Analysis

A Data-Driven Look at This Week’s Day Sales Offers More Proof That the Auction Market Is Only Growing at the Top

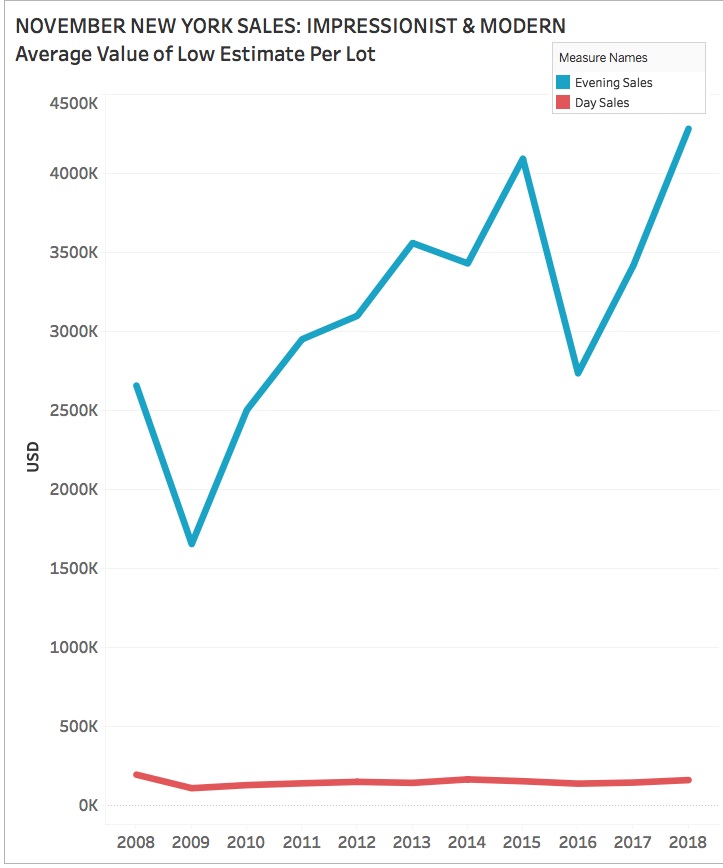

Evening-sale estimates have exploded, while their day-sale counterparts have stagnated.

. Image courtesy of Sotheby's.")

Evening-sale estimates have exploded, while their day-sale counterparts have stagnated.

Tim Schneider

ShareShare This Article

ShareShare This Article

It doesn’t take much immersion in the auction sector before you hear a common refrain: To find out what’s really happening in the market, ignore the theater of the evening sales and look at the day sales. So, in advance of this November’s morning and afternoon auctions at Sotheby’s, Christie’s, and Phillips New York, I examined how their pre-sale data has shifted since 2008, courtesy of my colleagues at the artnet Price Database.

It turns out, if the chorus about day sales is true, then the data suggests the “real” auction market has been running in place for 10 years, while trophy works have driven almost all the sector’s much-celebrated growth in the nighttime sessions. And we can clearly see as much with a few charts.

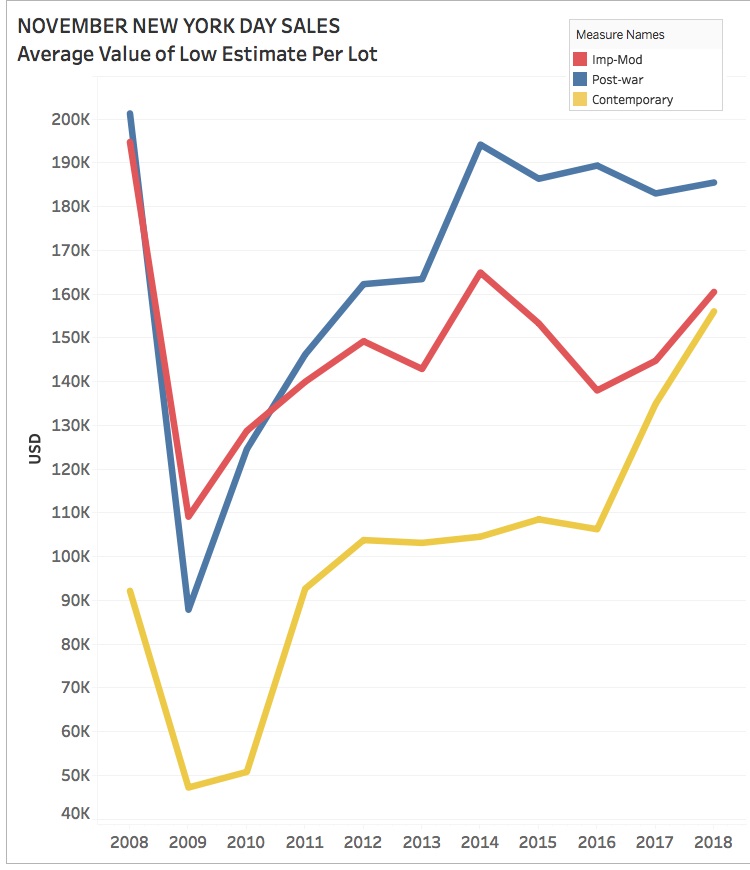

The average day-sale low estimate of contemporary works (which we define as those made by artists born in 1945 or later) has increased nearly 70 percent in the past decade, from about $92,000 per lot in 2008 to about $156,000 per lot this November. In contrast, post-war, Impressionist, and modern lots still have yet to return to their 2008 peaks in this sales cycle.

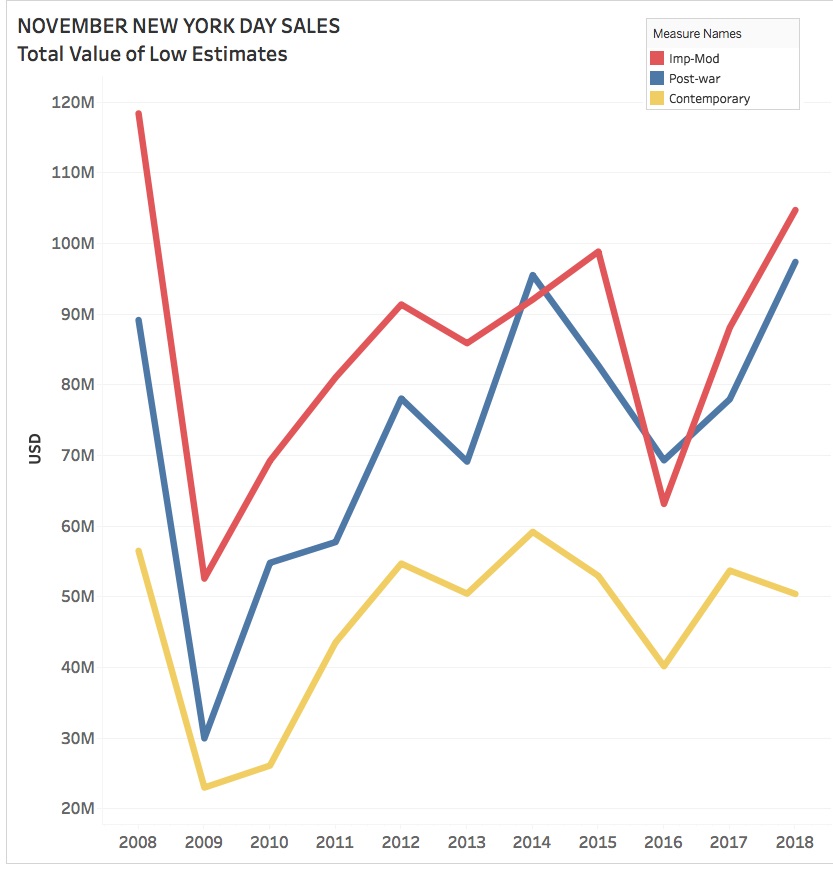

However, since the number of contemporary pieces consigned to the November day sales has plummeted by nearly half over the same period, the category’s total low estimate value has actually still declined this decade. Only post-war works reached a new apex this November at $97.4 million. But even this figure is less than 10 percent above the category’s 2008 mark of $89.2 million.

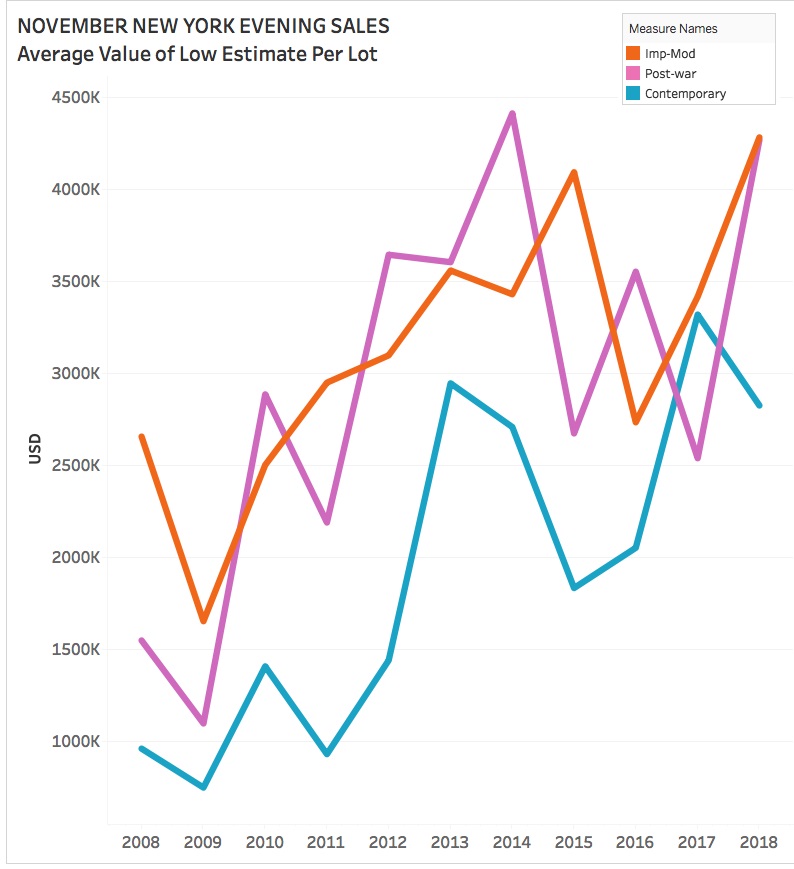

In contrast to what has transpired in day sales, estimates in evening sales have spiked in all three categories since 2008. Even the most modest gainers by percentage, Impressionist and modern works, still saw their pre-sale value increase by 61 percent on average. And although contemporary works carry the lowest average estimates of this group by dollar value, those estimates have nearly tripled in value in 10 years.

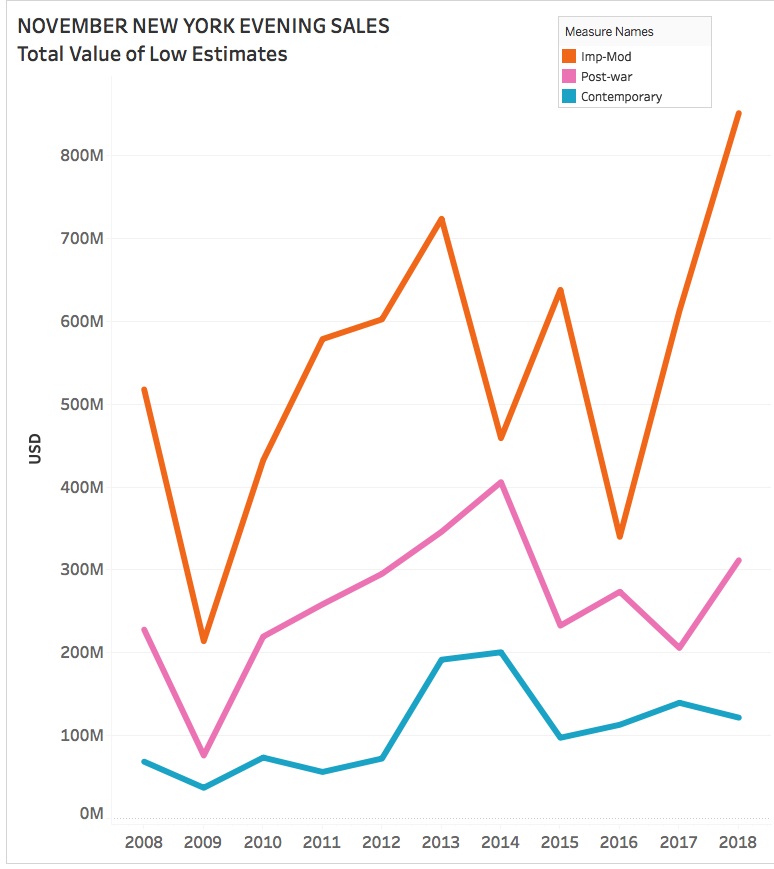

Since evening consignments of Impressionist and modern works have stayed relatively steady since 2008, this category shows the grandest growth of all three by value: a gain of over $333 million. Yet the drastic rise in average pre-sale estimate for post-war and contemporary evening works means that both categories this November will still eclipse their counterparts of a decade ago, despite the houses offering 40 to 50 percent fewer lots of those types than in 2008.

All comparisons of our pre-sale estimate metrics reflected the same gaping divide when charted: runaway growth in the premier evening auctions versus paltry or no growth in the day auctions. So while the most visible difference came when comparing the average low-estimate values of Impressionist and modern works—a difference of over $4.1 million per lot this November…

… every picture drawn from this data tells a similar story about the top-heavy realities of the art market since 2008. And that story is a sobering one about what’s “really” happening under the hammer.