Analysis

The Gray Market: Why You Can’t Trade Art Like Stocks (and Other Insights)

This week, our columnist examines three stories that raise hard questions about what the art market is—and what it isn't.

This week, our columnist examines three stories that raise hard questions about what the art market is—and what it isn't.

Tim Schneider

ShareShare This Article

ShareShare This Article

Every Monday morning, artnet News brings you The Gray Market. The column decodes important stories from the previous week—and offers unparalleled insight into the inner workings of the art industry in the process.

This week, we’re examining three stories that raise hard questions about what the art market is and isn’t…

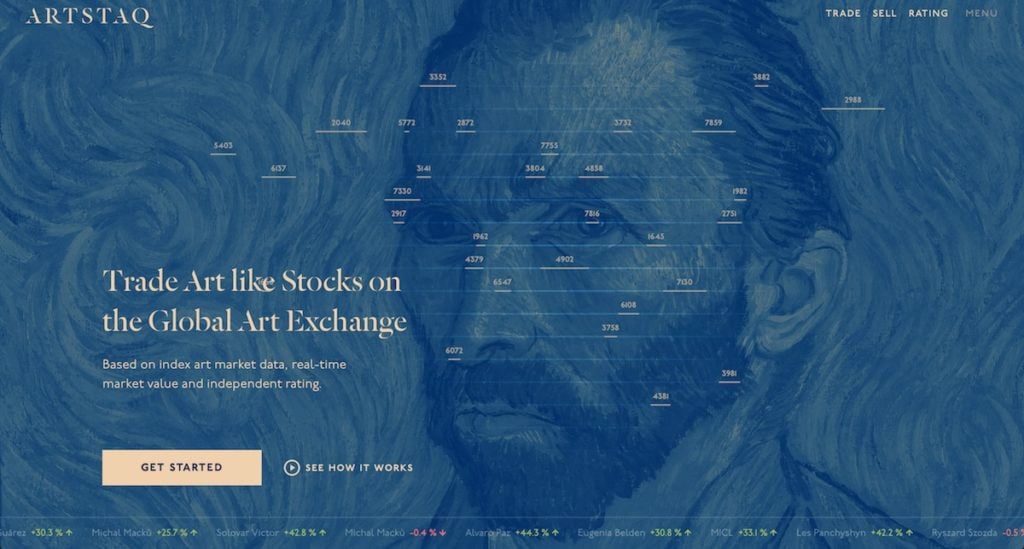

STAQ ATTACK: On Friday, Robin Scher interviewed Petr Václavek, head of communications for London/Prague-based startup ARTSTAQ. The firm seeks to alchemize the work of emerging artists into—here we go again—pure investments. How?

By combining an algorithm-generated rating with opinions from a team of human experts, all in an effort to establish a transparent exchange where participants can “buy paintings from the site, leave them in deposits, and then sell them again like stocks.”

Based on the interview, their press materials, and their website, the only tiny flaw in ARTSTAQ’s model is that no one involved seems to have any idea what they’re talking about. And this becomes readily apparent if we tick through three key statements made by Václavek and the platform’s own online copy.

ARTSTAQ. Image courtesy of ARTSTAQ.

1. “The art market [is] totally unregulated.”

This cliché drives me so insane that at any moment a pair of orderlies are liable to burst into my apartment, ram a bite-guard into my mouth, and muscle me onto an electroshock table. Yes, the art market isn’t regulated to the degree that the financial markets are (or purport to be, anyway—shout out to the unblemished integrity of the rating agencies). There’s no officially sanctioned art-industry watchdog in the vein of the SEC, or even a universally accepted set of best practices for sellers and representatives to abide by.

Yet all of the normal laws of commercial transactions still apply. If they didn’t, we in the art media wouldn’t perpetually have the option to keep the content flowing by tapping at least three major lawsuits and/or investigations like frat-house kegs. As evidence, just consider the current rotation of Dmitry Rybolovlev vs. Yves Bouvier, Alec Baldwin vs. Mary Boone, and the Old Masters forgery debacle seeming to tighten around collector Giuliano Ruffini.

So while there’s plenty of room for improvement in the art industry’s operation and oversight, show me someone willing to imply that you face no penalties if you, say, brazenly traffic fakes or hold up a rival dealer like some brigand in an episode of Deadwood, and I’ll show you someone painting the market with too broad a brush.

2. “All the current art market models and start-ups deal with existing big data information, which only takes into consideration auction results.”

This is blatantly false. ArtRank has been synthesizing data science with on-the-ground intel from an expert network since at least 2014, as founder Carlos Rivera clarified in this interview two years ago. Artsy‘s new analytics initiative under Hugo Liu sounds like it will do something similar. True, neither of those platforms is currently trying to run an art stock market.

But the bombast of Václavek’s statement nevertheless suggests either that ARTSTAQ’s principals aren’t particularly aware of prominent competitors in their chosen field, or that they’re willing to pretend that said competitors don’t exist. I don’t know which is worse, but neither one makes me want to link up my checking account and start funneling cash into the platform.

Still, in terms of pure audacity and baselessness, even these previous claims pale in comparison to the following bombshells, which I found on ARTSTAQ’s website…

3. “Art is one of the safest investments in time of global financial crisis” and is “resilient to fluctuations in the financial markets.”

My reaction to these twin proclamations was the same as my reaction to hearing that GOP Congressman Paul Labrador had declared in a recent town hall meeting that “nobody dies because they don’t have access to health care.” For those of you who are NSFW friendly, I’ll turn the floor over to Billy Bob Thornton. The rest of you, I’m sure, can use your imaginations.

Any art-market professional who’s lived through a financial downturn or two will tell you with confidence that, broadly speaking, the value of art rises and falls in tune with the larger economy—for better and worse. But the most volatile segment of all is the emerging artists that ARTSTAQ exclusively deals in right now.

Almost every longtime collector’s storage contains a mistake room brimming with once-buzzy talents whose identities are now buried deeper in anonymity than high-value FBI informants. In fact, we just emerged from another episode of this mass folly in late 2015, after the heat that had been building on many so-called Zombie Formalists since 2011 finally flamed out (and took a hefty chunk of the market’s alleged “asset value” with it).

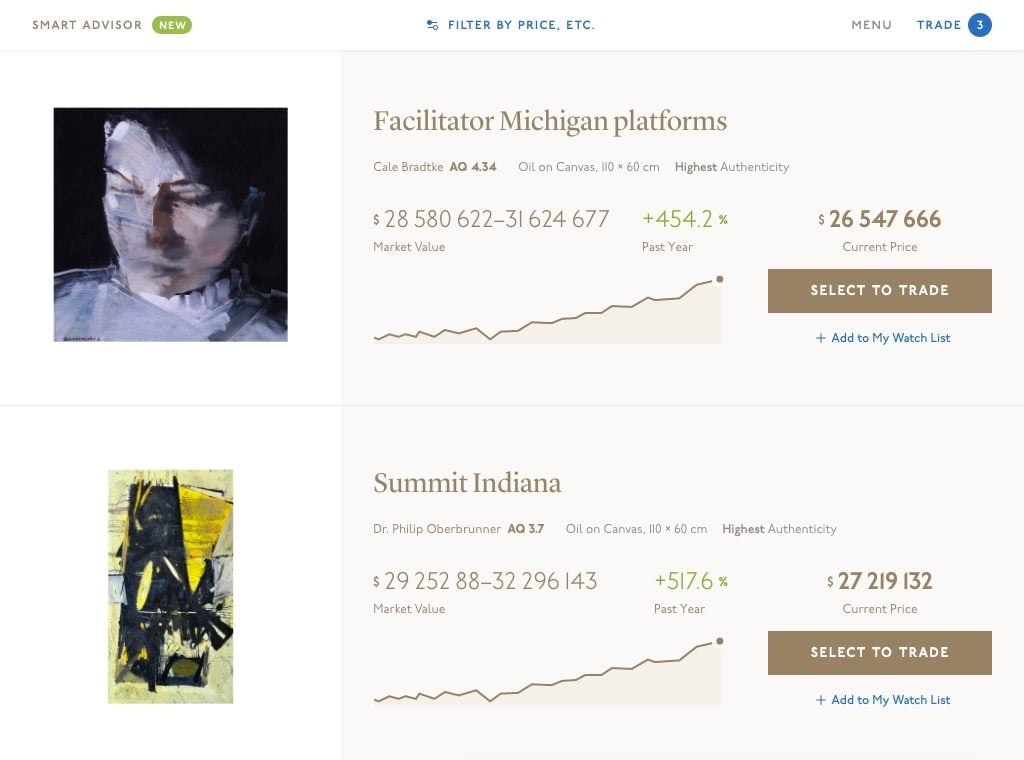

ARTSTAQ’s interface. Image courtesy of ARTSTAQ.

Don’t get me wrong: A Gerhard Richter or a Christopher Wool will still return more money in an economic crash than the work of a recent MFA grad. But if you believe that any of these items qualify as some of the “safest investments” available, have fun trying to, at best, find a ready buyer for an illiquid good in the downswing of a subjective market—and at the apocalyptic worst, navigate a future wasteland ruled by roving bands of headhunters while trying to barter painted canvas for lantern oil.

Until then, I’ll continue to apply financial advisor and Wall Street analyst Josh Brown (a.k.a. The Reformed Broker)’s position on gold to ARTSTAQ, and emerging work more generally:

“One thing I do have a strong opinion on is whether or not it belongs in an investment portfolio. My opinion is that it does not. It’s utterly pointless as an investment in that there is no conceivable way to value it and it doesn’t do what its most vocal supporters claim it does. Stocks and real estate have historically been a better, more productive hedge against inflation. These are the facts.”

…and I’d advise curious readers to listen to them. [ARTnews]

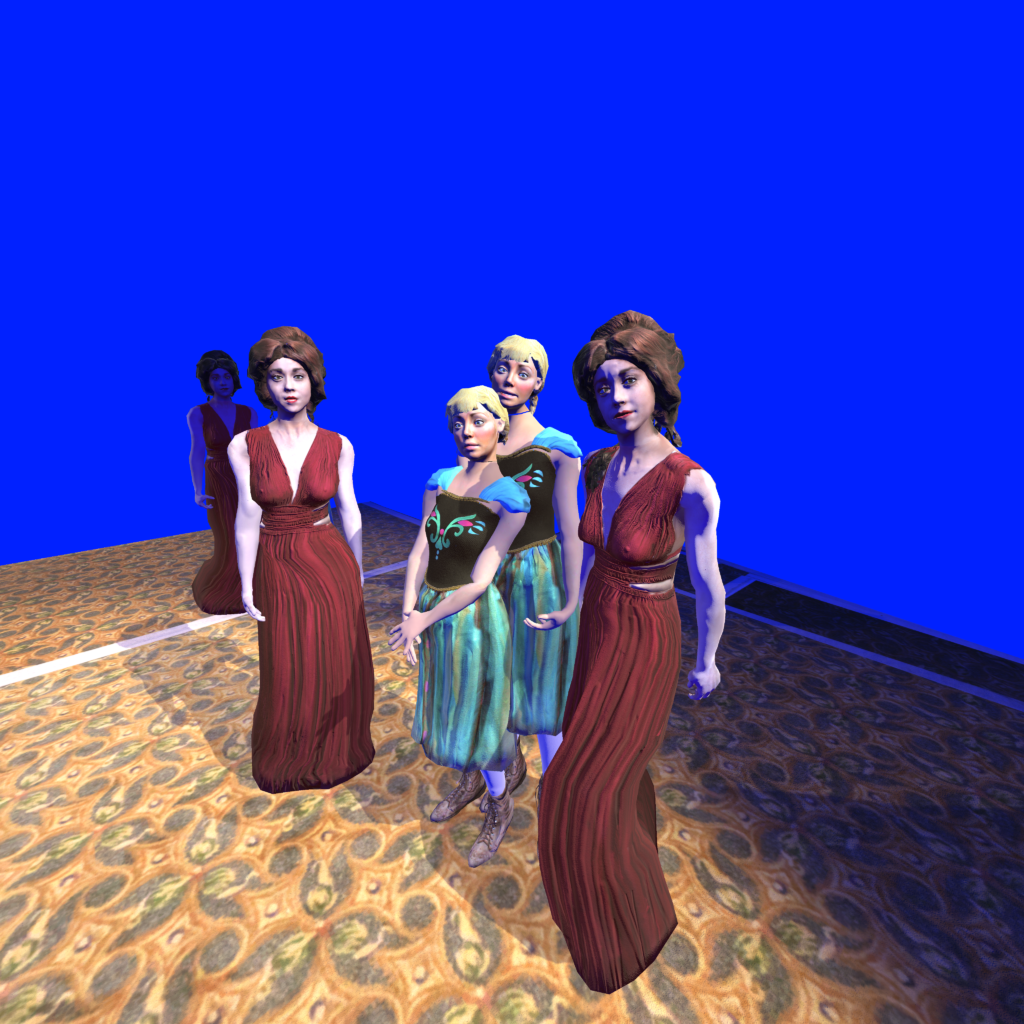

Paul McCarthy’s C.S.S.C. Coach Stage Stage Coach VR experiment Mary and Eve (2017). Virtual reality. © Paul McCarthy and Khora Contemporary. Courtesy the artist, Hauser & Wirth, Xavier Hufkens, and Khora Contemporary.

VIRTUALLY THE SAME: Among the 2017 Venice Biennale‘s official collateral events, the Faurschou and Cini foundations teamed up with Khora Contemporary, a Denmark-based virtual-reality production company “created specifically for artists,” to try to push serious visual practice deeper into virtual reality. But as so often happens, I think the venture’s business aspects are as noteworthy as its aesthetic ones.

Using HTC’s VIVE VR hardware, Khora debuted two newly commissioned works by two known art-world quantities in Venice. Christian Lemmerz’s La Apparizione (2017) confronts users with a colossal golden version of Christ crucified, which spews embers and molten gold from its wounds as death throes convulse its absurdly Marvel-esque physique.

Paul McCarthy’s CSSC VR experiment “what is your name?” (2017) immerses viewers in a spectacle of depravity centered on, in Scott Indrisek’s words, “a swiftly replicating group of female figures who saunter, molest, and abuse each other” (a nice reminder that “McCarthyism” means something totally different in the closed circuit of the art world than in the larger political and cultural realm).

While I applaud everyone involved here for exploring new technological horizons—particularly McCarthy, who becomes one of the very few already-successful septuagenarians rocking with new media right now—Khora’s biennale contributions also underline what I see as the central paradox of VR artworks: For every expectation they upend in terms of content or (simulated) experience, they still tend to be governed by the same economy of scarcity as the most traditional of artistic media.

Christian Lemmerz’s La Apparizione (2017). Virtual reality. © Christian Lemmerz and Khora Contemporary. Courtesy the artist and Khora Contemporary.

Case in point: As of now, only a select handful of collectors will be able to come to Bodybuilder Jesus, since La Apparizione is strictly offered in an edition of six. McCarthy’s work has 11 different variations, but each one is available in an edition of just five (technically, three + two artist’s proofs, but that artificial distinction calls for a whole other column).

And while Khora will try to expand the audience for their artistic collaborations by securing exhibitions at museums and foundations, the company will still only be able to do so using these measly rations—rations determined in large part by the artists’ galleries, who are solely responsible for selling the works, per my correspondence with Khora partner Sandra Nedvetskaia.

Like most, if not all, of the art industry’s other early adopters of VR, then, Khora is trapped in a commercial vise. Even though virtual-reality works exist as infinitely replicable software, their producers and distributors continue to deliberately restrict supply in the same way they would for, say, a sculptural edition.

That doesn’t mean virtual reality, augmented reality, or other new-media works are incapable of disrupting the longstanding fundamentals of art sales. It just shows that, so far, the art industry’s power brokers are much more interested in reproducing the old blueprint for success than in using new technological tools to make major revisions. [Artsy]

Works by Jean-Michel Basquiat, Andy Warhol, and Yayoi Kusama on view in London ahead of the spring sales at Sotheby’s New York this week. (Photo by Tristan Fewings/Getty Images for Sotheby’s)

ALL THE (ART) WORLD’S A STAGE: Finally this week, in advance of New York’s imminent May auction extravaganza, Sotheby’s reported better-than-expected first-quarter results—and more important, offered a crucial reminder of what the 21st-century gavel game has become beneath the surface.

While using the earnings call to celebrate his house’s ability to reduce losses by $14.6 million, increase revenue by $81 million, and grow private sales by 41 percent in comparison to the first quarter of 2016—amid other spreadsheet fodder that probably threatens to plunge the average reader into a fugue state—CEO Tad Smith mentioned a key detail about Sotheby’s strategy.

Despite offering $217 million in guarantees to actual consignors in its May auctions, the house has secured a $177-million hedge in the form of irrevocable bids by third parties. Or as my colleague Eileen Kinsella put it, “Essentially, Sotheby’s has already secured willing buyers for many of the most valuable works in the sales next week.”

Since Christie’s and Phillips are privately held companies, it’s unlikely that we’ll hear specific figures on how their offsets compare to Sotheby’s. But there’s little doubt that all three sellers are aggressively securing these risk-sharing agreements, likely to an unprecedented extent.

What this means in practice is that sales at the major houses, which are frequently cast as more freely competitive, spontaneous, and democratic than the high end of the private market, have largely become carefully stage-managed theater. In an update of the old political adage that war is too important to be left to the generals, auctions are now too important to the houses, consignors, dealers, and artists to be left to the bidders in the room.

Granted, this change makes auctions no less relevant to understanding part of what’s happening in the art market at any given time. But it does mean that consignors and auctioneers are now producing plays as much as they’re producing sales. And when the curtain raises on the next set of results, we would all do well to ask ourselves which aspects of the story we can believe in most—and who’s paying to communicate them from backstage. [artnet News]

That’s all for this edition. ‘Til next time, remember: Looks can be deceiving, but blind trust is the real killer.

You can read The Gray Market’s full archive, as well as the latest posts, here.