The Gray Market

Why the Art Industry Should Brace Itself for the Permanent Staycation Era (and Other Insights)

After surveying the travel landscape, our columnist finds the strong Euro flavor of Art Basel 2021 is a taste of more regionalism to come.

. Commissioned by LaGuardia Gateway Partners in partnership with Public Art Fund for LaGuardia Airport’s Terminal B. Photo by Nicholas Knight, courtesy of the artist; LaGuardia Gateway Partners; Public Art Fund, NY; Tanya Bonakdar Gallery, New York/Los Angeles. ©Sabine Hornig and VG Bild-Kunst, Bonn Germany.")

After surveying the travel landscape, our columnist finds the strong Euro flavor of Art Basel 2021 is a taste of more regionalism to come.

Tim Schneider

ShareShare This Article

ShareShare This Article

Every Wednesday morning, Artnet News brings you The Gray Market. The column decodes important stories from the previous week—and offers unparalleled insight into the inner workings of the art industry in the process.

This week, another blow to art-business exceptionalism…

Last week, at least one consensus observation emerged from the first live Art Basel to be held since the pandemic’s onset: few U.S.-based collectors and advisors made the trip, lending the fair a distinctly more European character than it has had in many years. But was this shift a one-time anomaly caused by Delta-variant fears and an unusually volatile set of entry requirements for both Switzerland and the fair itself? Or was it a first glimpse into the art industry’s version of the more travel-selective, regionally focused business world predicted by analysts across economic sectors since the early spring of 2020?

Based on broader trends in business travel, I’m increasingly leaning toward the latter option—and the next two months will help clarify whether the art market is the exception or the rule.

Before we try to look forward, though, let’s look back. In July, I wrote a column about a growing body of evidence suggesting that life in high-income countries (and as a consequence, their art industries) would undergo far less long-term change than many experts forecast during the depths of the Covid-19 crisis, even when it came to three extremely popular predictions:

By midsummer in the U.S., each of these widely held prognostications looked like it was standing on legs made of boiled spaghetti. Giants in tech and finance were already calling much of their respective workforces back to the office, from Google and Twitter to Goldman Sachs, Barclays, and Blackstone. Migration patterns into and out of major cities had largely stabilized to pre-pandemic levels, with the median home price in San Francisco surpassing its prior high by more than $300,000. At least three major U.S. airlines—American, Delta, and Southwest—reported Q2 profits, with Delta’s CEO declaring that “domestic leisure travel is fully recovered to 2019 levels.”

Yet there was one important footnote in the story of the airlines’ recovery: business and international travel in 2021 were still stuck far below the heights they had achieved two years earlier, no matter which time horizon you considered. In July, multiple airline executives expressed confidence that we would see these areas “improve meaningfully over the coming months,” in the words of New York Times business reporter Niraj Chokshi. The heads of American, Delta, and United Airlines also agreed that they had seen no drop in demand for bookings because of concerns about the Delta variant, which had by then become the dominant virus strain in the country.

So what has happened to U.S. air travel since then? The recovery slammed into a barrier it has not been able to bust through.

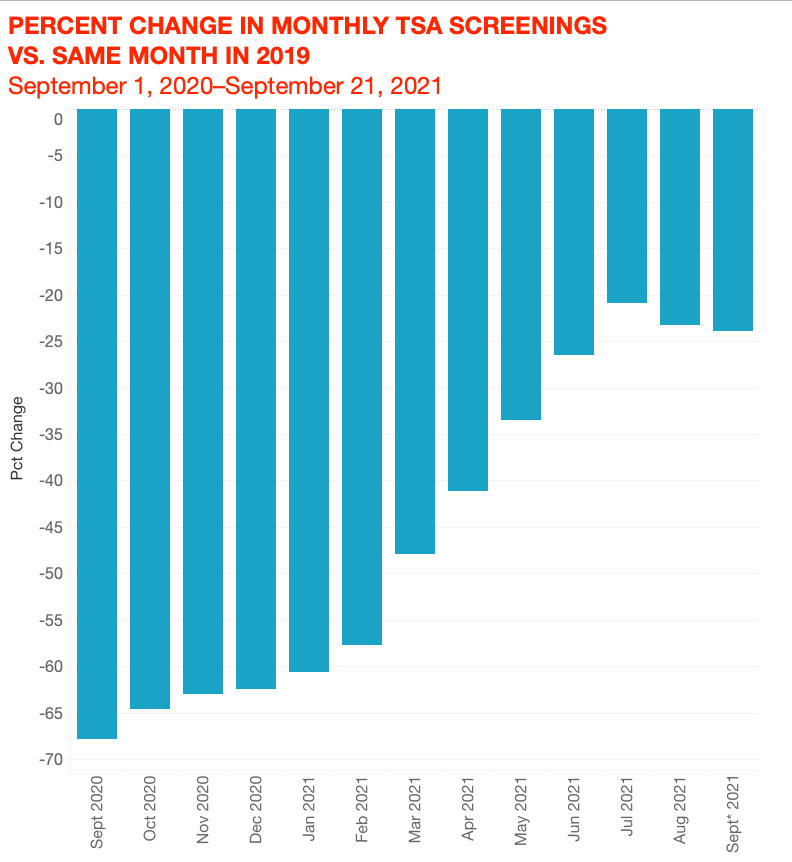

Data by Sivak Applied Research. Chart by Artnet News.

What you’re seeing in the chart above are the percentage changes (adjusted for population) in the number of monthly Transportation Security Administration (TSA) screenings at U.S. airports compared with their 2019 equivalent, courtesy of data from transportation analyst Sivak Applied Research. The trend is unmistakable. After 11 consecutive months of improvement, the number of passengers screened by TSA peaked during July 2021—then went back into decline over the next 51 days. (The data for September 2021 covers only the first 21 days of the month.)

Ironically, then, just days after those U.S. airline executives were crowing about the industry’s bounce back in the press, travelers started backing away from booking again. At least four airlines, including two that had posted profits the previous quarter (American and Southwest), were warning investors in August that they would underperform quarterly financial projections, “a trend they blamed on rising cases of the Delta variant,” according to CNBC.

Business trips have taken the worst beating. Much of the travel industry’s optimism in July anticipated a return to the long-established seasonal cycle: vacationers own the sky every summer, and corporate warriors surge back into the air every fall. But a survey conducted in mid-August by Morning Consult and the American Hotel and Lodging Association found that almost 70 percent of responding business travelers were likely to take fewer trips due to Covid dread, and 52 percent were likely to cancel their existing travel plans, with no intention of rescheduling.

Data from Deloitte painted a similarly stagnant picture. Based on a poll of 150 travel managers, the firm projected that fourth quarter 2021 travel budgets at U.S. corporations would only be about 25 percent to 35 percent of their fourth-quarter 2019 equivalents. Nor did the findings anticipate a full recovery by the end of next year; Deloitte forecast that fourth-quarter 2022 spending on business travel would still land between just 65 percent and 80 percent of 2019 standards.

Yet the most sobering aspect of Deloitte’s research only emerges in the fine print. The survey was conducted from May 28 to June 10—a period during which the pandemic’s grip on the U.S. was among the loosest it has had since reaching here in the spring of 2020, per the New York Times. Compared to June 10, however, the country’s current seven-day average counts of infections have increased about 8X (to 118,000), while hospitalizations have increased about 4.5X (to more than 85,000), and deaths have increased about 5X (to more than 2,000 per day).

Call me a cynic, but I’m betting those ghastly leaps have convinced many of the same companies represented in the survey to dial back their travel budgets even further for the foreseeable future.

British Airways planes parked at Gatwick Airport. Photo by Gareth Fuller/PA Images via Getty Images.

What’s the short- and medium-term future of travel in the art business, then? I think the best answers require asking two more specific questions: Where do you want to go, and where are you starting the trip?

International exchange should increase markedly once the U.S. (finally) removes entry restrictions on fully vaccinated passengers flying out of 33 countries headlined by the E.U. and China in November. At the same time, art pros intent on traveling abroad should prepare for more regulatory headaches like the ones that surrounded last week’s edition of Art Basel, not less. As one bespoke travel agent recently told CBS News Moneywatch about international trips, “People have held out for this idea that we’ll get vaccinated and the world will be exactly like it used to be. Everyone in the travel industry realizes this is a long-term thing, and everything is a lot more complicated and will remain more complicated.”

So between health concerns, red tape, the appeal of cost savings, and an increasingly robust body of proof that remote participation can often still get the job done, I would expect members of the art trade to stay highly selective about when they really need to travel abroad through next year at least. That doesn’t mean everyone will chuck their passports into storage until 2023. But my guess is that both the buy and sell sides of the industry are likely to think (and keep thinking) much harder about which relationships, negotiations, and events require high-touch globe-trotting.

Regional and domestic business travel stands a better chance of holding strong, regardless of whether we’re talking about the U.S. or elsewhere. Remember, the data from Sivak Applied Research shows only a slight retrenchment in monthly TSA screenings since July, not a dramatic drop-off. While founder Michael Sivak was unwilling to make projections about the future, he noted in an email to me on Monday that domestic “interstate travel (in miles) by passenger vehicles”—basically cars, trucks, and vans—“is essentially back to where it was in 2019.” In other words, I’ll wager that last year won’t end up being the last time that some dealers and collectors refused to fly to Miami Art Week, but were still willing to drive there.

Suitcases from the limited-edition RIMOWA x Alex Israel series. Courtesy of RIMOWA.

An even more robust regionalism seems to be manifesting abroad. Reuters relayed on September 9 that Lufthansa had “seen demand for its regional flights between Germany, Austria, Switzerland, and Belgium jump 15 percent in recent weeks, and rise 30 percent for flights within Germany.” That data certainly tracks with the crowd at last week’s Art Basel being both solid in size and overwhelmingly European in character, without being totally homogenous.

I would anticipate that much the same scenario will play out at Frieze London and FIAC in the weeks ahead. China’s rich slate of fall fairs, headlined by Art021 and West Bund Art and Design, should also be as dominated by locals and other East Asian buyers as they were last year, when onerous regulations meant foreigners had to quarantine for weeks ahead of the events to participate. Art Basel Miami Beach will likely complete the set by being even more American and Latin American than in years past.

Each of these events will have their own variations based on each country or bloc’s particular health protocols, which are liable to change at almost any time in response to developments both worldwide and in specific countries. In general, however, we should expect the “global” art market to feel more regional for a long time to come.

That’s all for this week. ‘Til next time, remember: We might all be traveling the same terrain, but there are infinite routes through it.