Analysis

How Is Western Art Really Faring in Asia? 3 Trendlines From Hong Kong’s Spring Auctions Reveal the Changing Market

Asian, postwar, and fine art are by far the most bankable categories in Hong Kong.

Asian, postwar, and fine art are by far the most bankable categories in Hong Kong.

Tim Schneider

ShareShare This Article

ShareShare This Article

In recent years, Hong Kong has transformed in the eyes of the Western art industry. Formerly a destination that warranted attention primarily during Art Basel Hong Kong and a few scattered auctions, the region now hosts permanent spaces from many of the most powerful galleries in the world, while Christie’s, Sotheby’s, and Phillips are all seeking to expand their influence there in various ways.

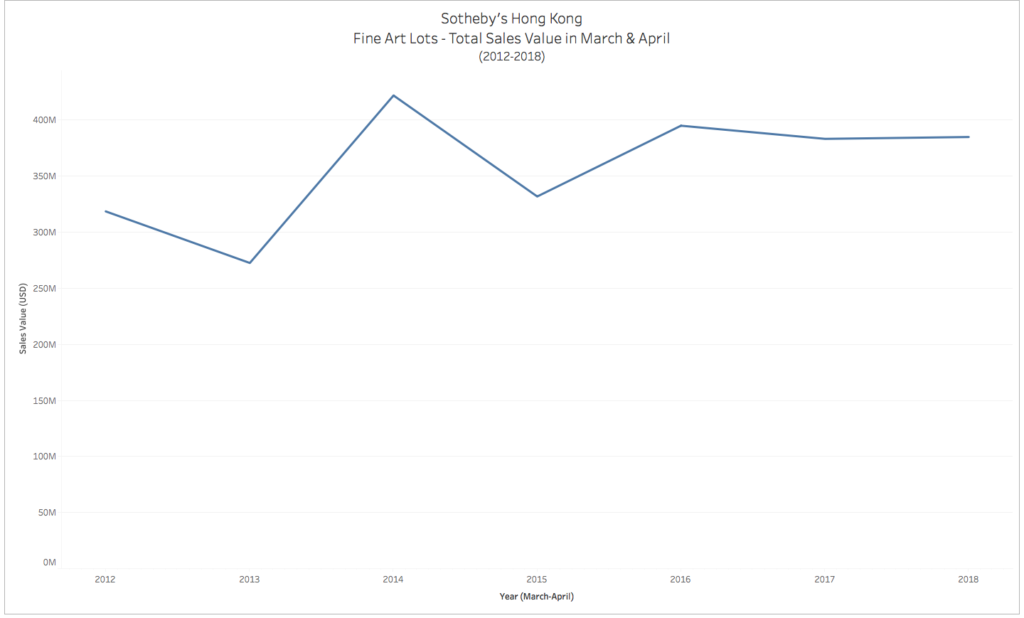

So far, this season’s auction results suggest that the market’s steady expansion shows no sign of abating. Sotheby’s Hong Kong closed its main group of spring auctions on April 2 with $466.5 million in reported sales across all categories (and one epic, 40-minute bidding war). The vast majority of the total owed to continued strong performance in fine art sales, which generated just shy of $385 million.

While not an all-time high, that haul is among the highest since 2012 (the first year of data available from Hong Kong in the artnet Price Database).

For historical perspective, the chart below shows the total sales value for fine art lots at Sotheby’s Hong Kong during March and April, from 2012 through 2018.

But this is only one snapshot of auction sales in the bustling region. For deeper insights into recent activity at major spring auctions in Hong Kong, we took a deep dive into the historical data.

A few explanatory notes are in order before we get into the analysis.

With that context in mind, here are three major takeaways from the data.

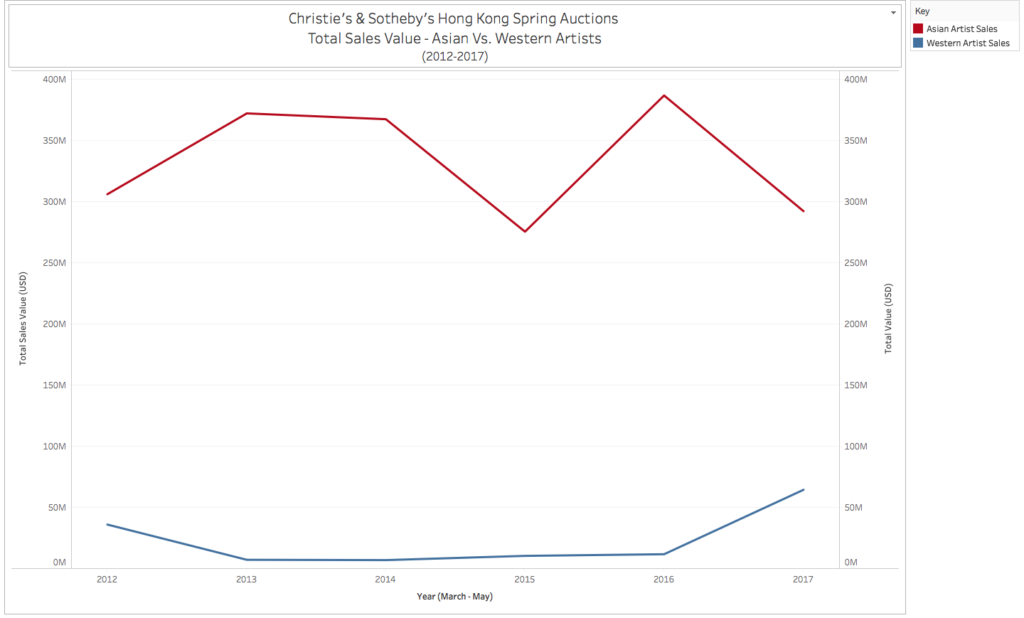

The first chart below shows the total sales value for fine art lots by Asian artists (in red) and Western artists (in blue). The picture could hardly be starker.

In relative terms, interest in Western artists has surged since 2016, with total sales of their works at auction reaching a high of $64.4 million in spring 2017.

However, even with total sales of Asian artists’ work declining during the same year to their lowest value since 2015, the gap between east and west still stood at nearly $228 million—over three and a half times the Western artists’ total.

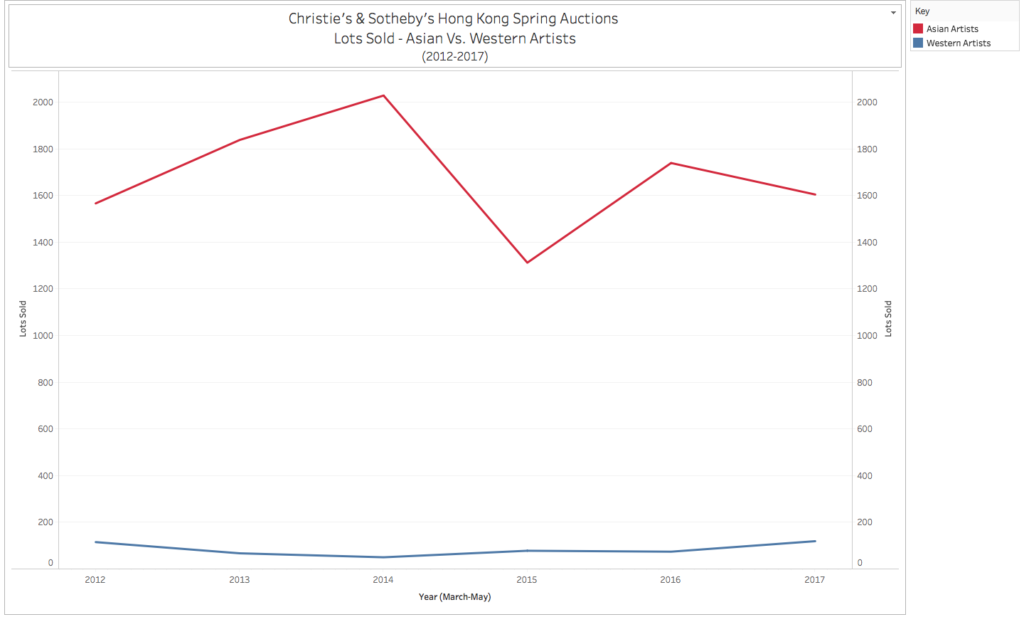

You might suspect this gap is due to the fact that Asian artists’ work is simply selling for higher prices than Western art. Not so. Asian artists also sell dramatically better in terms of sheer quantity.

To date, Christie’s and Sotheby’s—combined—have never sold more than 119 lots by Western artists during the spring auction cycle. Meanwhile, they have never sold fewer than 1,312 lots by Asian artists.

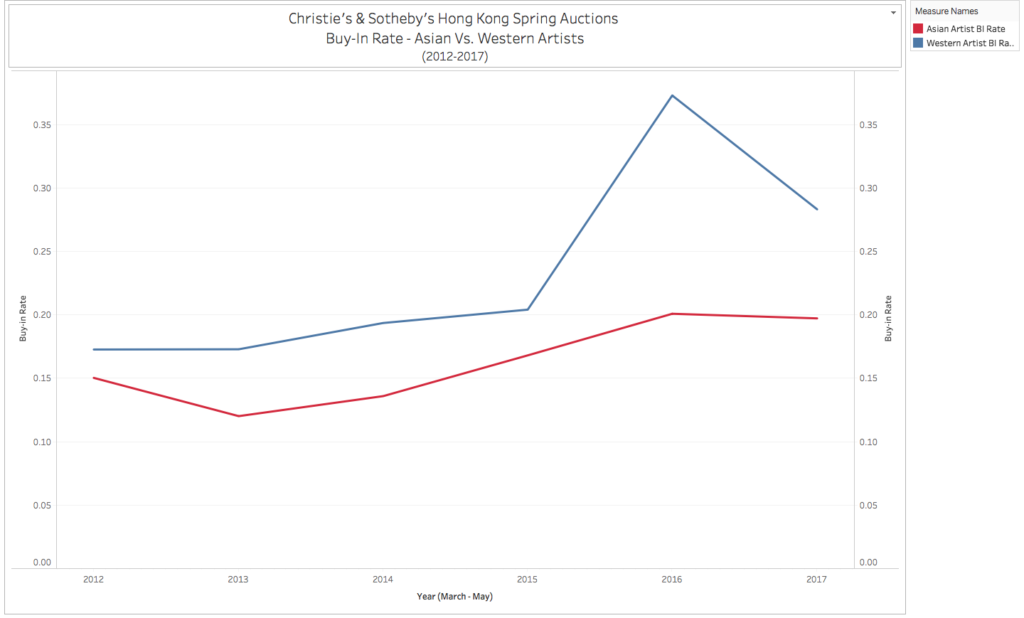

Buy-in rates tell a similar story. On the whole, Asian artists have been significantly more likely to sell at auction than Western ones.

The buy-in rate for Asian artists has hovered between 12 and 20 percent since 2012. And while that figure was on the uptrend from 2013 to 2016, the same could be said for Western artists, whose buy-in rate has never once been lower than their Asian peers—and spiked to a lofty 37 percent in 2016.

The bottom line: Western artists could gain steam in Hong Kong’s primary market thanks to outreach and initiatives from major Western galleries, and auction houses clearly believe there is plenty of room for growth for Western artists in the private resale market. But by any metric, the numbers haven’t shown much progress in that department yet.

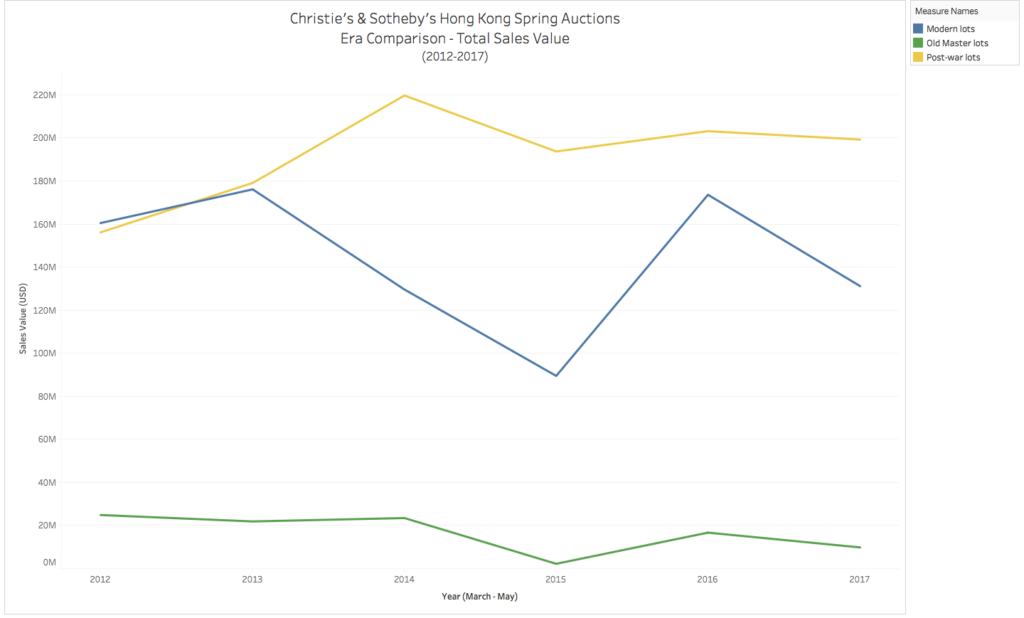

If you want to sell art in Hong Kong, you are most likely to be successful if that art is from the postwar period. The category (which we defined as work by artists born after 1910) led the way in every year except 2012. Although the sector crested in 2014 at nearly $220 million, it also proved to be the least volatile of the three eras we examined (postwar, Modern, and Old Masters)—including during China’s stock market turbulence in 2015.

By contrast, the total sales of Modern work (which we defined as by an artist born between 1821 and 1910) fluctuated significantly from year to year, plummeting sharply over two years from its 2013 peak of $176 million to $89.5 million in 2015. It rebounded in 2016 to $173.6 million—near its historical apex—before declining again last year.

Meanwhile, Old Masters (defined as work by artists born in 1820 or earlier) operated at their own low altitude. After hovering between roughly $22 million and $25 million from 2012 through 2014, the category took a nose dive to just $2.2 million in total sales in 2015. Its recovery has been uneven, too, as the works sunk back beneath the $10 million mark in 2017.

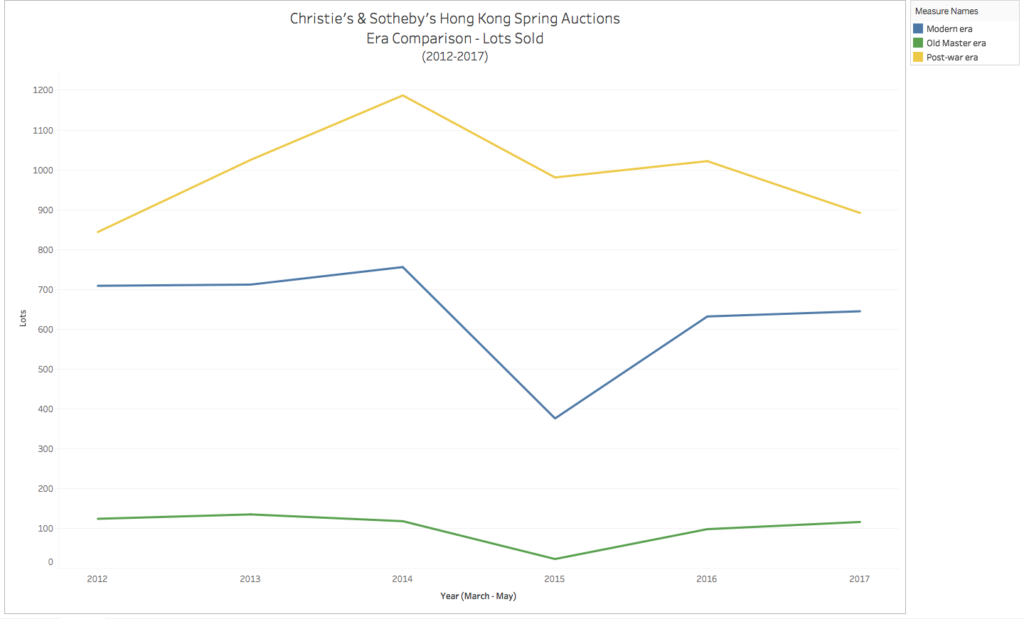

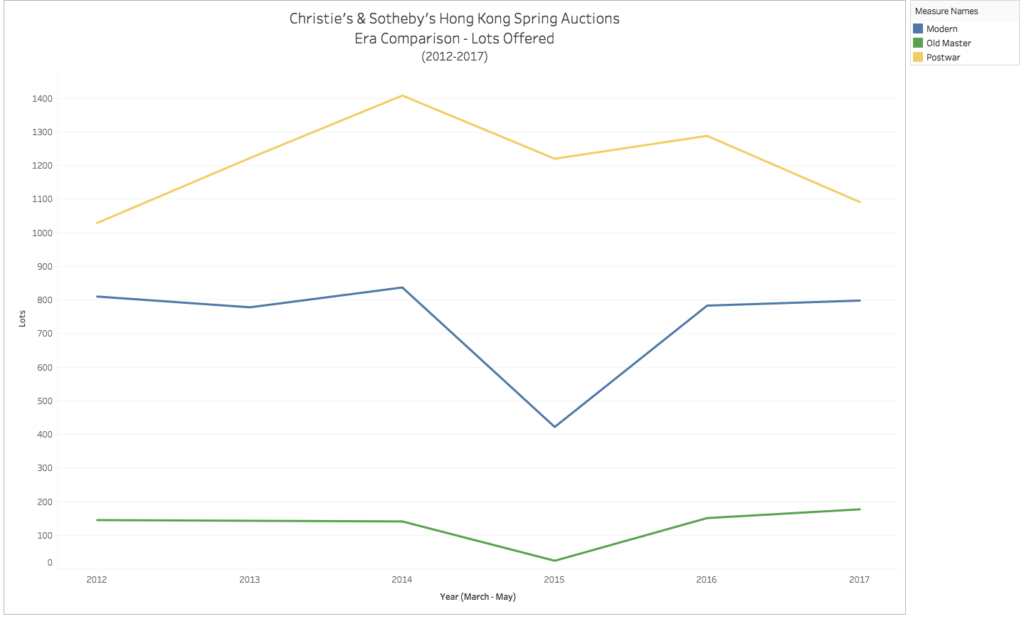

We see these same basic trends mirrored in the number of lots sold and the number of lots offered: Postwar art leads, with Modern art behind, and Old Masters following in a distant third place.

But while buyers’ category preferences have remained relatively consistent, there has been another notable shift in their behavior during this period: Collectors of postwar art seem to have gravitated toward higher priced lots, while the opposite is true for Modern and Old Master buyers.

Here’s how we can tell: Although there were significant drops in the number of postwar lots sold (a drop of 130 lots) and offered (a drop of 197) between 2016 and 2017, the total sales value for the category declined less than $4 million. This indicates collectors of postwar art are buying less—but what they do buy is more expensive.

The opposite was true in the Modern and Old Master sectors last year. While people actually sold more lots of both types in 2017 than in 2016, the total sales value in both categories declined in 2017. This indicates the works that found buyers were actually lower-priced on average than previously.

This dynamic is most extreme in the Old Master category, where the average lot last year sold for around $55,500—almost exactly half the average in 2016, and the lowest value in our sample—despite a six-year high in the number of lots offered.

The bottom line: Postwar works lead the field in terms of both supply and demand, and the market for Modern works has been fairly healthy (if somewhat more volatile). But the measurable chill in the Old Master sector makes for a great value opportunity for Hong Kong buyers—and plenty of sleepless nights for Old Master dealers.

For all the press about Chinese buyers clamoring to buy Château Lafite, fine art outshines wine—and every other category—in the Hong Kong auctions.

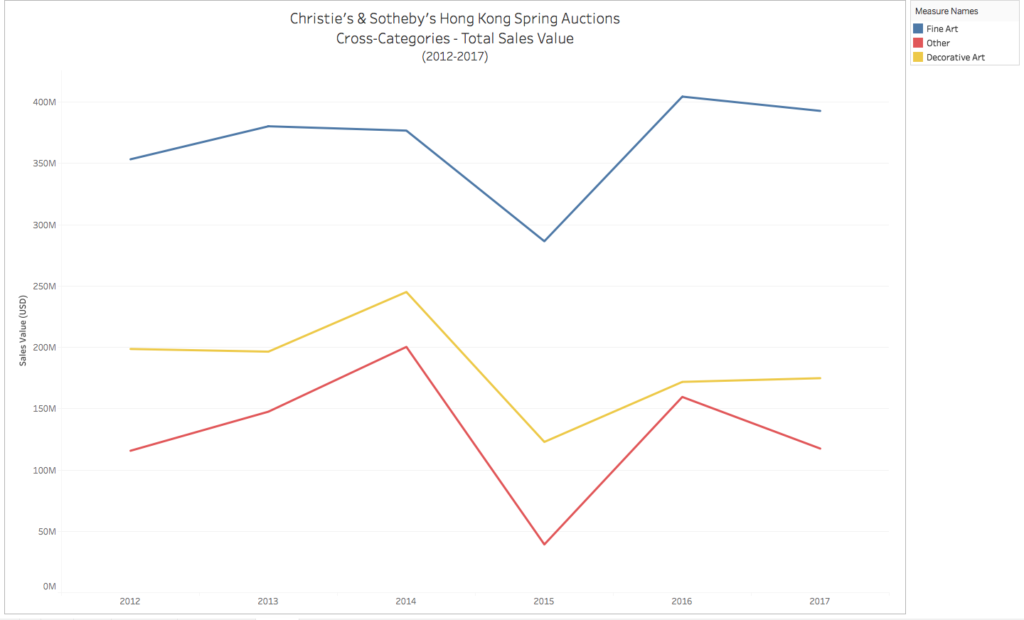

The following chart shows the total sales values for each of three categories: fine art, decorative art, and a catch-all labeled “other” (which includes jewelry, watches, wine, furniture, and everything else that does not fit neatly into either of the first two categories).

The chart tells us that fine art has not just been the unquestioned sales leader since 2012. It is also the only one of the three categories that rebounded to new heights after the Chinese stock market’s crash in 2015.

Even after declining from a 2016 high, fine art’s roughly $393 million total in 2017 still soared above every other year in the sample. And although decorative art climbed for two consecutive spring auction cycles after the 2015 turbulence, its nearly $175 million in 2017 sales still submarined beneath results in 2012–2014.

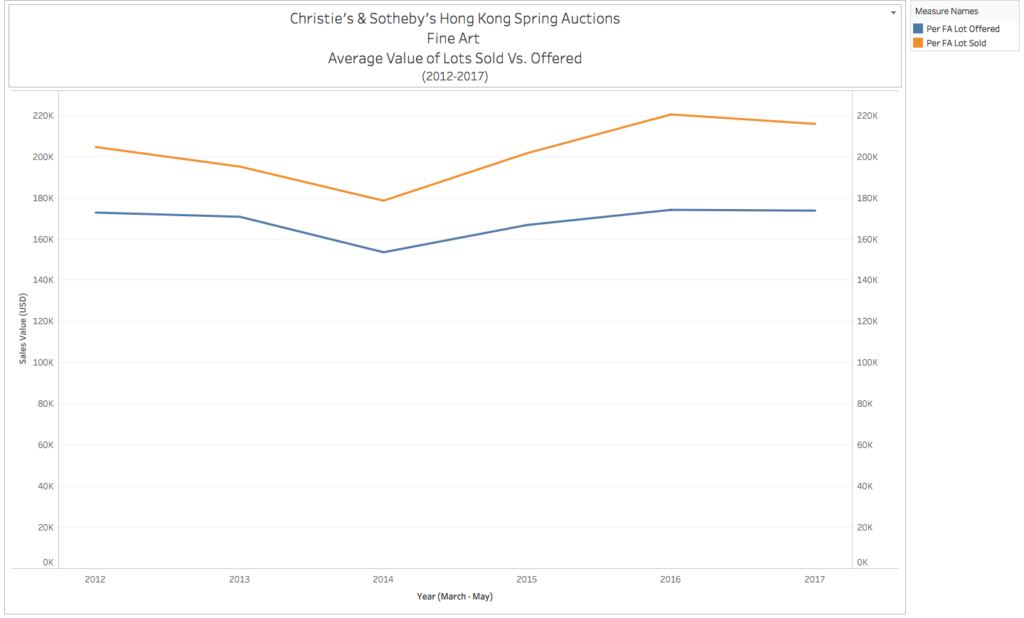

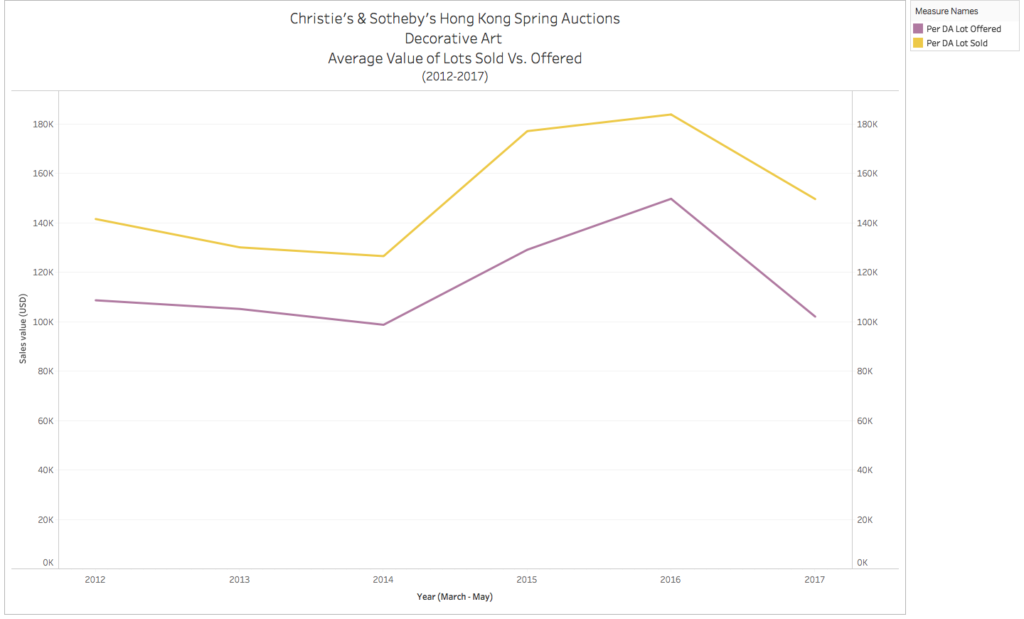

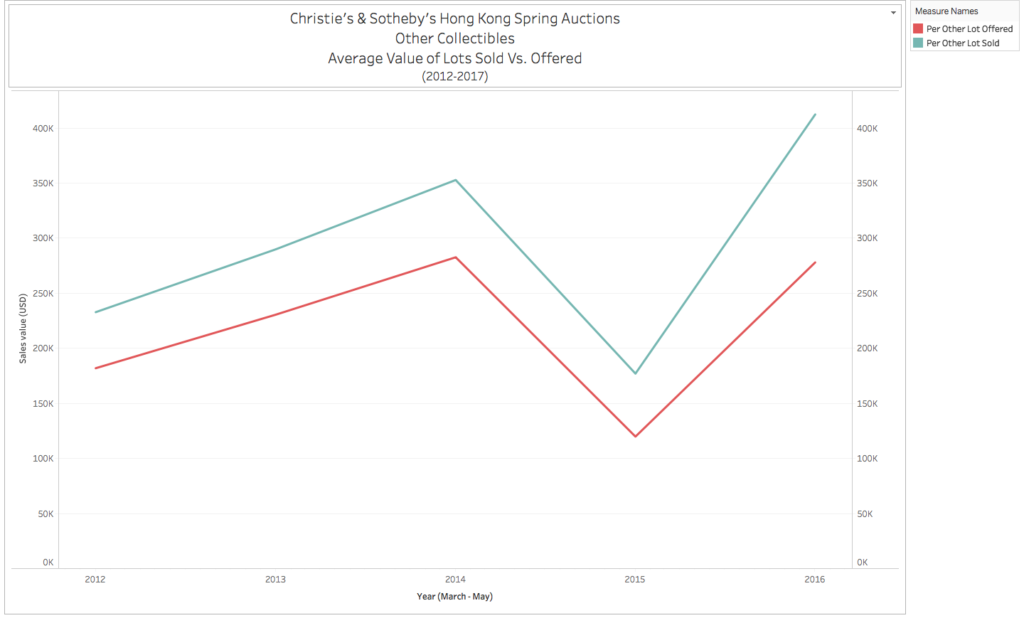

To drill deeper into the trends within each market, it’s useful to consider a different data visualization. The following charts compare two metrics—average value of lots offered versus average value of lots sold—across the fine art and decorative art categories.

This comparison gives us some sense of buyers’ relationship to price tiers. The greater the gap between average value of lots sold and average value of lots offered in a given year, the more that year’s auction totals owe to the sale of fewer lots at higher prices—in other words, a thinner market more polarized toward the top.

Notably, for both categories, the year of the Chinese stock market crash saw a move toward polarization in both markets, as the gap between average value of lots sold versus offered increased relatively sharply. But while both markets took a downturn from 2016 to 2017, fine art became slightly less polarized toward the top, while decorative art’s disparity widened again.

The main point is this: Amid the crash in 2015, buyer interest in both fine art and decorative art moved toward fewer higher-priced lots, suggesting a retreat toward “sure things” during a chaotic period.

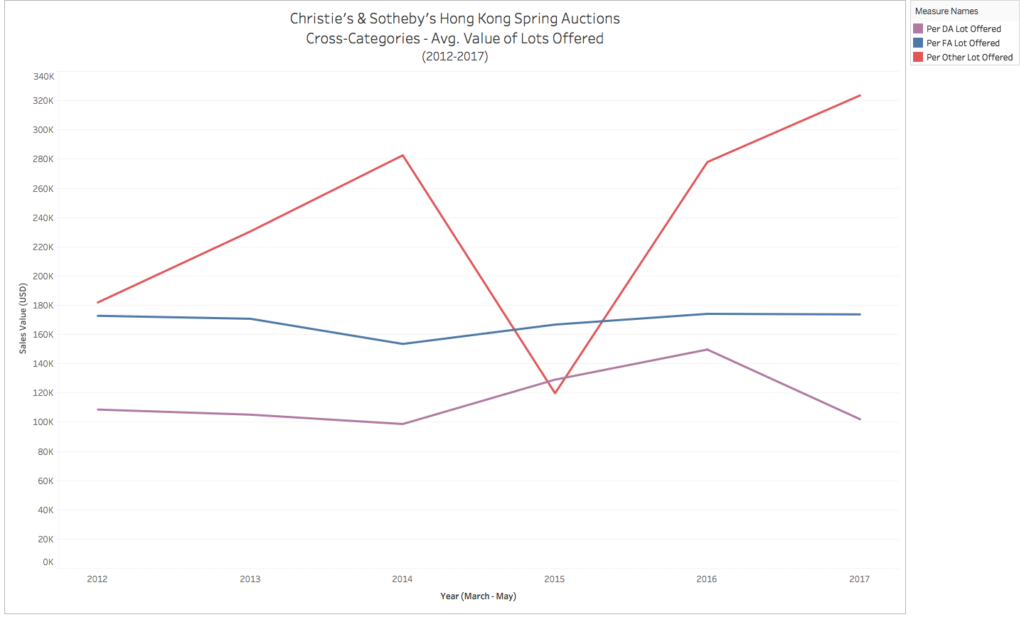

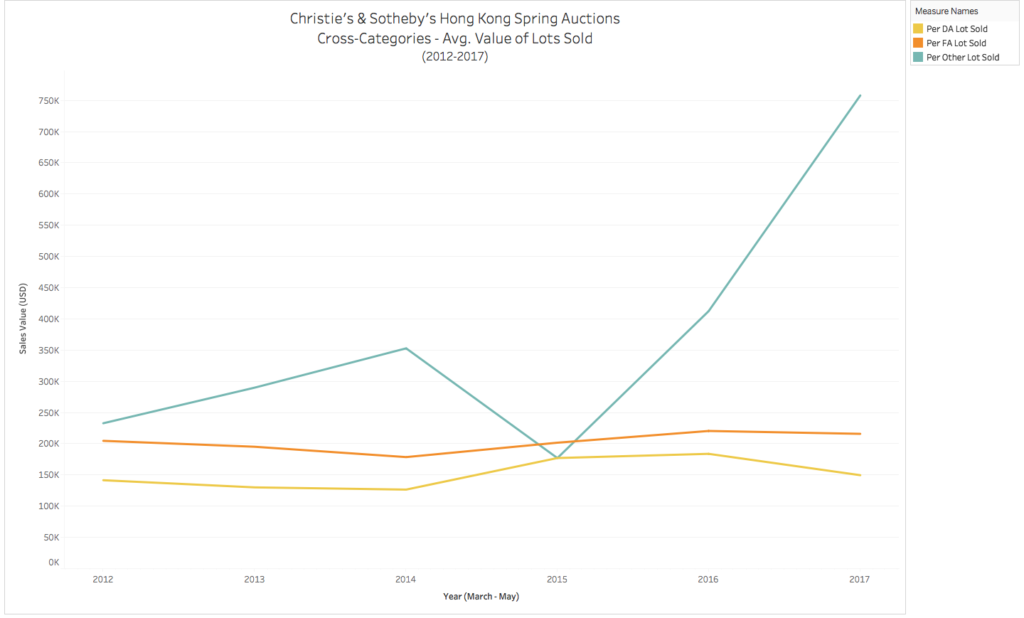

But how do all three markets—fine art, decorative art, and other—stack up against one another?

(Before we go much further, a few caveats about our “other” category: It includes some Sotheby’s specialty sales that might have offered an errant painting or decorative art object. It also includes significantly fewer lots overall, and smaller sample sizes are more likely to deliver more dramatic results. But these statistical blemishes were scarce enough—a few dozen modestly priced lots among thousands—to avoid undermining the overall analysis.)

Sure, according to the charts above, “other” looks like a category on the rise. But its bump owes in large part to a special one-item sale at Sotheby’s Hong Kong in April 2017, when the house auctioned the Pink Star diamond for a cool $71.2 million. Such an outsize result goes a long way toward explaining last year’s spikes.

Even before the Pink Star supernova, however, the market for our catch-all category of jewelry, watches, wine, and other works generally concentrated more than all others on fewer sales at higher prices (as judged by the percentage difference between value of lots sold and value of lots offered).

This suggests that, rather than being a safe bet, it is instead higher variance than the other two categories: A riskier gamble for consignors, but one that could pay off big if the odds fall in their favor.

The bottom line: The results indicate that fine art has been both the star performer in terms of total sales value and the most stable of the three categories—if not always the most exciting on a lot-to-lot basis. But for Christie’s and Sotheby’s, as well as the many private dealers flocking to Hong Kong, stable growth brings its own kind of excitement.