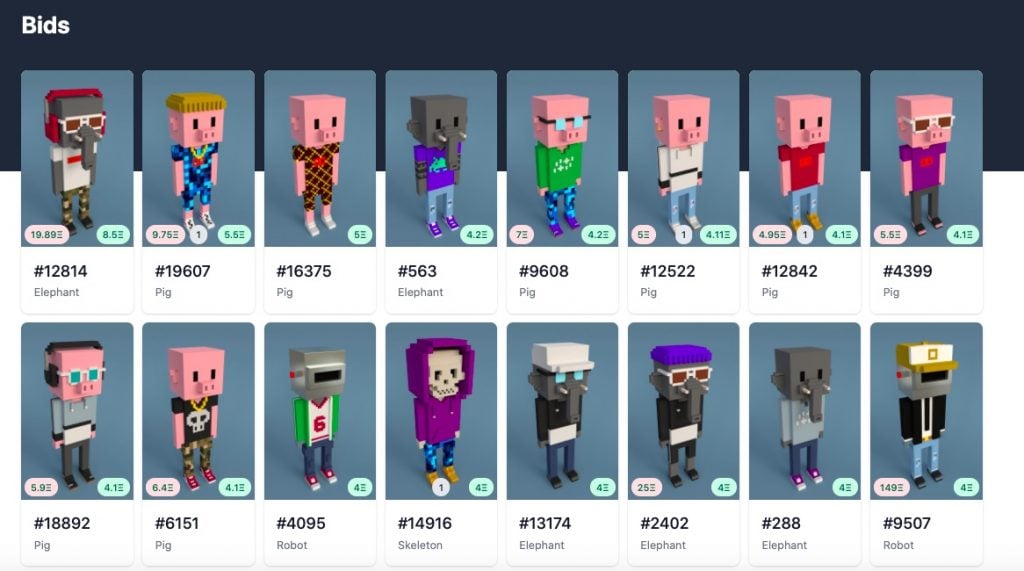

Screenshot of the “Bids” section of LarvaLabs’s Meebits site.

By dollar values alone, collectibles brought in the most sales so far this year ($565 million), followed by art ($226 million), and sports ($74 million), the Protos report said.

Some might find this “sports” total surprisingly low, given that many headlines have been written about NBA successfully turning sports highlights into NFTs via NBA Top Shot. But Nonfungible.com excludes some of the most popular NFT sales, including Top Shot, which runs on Dapper Lab’s Flow blockchain, not Ethereum. (Nonfungible.com says it plans to add Flow data in the near future.)

Pak’s The Switch (2021) sold for $1.4 million with 10 bidders chasing. Courtesy of Sotheby’s and Pak.

Similarly, if the numbers for the crypto-art category appear startlingly low, that is because Nonfungible.com only tracks on-chain transactions. Some of the biggest sales of crypto art—like the Beeple digital collage that sold at Christie’s for $69.3 million worth of ether, Sotheby’s sale of Pak for $17 million, and so on, generally happen off-chain, meaning they are not recorded on the public blockchain. (This has, in turn, led some in the digital art community to question whether these are “real” NFTs.)

And that includes big NFT art sales in May, such the $17 million sale of nine CryptoPunk NFTs at Christie’s.

Images of CryptoPunks displayed on a digital billboard in Times Square on May 12, 2021 in New York City. (Photo by Alexi Rosenfeld/Getty Images)

Basically, the Nonfungible.com data excludes most of the recent surge of interest in NFTs from the fine art world.

It’s also worth noting that Nonfungible.com does not track sales data on Nifty Gateway—a popular NFT marketplace owned by Gemini. Unlike most NFT marketplaces, Nifty Gateway functions more like an exchange. It’s custodial in that they hold all your keys by default, until you move your tokens off the platform.

“Nifty Gateway is a centralized marketplace—both primary and secondary market sales are not recorded on-chain,” a Nifty Gateway representative explained in an email. “The initial minting of the tokens happens on-chain and if a user withdraws them off the platform, this is recorded on-chain. We create and store all of our NFTs on the Ethereum blockchain. But the sales happen off-chain, on our website. Off-chain sales are faster, easier to use, and have much lower fees.”

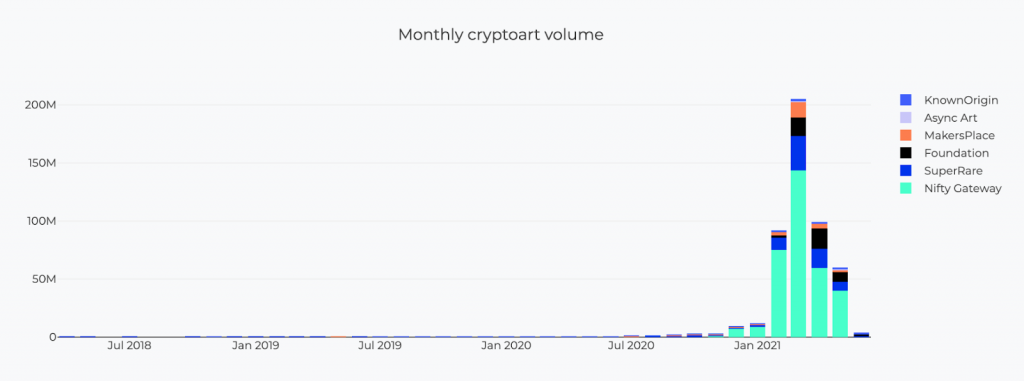

Graph of volume of sales on major NFT platforms, from Cryptoart.io.

Still, monthly sales on Nifty Gateway of $40 million in May were down from $60 million in April, and had fallen significantly from March when they totaled $144 million, according to data from Cryptoart.io, another data site.

So sales are slumping, though they haven’t become a dried up riverbed of the damned either.

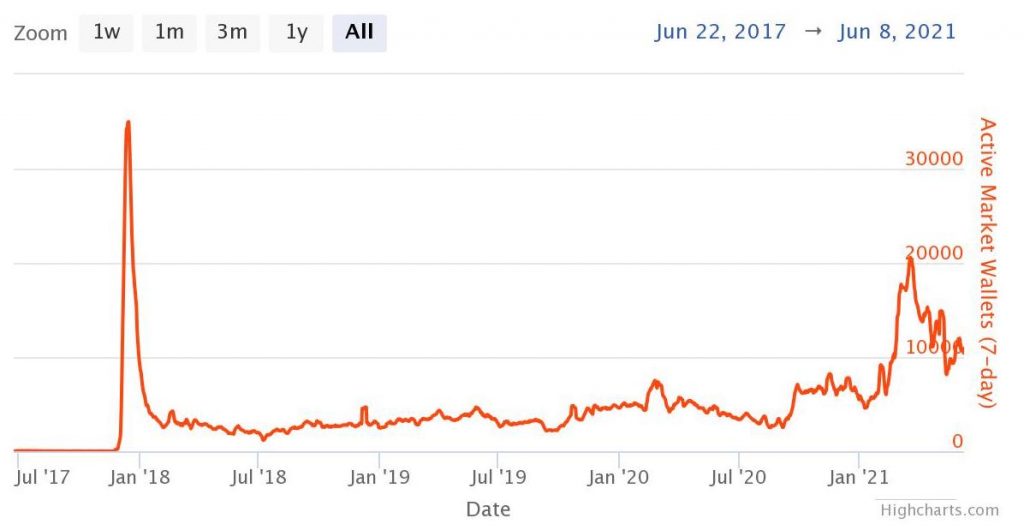

Another worrying sign for the NFT market, according to the Protos analysis, is that the number of active NFT wallets (that is, wallets that register a purchase or sale on a particular day) dropped 70 percent from 12,000 at its daily peak to 3,900 last week. However, again, that is not a fair reflection of the current market.

That daily peak comes from way back in December 2017 when CryptoKitties, the project that was briefly so popular that it clogged the Ethereum blockchain, were all the rage—before falling quickly out of the headlines for literally years.

Graph from Nonfungible.com showing active wallets since 2017.

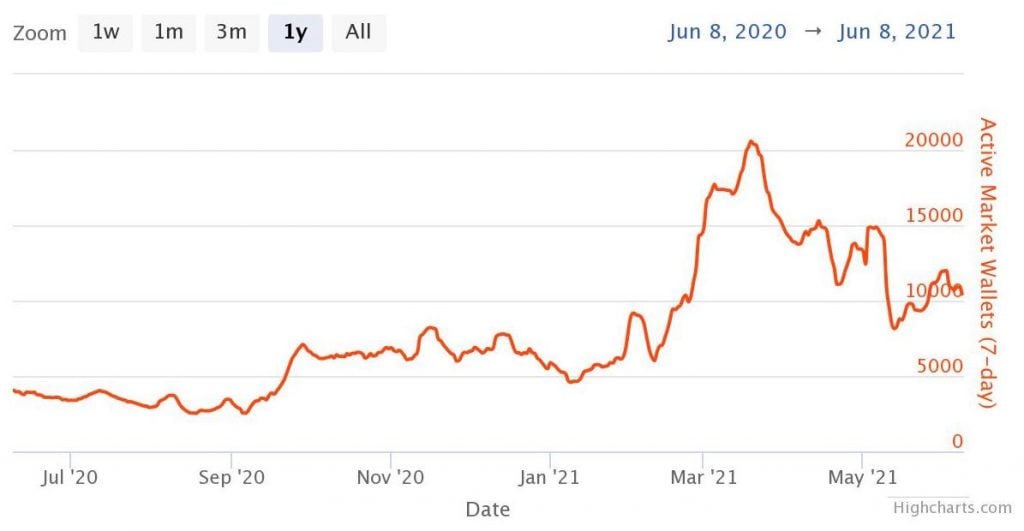

If we consider only the recent NFT bubble, which started building in October 2020, the daily peak in active wallets was 5,700 on March 17, 2021. Compared to that more recent (and relevant) benchmark, the current total represents a 39 percent decrease instead of the much more alarming 70 percent.

Graph from Nonfungible.com showing active wallets over the last year as of June 8, 2021.

All this is to say, the NFT market definitely appears to be cooling off, just not to the dramatic extent that Protos reports.

[UPDATE 6/16/21: In an email, Protos editor David Canellis said that the peak number of “active wallets” did not refer to the 2017 peak associated with CryptoKitties. Instead he says that the “over 12,000” number was generated by adding together the peak number of wallets active in each category of NFTs listed on NonFungible.com, even though these peaks occurred on different days: “This is to be kind to each category as they trend differently,” he wrote. The various peaks are “Collectible,” which reached 4,589 on May 3, 2021: “Game,” which reached 1,036 on May 14, 2021; “DeFi,” which reached 89 on January 22, 2021; “Art,” which reached 2,215 on March 17, 2021: “Utility,” which reached 678 on April 25, 2021; “Metaverse,” which reached 940 on November 12, 2020; and “Sports,” which reached 2,761 on February 7, 2021.]

But why is it cooling at all? A quick look at the broader crypto markets gives a possible answer.

Graph of the price of Ether, year to date, as of June 8, 2021, from Coinbase.com.

Ether reached an all-time-high of $4,300 on May 12. This run up left many ETH whales with spare change to pour into NFTs. The world’s second most popular cryptocurrency went on to lose over half its value before recovering to $2,600 at the end of the month. Similarly, bitcoin surged an all-time-high of $64,000 on April 14. By the end of May, it had crashed to $35,000.

Less valuable cryptocurrencies mean less money overall to throw around at NFTs.

“If you look at the big picture, everything keeps growing, despite the crypto-currency decrease and the over-hype in the past few weeks,” Zuppinger wrote, adding that Nonfungible.com plans to publish its own quarterly report in a few weeks.

I’m not sure this sanguine assessment is an accurate description of the market either. The hype has been so thick—and there is so much actual grift in the space—that there are plenty of people hungry for a story about a fall. But we can’t let that get in the way of looking at the data clearly.