The Gray Market

Why (and How) Global Economic Chaos Will Hit the Art Market in Ways You Might Not Expect (and Other Insights)

Our columnist examines how multiple asset markets in free fall might impact an art market fixated on its own business.

Our columnist examines how multiple asset markets in free fall might impact an art market fixated on its own business.

Tim Schneider

ShareShare This Article

ShareShare This Article

Every Wednesday morning, Artnet News brings you The Gray Market. The column decodes important stories from the previous week—and offers unparalleled insight into the inner workings of the art industry in the process.

This week, stretching out the big picture…

Two years on from the U.S.’s first Covid lockdowns, a wide range of markets are melting down before our eyes. From stocks, to bonds, to cryptocurrencies, it seems that everything touted as a store of value or an opportunity for wealth creation badly wants to prove it is neither.

Select early results from this week’s major spring auctions might convince some observers that artwork could be a rare refuge from the mayhem. But anyone trying to separate the signal from the noise in this particular playground for global wealth has their work cut out for them. Even though I expect the rest of the sales cycle to produce several more bombastic results, deeper forward-looking indicators hint that harder times could be just over the horizon.

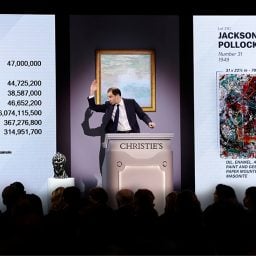

When I filed this column, the only completed evening sale was for the Thomas and Doris Ammann estate. Still, it introduced the conflicting narratives I expect to see reappear across the other marquee May auctions.

Bidders jumped off by careening drunkenly through an $80,000 high estimate to pay $1.26 million for a painting by Mike Bidlo, a nearly 70-year-old conceptual artist I cannot recall seeing in an evening auction before. It closed with the anticlimactic sale of Andy Warhol’s Shot Sage Blue Marilyn (1964)—which, at a premium-inclusive $195 million, set a new high mark for an American artist’s work at auction (after quickly stalling out at a $170 million hammer price).

The Ammann sale’s grand total reached $317.8 million with fees, within its presale estimate range but still more than $100 million south of its $420 million top projection. And beyond the bounds of New York’s auction houses, valuations for other assets were plunging with breathtaking speed.

Andy Warhol, Shot Sage Blue Marilyn (1964). Photo: Christie’s Images Ltd.

On Monday morning, the New York Times DealBook noted that the S&P 500 had “now registered five consecutive weekly declines, its longest streak of losses since June 2011,” a trend lowlighted by the index’s most significant one-day drop since COVID emerged. Michael Batnick, managing partner of Ritholtz Wealth Management, tweeted that Amazon, Facebook, and Netflix were all in their “deepest drawdown of the last 10 years,” as each company’s share price tumbled between 37 percent and 72 percent from its respective apex during that span.

Cryptocurrencies were a horrorshow, too. The price of Bitcoin was down about 38 percent year-to-date (from nearly $48,000 to $30,000) on Monday, while the price of Ether was down about 41 percent (from $3,766 to $2,228) over the same period.

If that weren’t enough, the Federal Reserve just hiked interest rates 0.5 percent, the largest such increase in 22 years. Inflation in the U.S. economy is still a runaway train hurtling past 8 percent, worse than it’s been in decades (even after new data showing a slight ease in April). Russia’s war on Ukraine is still elevating global gas prices and mangling global supply chains; and China’s economy is still being choked by the combination of Omicron’s blitz through the population and the state’s iron-fisted lockdown measures to try to stop it.

Does all this make Christie’s evening sale of the Ammann collection the new “Beautiful Inside My Head Forever,” the hugely lucrative 2008 Damien Hirst auction at Sotheby’s London that unfolded only hours after Lehman Brothers collapsed to usher in the Great Financial Crisis? Personally, I wouldn’t go that far.

I do think the signs suggest we’re facing a macro market correction that will bring art valuations closer to earth in the foreseeable future, and that the art economy would do well to start prepping for the descent now. But since even the inevitable is not necessarily immediate, let’s game out the most important dynamics influencing art sales across three different vectors.

The interior of Anne H. Bass’s New York City Home, with artworks by Mark Rothko and Claude Monet. © 2022 Visko Hatfield. Courtesy of Christie’s.

Timing isn’t everything in the art market, but it sure does account for a lot. Much of the excitement from the May auctions comes courtesy of collections that were essentially forced into availability, headlined by the estate sales for Anne Bass and the Ammanns, as well as part two of the Linda and Harry Macklowe separation sale. The reaper doesn’t care about your scheduling preferences, and neither do fed-up judges in divorce courts. The Big Three houses should be thankful on both accounts this time around.

It’s also hugely beneficial to the trade that the broader asset-market nosedive only went low enough to trip alarms well after the rest of this auction season’s offerings had been locked in. As veteran hammerman Simon de Pury told me for a story on auction-sector resilience during a recession, “What dries up in down markets is discretionary consignments.” In other words, collectors who don’t have to sell when the economy looks shaky, tend not to—especially if the works in question are top-tier.

Auction data supports de Pury. In 2009, the first full year of the Great Financial Crisis, the number of pieces consigned worldwide with a low estimate between $1 million and $10 million dropped almost 60 percent, to just 443. Meanwhile, the number of works consigned with a low estimate of $10 million or higher dropped nearly 75 percent, to just 12. (Broadly similar but less severe declines occurred in the 2016 mini-downturn.)

The irony is that this trend is self-defeating. Genuinely great works have a history of selling for strong prices even during broader market declines. Banner results from 2009 underscore this point. That February, a trove of works owned by Yves Saint Laurent and Pierre Bergé at Christie’s set six artist records and brought $484 million in sales, the largest sum ever paid for a private collection at the time. Nine months later, Andy Warhol’s 200 One Dollar Bills (1962) flew to $43.8 million, more than 3.5 times its most optimistic presale expectation as part of a propulsive Sotheby’s sale that de Pury credits for starting to resuscitate “the most morose market ever.”

What about lots priced south of the mountaintop this week and in future sales cycles? This question leads us to think about…

Anna Weyant, Summertime (2020). Courtesy of Christie’s Images, Ltd.

Here is where things start to get interesting, particularly in the context of macroeconomic turbulence. Tech companies and other would-be growth stocks have been disproportionately responsible for the carnage among equities to date. Based on the parallel market dynamics, this could spell trouble for the breathlessly pursued band of young artists whose auction prices have been blasting off to unprecedented heights at unprecedented velocity.

After reviewing a slew of stock-market data, Bloomberg Opinion columnist John Authers found “overwhelming” evidence that “the previously most overblown speculative stocks” are taking the hardest hits. To me, his most damning example is the swoon of the ARK Innovation ETF, tech investor Cathie Wood’s index fund tracking Silicon Valley’s hottest companies. After trouncing the average return of the S&P 500 since 2016 (including by as much as 300 percent during the first year of the pandemic), “all of ARK’s advantage for the last five years [had] evaporated” by the end of Monday’s selloff, Authers wrote.

Elsewhere, new research from Morgan Stanley showed that “meme investors who jumped into the market in early 2020 have now given up all their gains,” in the words of Bloomberg analyst Tracy Alloway. Accelerating the trend is the aforementioned dive in the price of cryptocurrencies, undoubtedly the most high-risk, high-reward growth assets (or “assets,” to critics) of the past two years.

Other data bolsters the notion that investors are retreating to value and stability. As of Monday, the only six stocks up 100 percent or more over the past year were all oil and gas companies. Derek Thompson of the Atlantic categorized some of 2022’s best performers as creating the foundation of “the Medieval economy.” They include U.S. Steel; meat manufacturer Tyson Foods; fertilizer giant Nutrien; the parent company of agribusiness colossus Monsanto; and construction and lawn-care equipment makers Caterpillar and John Deere.

Authers also noted that stock prices for producers of consumer staples—that is, essential goods like food and beverages, cleaning supplies, and personal-hygiene products—are now the richest they’ve been compared to consumer discretionary stocks—makers of inessential items like cars, electronics, apparel, and luxury goods—since the darkest days of the Great Financial Crisis.

Wayne Thiebaud, Little Deli (2001). Courtesy of Christie’s Images, Ltd.

Why the about-face from investors? The simplest explanation is that wealth tends to gravitate toward future-focused stories about explosive growth when interest rates are low (let alone near zero). Who cares about present-day profits when it’s almost free for a company you’re backing to borrow money in pursuit of initiatives that could lead to long-term market dominance? Better to take a bigger risk with enormous upside than play it safe. When interest rates rise, however, present-day factors like costs and earnings tend to suddenly return to prominence in investors’ minds, making value more alluring than growth potential and inverting judgments about what constitutes a smart use of capital.

Bleak as these signals might sound for the entire cultural economy, period, the likeliest outcome is that the next downturn in art sales will be as selective as the current downturn in stocks. Daniella Luxembourg, who had more market wisdom decades ago than I ever will, once told me, “It doesn’t always affect all the works of art” if the market enters an extreme low (or high). “It just affects the fashionable, of-that-moment works of art.” I also wouldn’t expect too many outsize performances from grade-B works by grade-A artists, let alone material further down on one or the other hierarchy.

But this isn’t to say that we should brace for a slew of flops at the Big Three’s contemporary and ultra-contemporary-focused evening auctions this May. In fact, I’d bet that several works by rising stars will vault multiple times over their high estimates.

The reason? It’s notoriously difficult to predict how long a euphoric growth narrative can withstand the sobering influence of reality in any market. Collaborative Fund partner and author Morgan Housel noted that every classic, textbook valuation metric confirmed that prices for the original tech stocks “looked crazy” by 1995–96, but it took another four to five years before the dotcom bubble actually burst.

Similarly, critics have been prognosticating an imminent collapse of the new tech stocks since 2011, and we may only be experiencing it now, 11 years later. Although I expect art buyers to see through the growth mirage faster in our niche economy, there’s no guarantee that they necessarily will. My sense is that their reaction time will depend on larger uncertainties whose contours are still coming into focus.

As painful a time as investors have had since April, recency bias is making the damage feel worse than it is. At the start of May, Housel noted that the U.S. stock market was down 14 percent year-to-date—but that the average peak-to-trough swing in any given year during the previous 100 years in the stock market has been 13.5 percent. Losses have mounted between when he made that proclamation and now, but they are still within range of the same ho-hum historical standard.

Yet the experience of the downturn is far more stomach-turning because the preceding two years has been so exceptionally profitable for so many participants. Expectations are even further away from a healthy, historical norm because at least an estimated 20 million new retail investors have entered the market since the start of 2020, per JMP Securities. Many of them have been able to double their money every six months by piling into meme stocks (to say nothing of cryptocurrencies and NFTs). Their atypical, unsustainable rise in portfolio value amplifies the panic produced by today’s basically typical, foreseeable decline.

While very few of these COVID-era day traders have been propping up the establishment art market, it has benefited from a broader buyer base and major spending by a growing demographic of young, wealthy collectors, especially in East Asia. They too have never seen the value of their acquisitions (or their broader portfolios) do much of anything besides go up. We should find out soon whether they are more willing to shrug off a tightening economy than the millions of young retail investors losing their minds in the stock-market drawdown.

A scene at West Bund Art & Design 2021, Shanghai. Courtesy of West Bund Art & Design.

One tidbit from my colleague Katya Kazakina’s report on the Ammann evening sale stands out against this context: “Asian bidding was thin throughout the sale, with only 10 percent of Asian participation, compared with 45 percent of American bidding, according to Christie’s. The Hong Kong salesroom was quiet when the Marilyn came up. And Middle Eastern bidders didn’t seem to materialize, either.”

China and its political climate loom especially large when it comes to calculating fine art’s odds of fending off a market correction (or worse). We are now several months into president Xi Jinping’s push for “common prosperity,” or a narrowing of the Chinese wealth gap pursued partly by clamping down on elites ranging from “tech billionaires to film stars, social media influencers [to] private tutoring start-ups,” per the Financial Times.

The new campaign is both a resurrection and an expansion of a previous wealth purge that spanned four years, shaved billions of dollars off the global luxury market, and precipitated a nationalist drive toward domestic brands. The East Asian collecting pool is larger than just China, of course, but a population of newly chastened Chinese plutocrats certainly won’t help international art sellers’ results.

There is no telling how, exactly, these different economic factors will influence the art market’s trajectory for the remainder of 2022, let alone beyond it. But to me, the number, severity, and duration of the headwinds hitting the global investor class right now seem too great for the art market to escape a slowdown before the year is out. Whether the market correction becomes a crisis depends on how participants react to elements beyond their control.

That’s all for this week. ‘Til next time, remember: everything looks obvious in the rearview mirror.